This week we look at the PMI results for China and the US and reflect on their implications. Then we review the monetary policy decisions out over the past week including the announcement from the US FOMC. Then we wrap up with a look at the US employment figures for October, and the New Zealand employment stats for the September quarter.

1. China PMI

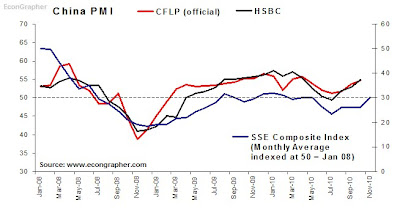

China saw a continued rebound in its manufacturing PMI figures for October, with the official CFLP figure rising to 54.7 from 53.8, and the the HSBC index rising to 54.8 from 52.9. Within the CFLP PMI index, the strong points were Production (57.1 vs 56.4), New orders (58.2 vs 56.3), and Inventory (49.5 vs 49.1), while the lower points were Employees (52.1 vs 52.4), and Supplier delivery (49.3 vs 50.4). So overall a reasonably good result, and reflects the continued strength in the Chinese economy - which is showing through into a higher stock market, with the SSE composite rising 15% in October.

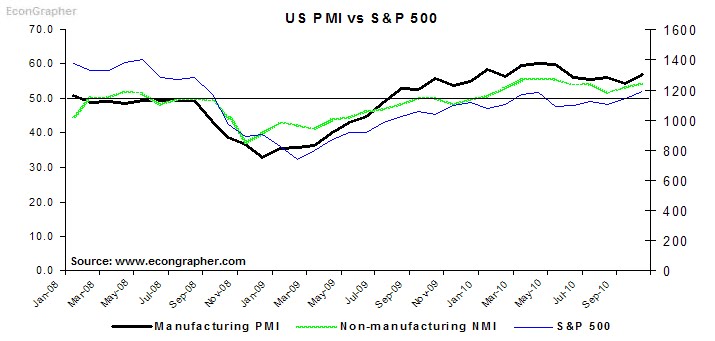

2. US PMI

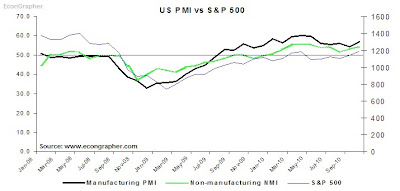

In the US, the October PMI result was also relatively positive with the main index rising to 56.9 from 54.4 driven by strength in new orders, production, and new export orders - with imports falling (a positive sign for net exports). While the non-manufacturing index also rose to 54.3 from 53.2, driven by strength in production, a large spike in prices, and back log of orders. So overall the October results for the US (unless there is some quirk to it) helps provide evidence or support for the non-double-dip scenario. So it is a positive, but at the same time the fundamentals are not quite there yet for economic growth to be anything more than subdued/baseline.

3. Monetary Policy Rates

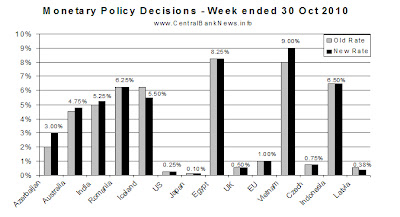

In monetary policy the main event was the US FOMC announcing the $600 billion asset purchase program, to be implemented at a pace of $75 billion per month. The other major moves were tightening of monetary policy rates in Azerbaijan (100bps), Vietnam (100bps), Australia (25bps), and India (25bps), and loosening of monetary policy rates in Iceland (75bps), and Latvia (12.5bps). Meanwhile other banks held rates due to low inflationary pressures and a desire to keep stimulatory monetary policy conditions to aid the economic recovery e.g. US, EU, UK, Japan.

4. US Nonfarm payrolls

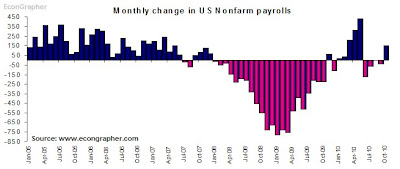

Back to the US, the October nonfarm payrolls pleasantly surprised to the upside, with 151k jobs added in October vs consensus 60k and previous -95k (revised to -41k). Private payrolls grew 159k in October vs 64k in September. Average hourly earnings crept up slightly 0.2% and the average work week was 34.3 hours vs 34.2 in September. So overall, as with the PMI results another good result for the US, a positive from the perspective that it's not going down, but there's still a long way to go before the ground lost during the crisis can be recovered.

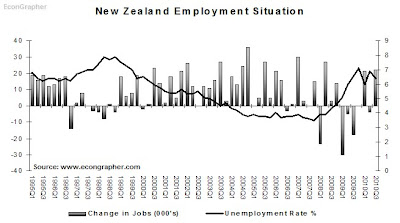

5. NZ Employment situation

In New Zealand the Q3 employment report saw the unemployment rate dip to 6.4% from a revised 6.9% in the June quarter. Total persons employed grew by 22k, with part-time jobs increasing 12k and full-time jobs expanding 10k. Across the sectors the jobs growth was relatively broad based with most sectors adding jobs. The figure reflects the progress, albeit slow, being made in the New Zealand economic recovery, but the subdued nature is showing through with deleveraging playing through. One major challenge for New Zealand is the high exchange rate which will impact on net exports, but a key driver of that is weakness in the US dollar. In terms of monetary policy the RBNZ has likely finished tightenings for the year, but will likely continue early next year as the recovery unfolds.

