This is part II of my previous post on the fundamentals of value creation. In part I, we described how value creation can be quantitatively captured by looking at two key variables: growth rate (g) of NOPAT and return on invested capital (ROIC). If you are not familiar with these concepts, I recommend you read part I (here) before continuing.

A computer could easily give you a list of all companies that have grown at healthy rates and at ROIC that consistently exceeded the cost of capital by some reasonably wide margin. In fact, Joel's Greenblatt's "Magic Formula" screen (based on his book ("Little Book that Beats the Market") is programmed to almost do this — find high ROIC companies trading at cheap valuations. The formula has shown to work well if you stay disciplined and stick to the formula even when it looks like it isn't working.

I believe a "defensive" investor (investors that are unable to devote much time to the process of investing) will be well served by just sticking to the prescriptions laid out by Mr. Greenblatt in his book. However, for the "enterprising" investor (investors that are willing to put the time and thought required for the process of making sound investing decisions) the edge is in going one step further and digging answers to questions like:

Fortunately, I am not the first one to ask these questions. Renowned Harvard Business School professor, Michael Porter, addressed these questions in his two books that are now classics, "Competitive Strateg " (1980) and "Competitive Advantage" (1985) and numerous other HBR articles published since then.

Returns in a business are highly dependent on the industry in which it operates. Pharmaceutical and biotechnology companies protected by patents have produced a median returns of 23.5%, whereas most airlines have destroyed capital.

The reason for difference in industries performance lies mainly in differences between their competitive structures. When most people think of competition, they think of the rivals trying to earn the sale. However, competition for returns is actually a struggle between multiple players, not just rivals, over who will capture the value an industry creates.

It's true, of course, that companies compete for profits with their rivals. But they are also engaged in a struggle for profits with their customers, who would be happy to pay less and get more. They compete with their suppliers, who would always be happier to be paid more and deliver less. They compete with producers who make products that could be substituted for their own. And they compete with potential rivals as well as existing ones, because even the threat of new entrants place limits on how much they can charge their customers.

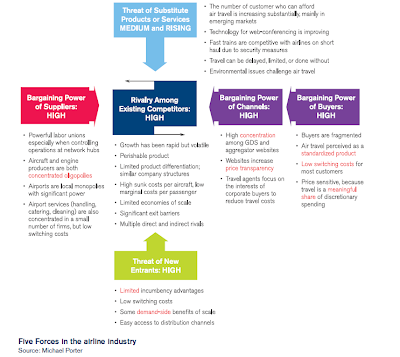

These five forces — the intensity of rivalry among existing competitors, the bargaining power of buyers, the bargaining power of suppliers, the threat of substitutes, and the threat of new entrants — determine the industry's competitive structure which in turn determine to a large degree the returns that a business in that industry generates.

The best way to learn about the five forces framework is to apply it to a specific industry. We'll use the example of the airline industry to gain a much deeper insight into the underlying reasons for the industry's poor record for value creation.

Intensity of Rivalry (HIGH):

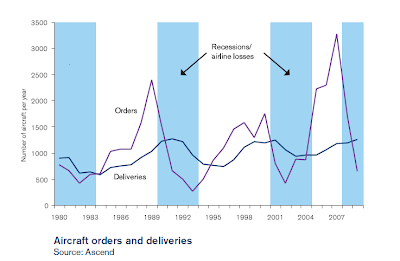

Rivalry in the airline industry is highly intense. Intensive rivalry is driven by a number of underlying characteristics of airline transport. At its core, the aggressive buildup of capacity that never leaves the industry drives pricing decisions that fail to support attractive returns.

Bargaining Power of Customers (HIGH):

Customer bargaining power is high and rising driven by the following factors:

Power of Channels:

The bargaining power of suppliers is high for several critical inputs.

Airframe and engine manufacturers:

Threat of Substitutes (MEDIUM AND RISING):

The most powerful substitute to aircraft travel is the decision not to travel.

The threat of new entrants is high. Over 1,300 new airlines were established in the past 40 years, an average of over 30 each year. Entry has been highly cyclical. Remarkably, entry rates have shown no sign of slowing down despite low industry profitability.

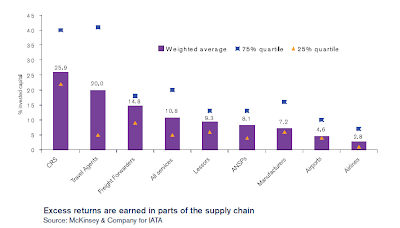

As you can see, the airline industry is squeezed by all the five forces causing it to have the worst economics for any industry. In fact, airlines capture the least value among all the players in the entire supply chain.

