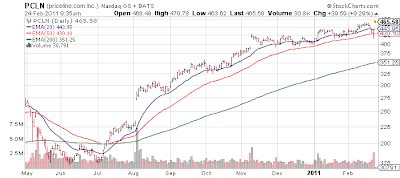

Priceline.com (PCLN, Financial) continues to astound me with it's performance. Since the August lows, it has doubled... after having a stellar 2009 and early 2010. I was a mega bull on this name a long while back but in this case I certainly left the train far too early and left a ton on the table, as the stock has gone so much farther than I anticipated. Despite being a momentum stock with heightened expectations for much of the past year and a half, each of the last 3 quarters the stock has gapped up on earnings which is a rare thing to do, three times in a row.

Analysts were in fro $3.09 but the company was able to beat that by 31 cents. They also guided up for the next year.

Via IBD:

Analysts were in fro $3.09 but the company was able to beat that by 31 cents. They also guided up for the next year.

Via IBD:

- Priceline late Wednesday reported Q4 profit that shattered analyst views, but sales just missed as airline ticket revenue slipped. Still, the name-your-price online travel site guided profit and sales above analyst views for the current quarter.

- The Norwalk, Conn.-based company said it earned $3.40 a share minus special items last quarter, up 71% from the year-ago quarter. That beat by 31 cents the estimate of analysts polled by Thomson Reuters. In Q3, Priceline beat by 36 cents.

- Sales surged 35% to $731 million, but still missed analyst expectations for $734.9 million.

- Gross bookings, the value of all travel services bought by customers, jumped 44.2% to $3.26 billion in Q4, led by a 64.9% surge in international gross travel bookings. Domestic bookings rose 8.5%.

- Hotel room nights booked surged 50.6% worldwide, but airline ticket bookings fell 2.3%.

- "This company continues to execute," said Standard & Poor's equity analyst Scott Kessler. "Priceline has demonstrated time and again that they are the best operator in (online travel)."

- "Their growth strategy in Europe is working for them better than anyone else in the industry," said Morningstar analyst Warren Miller.

- For Q1, Priceline expects to earn $2.34 to $2.44 a share minus items, on a 29% to 34% increase in sales. Analysts were expecting EPS of $2.30 on a 27% revenue rise.

- Boyd said he expects "some deceleration" in Priceline's international growth "due to the sheer size of the (online) travel business" and hard-to-beat comparisons as the world economy recovers.

- Analysts say Priceline's risks in 2011 include whatever impact Middle East tensions will have on travel and fuel costs.