Summary

So we saw relatively strong PMI results in China which showed the economy is still running strong in the middle kingdom. The US also showed strong results in its PMI stats, providing some comfort against the double-dip scenario, but not yet being able to offer more than a subdued, sub-trend economic growth outcome. In monetary policy the major banks are holding tight but other banks are acting as the case demands, with several emerging economies opting to tighten or normalise monetary policy as inflation risks trump growth risks. In employment, the US showed a strong result in October, and New Zealand also showed a pretty good result in Q3. So overall it's a scene of economic recovery, but all is not yet clear and well.

Sources:

1. CFLP www.chinawuliu.com.cn & Markit/HSBC www.markiteconomics.com & Yahoo Finance finance.yahoo.com

2. Yahoo Finance finance.yahoo.com & Institute for Supply Management www.ism.ws

3. CentralBankNews.info www.centralbanknews.info

4. US Bureau of Labor Statistics www.bls.gov

5. Statistics New Zealand [url=http://www.stats.govt.nz/]www.stats.govt.nz[/url]

Article Source: http://www.econgrapher.com/top5graphs6nov.html

1. China PMI

China saw a continued rebound in its manufacturing PMI figures for October, with the official CFLP figure rising to 54.7 from 53.8, and the the HSBC index rising to 54.8 from 52.9. Within the CFLP PMI index, the strong points were Production (57.1 vs 56.4), New orders (58.2 vs 56.3), and Inventory (49.5 vs 49.1), while the lower points were Employees (52.1 vs 52.4), and Supplier delivery (49.3 vs 50.4). So overall a reasonably good result, and reflects the continued strength in the Chinese economy - which is showing through into a higher stock market, with the SSE composite rising 15% in October.

2. US PMI

In the US, the October PMI result was also relatively positive with the main index rising to 56.9 from 54.4 driven by strength in new orders, production, and new export orders - with imports falling (a positive sign for net exports). While the non-manufacturing index also rose to 54.3 from 53.2, driven by strength in production, a large spike in prices, and back log of orders. So overall the October results for the US (unless there is some quirk to it) helps provide evidence or support for the non-double-dip scenario. So it is a positive, but at the same time the fundamentals are not quite there yet for economic growth to be anything more than subdued/baseline.

3. Monetary Policy Rates

In monetary policy the main event was the US FOMC announcing the $600 billion asset purchase program, to be implemented at a pace of $75 billion per month. The other major moves were tightening of monetary policy rates in Azerbaijan (100bps), Vietnam (100bps), Australia (25bps), and India (25bps), and loosening of monetary policy rates in Iceland (75bps), and Latvia (12.5bps). Meanwhile other banks held rates due to low inflationary pressures and a desire to keep stimulatory monetary policy conditions to aid the economic recovery e.g. US, EU, UK, Japan.

4. US Nonfarm payrolls

Back to the US, the October nonfarm payrolls pleasantly surprised to the upside, with 151k jobs added in October vs consensus 60k and previous -95k (revised to -41k). Private payrolls grew 159k in October vs 64k in September. Average hourly earnings crept up slightly 0.2% and the average work week was 34.3 hours vs 34.2 in September. So overall, as with the PMI results another good result for the US, a positive from the perspective that it's not going down, but there's still a long way to go before the ground lost during the crisis can be recovered.

5. NZ Employment situation

In New Zealand the Q3 employment report saw the unemployment rate dip to 6.4% from a revised 6.9% in the June quarter. Total persons employed grew by 22k, with part-time jobs increasing 12k and full-time jobs expanding 10k. Across the sectors the jobs growth was relatively broad based with most sectors adding jobs. The figure reflects the progress, albeit slow, being made in the New Zealand economic recovery, but the subdued nature is showing through with deleveraging playing through. One major challenge for New Zealand is the high exchange rate which will impact on net exports, but a key driver of that is weakness in the US dollar. In terms of monetary policy the RBNZ has likely finished tightenings for the year, but will likely continue early next year as the recovery unfolds.

Summary

So we saw relatively strong PMI results in China which showed the economy is still running strong in the middle kingdom. The US also showed strong results in its PMI stats, providing some comfort against the double-dip scenario, but not yet being able to offer more than a subdued, sub-trend economic growth outcome. In monetary policy the major banks are holding tight but other banks are acting as the case demands, with several emerging economies opting to tighten or normalise monetary policy as inflation risks trump growth risks. In employment, the US showed a strong result in October, and New Zealand also showed a pretty good result in Q3. So overall it's a scene of economic recovery, but all is not yet clear and well.

Sources:

1. CFLP www.chinawuliu.com.cn & Markit/HSBC www.markiteconomics.com & Yahoo Finance finance.yahoo.com

2. Yahoo Finance finance.yahoo.com & Institute for Supply Management www.ism.ws

3. CentralBankNews.info www.centralbanknews.info

4. US Bureau of Labor Statistics www.bls.gov

5. Statistics New Zealand [url=http://www.stats.govt.nz/]www.stats.govt.nz[/url]

Article Source: http://www.econgrapher.com/top5graphs6nov.html