This concludes our discussion on the first question we raised at the beginning of this article: "Why does an industry have a high or low ROIC?" It's primarily a result of the five competitive forces that shape the industry structure.

Just because the industry on the whole has been destroying value doesn't mean that there aren't individual operators that aren't achieving returns above the cost of capital. As a matter of fact, there are quite a few that have generated large economic value. This will be the purpose of the article in the next part in this series. We'll use the example of Southwest airlines to answer the remaining two questions raised at the beginning: "Why does a company have ROIC much higher than the rest of the industry?" and "What will be result of management's current actions on future ROIC?"

Southwest airlines, a low-cost carrier, had a strong value creator record in 1980s and 1990s. However, during the 2000s, once the impact of the well-timed fuel hedging was removed, Southwest seems to have destroyed capital. Thus, it is instructive to closely examine Southwest because it will answer both the remaining questions. To be continued...

References:

A computer could easily give you a list of all companies that have grown at healthy rates and at ROIC that consistently exceeded the cost of capital by some reasonably wide margin. In fact, Joel's Greenblatt's "Magic Formula" screen (based on his book ("Little Book that Beats the Market") is programmed to almost do this — find high ROIC companies trading at cheap valuations. The formula has shown to work well if you stay disciplined and stick to the formula even when it looks like it isn't working.

I believe a "defensive" investor (investors that are unable to devote much time to the process of investing) will be well served by just sticking to the prescriptions laid out by Mr. Greenblatt in his book. However, for the "enterprising" investor (investors that are willing to put the time and thought required for the process of making sound investing decisions) the edge is in going one step further and digging answers to questions like:

- Why does an industry have a high (or low) ROIC? (I'll just focus on ROIC instead of g since analyzing the drivers of g are well popularized).

- Why is this company's ROIC so much higher (or lower) than the industry?

- Can it continue to perform at these levels? What will be the impact of management's current actions on company's future ROIC?

Fortunately, I am not the first one to ask these questions. Renowned Harvard Business School professor, Michael Porter, addressed these questions in his two books that are now classics, "Competitive Strateg " (1980) and "Competitive Advantage" (1985) and numerous other HBR articles published since then.

Returns in a business are highly dependent on the industry in which it operates. Pharmaceutical and biotechnology companies protected by patents have produced a median returns of 23.5%, whereas most airlines have destroyed capital.

The reason for difference in industries performance lies mainly in differences between their competitive structures. When most people think of competition, they think of the rivals trying to earn the sale. However, competition for returns is actually a struggle between multiple players, not just rivals, over who will capture the value an industry creates.

It's true, of course, that companies compete for profits with their rivals. But they are also engaged in a struggle for profits with their customers, who would be happy to pay less and get more. They compete with their suppliers, who would always be happier to be paid more and deliver less. They compete with producers who make products that could be substituted for their own. And they compete with potential rivals as well as existing ones, because even the threat of new entrants place limits on how much they can charge their customers.

These five forces — the intensity of rivalry among existing competitors, the bargaining power of buyers, the bargaining power of suppliers, the threat of substitutes, and the threat of new entrants — determine the industry's competitive structure which in turn determine to a large degree the returns that a business in that industry generates.

The best way to learn about the five forces framework is to apply it to a specific industry. We'll use the example of the airline industry to gain a much deeper insight into the underlying reasons for the industry's poor record for value creation.

Intensity of Rivalry (HIGH):

Rivalry in the airline industry is highly intense. Intensive rivalry is driven by a number of underlying characteristics of airline transport. At its core, the aggressive buildup of capacity that never leaves the industry drives pricing decisions that fail to support attractive returns.

- Perishable Product: An unfilled airline seat cannot be stored. Costs for providing capacity are thus largely sunk in the short term thus creating severe pressure on price discounting.

- Undifferentiated Product: The product offered is highly similar across airlines as new product features (flat bed, entertainment system etc.) are quickly imitated among peers.

- Low Marginal Cost Structure: High fixed costs exist at the level of individual aircraft, marginal costs for adding additional customers are very low, which further reinforces price discounting.

- High Exit Barriers: The disappearance of capacity and exit of companies are two key adjustment mechanisms through which other industries support normal returns. In the airline industry, neither of the two adjustment mechanisms work:

- Aircraft capacity can easily be deployed to different geographic markets. Thus, even if particular companies might leave the market, airline capacity usually stays in the market, and disappears only in the long run.

- Less than 1% of airlines exit the market in an average year.

- Governments have a tradition of bailing out airlines. In the US, Chapter 11 forces the debtors to provide the bailout; both mechanisms allow companies to shed some of their fixed costs. Management is often not held accountable in a bailout, reducing the disincentives for managers to avoid going through such periods.

- There are also specific other barriers that limit airlines ability to reduce capacity overall and on specific routes.

- Airlines are forced to take a capital loss charge if they sell an aircraft in a downturn. Getting out of a leasing contract is equally costly in a downturn. Keeping capacity idle is costly, but it avoids the capital loss.

- Gradual reduction in capacity is also complicated by need to retire by aircraft, not by seat.

- Use-it-or-lose-it rules on airport slots create barriers to exit from routes. Losing a connection can have ripple effects on other parts of the network for carriers that use the hub-and-spoke-model.

- And lastly, reducing capacity by moving to a smaller aircraft on specific connections increases the average cost per available seat kilometer.

Bargaining Power of Customers (HIGH):

Customer bargaining power is high and rising driven by the following factors:

Power of Channels:

- Aggregator website have concentrated consumers' buying power. Their focus on price comparison has significantly increased the transparency of prices across carriers. Global distributions systems (GDSs) have made it very easy for new aggregator websites to enter the market. The strong market power of the three dominant GDSs has triggered the current conflict between GDSs and US airlines.

- Travel agents now often represent the entire demand of large corporate clients, with significant power to move demand across carriers. Furthermore, agents have to comply with corporate policies that have become more price oriented.

- Air travel for leisure customers is a significant discretionary spending item, increasing price sensitivity.

- Switching costs are very low for leisure customers. Loyalty programs primarily matter to those who are traveling extensively on business.

- Frequency of a particular route is the key (and probably the only) differentiator among airlines of a similar type for a given connection for business travelers.

The bargaining power of suppliers is high for several critical inputs.

Airframe and engine manufacturers:

- Airframe and engine manufacturers are highly concentrated globally. These suppliers have high bargaining power.

- Switching costs between airframes and engines are modest. There are some fixed costs of introducing a new type of aircraft/engine to a fleet. For new aircraft, the often significant type lag between order and production create some switching barriers.

- Airframe and engine manufacturers have important alternate markets that they can sell to, especially the market for defense equipment.

- Airframe manufacturers have thus far not exploited their bargaining power to maximize their short-term returns. They have, however, been able to shift most of the market risk associated with aircraft purchases to airlines.

- The aggressive competition between aircraft manufacturers has hurt the airline industry structure by encouraging aggressive capacity buildup and reducing barriers to entry into the airline industry.

- Airlines are dependent on skilled employees, pilots and technical personnel. Network airlines (ones that operate hub-and-spoke model) are particularly vulnerable to disruptions at their hubs, which increases power of unions at these locations

- Unions tend to be local monopolies. In airlines there are different unions for different types of staff, with each of them having the ability to disrupt operations. Union power and regulation have led to significant lack of downward flexibility in staffing levels and wages, especially for legacy airlines.

- There are significant cost differences between new entrants, companies in bankruptcy protection, and unionized incumbents, where high wages continue to be paid relative to other industries, especially for employees with specialized skills like pilots.

- Employees have traditionally one of the groups most successful in capturing the value created by the airline industry. They remain powerful where labor regulations and hub-and-spoke give them leverage. Because union power increases as companies mature, the nature of labor relations also erodes industry structure by encouraging entrants and bankruptcy to avoid union related costs, even if there is no productive advantage.

- Many airports are local monopolies with limited competition from nearby secondary airports. There is little entry by new airports, so the main check of the exploitation of market power is through regulation. The pricing power that the local monopoly gives to an airport depends significantly on the potential traffic flows to which it provides access.

- Many airports in the US continue to be used by local governments to foster economic development through subsidizing airlines' operations. On average airports do not earn their cost of capital.

- Airport switching costs are high, especially for network airlines that are focused on providing connections. It is easier for point-to-point airlines, especially low cost carriers (LCC) flying to larger metropolitan areas with a number of airports or regional airports not served by network airlines.

- Airports marginally better profitability compared to airlines indicates that their effective bargaining power has been limited. The main impact on airline industry structure has been through infrastructure capacity constraints and other operational practices that have limited effective capacity adjustments in serving particular connections

- They have limited bargaining power, largely because airlines have the option of providing the service in-house.

Threat of Substitutes (MEDIUM AND RISING):

The most powerful substitute to aircraft travel is the decision not to travel.

- Time and inconvenience of security measures have reduced the overall attractiveness of scheduled airlines transport relative to substitutes.

- For short-haul connections, a key concern of airline passengers is punctuality. While airlines have some control, the key drivers for delays are the air control systems and airports.

- The slightly growing role of substitutes such as video conferencing for business travel has been driven by improvements in their performance and falling costs.

The threat of new entrants is high. Over 1,300 new airlines were established in the past 40 years, an average of over 30 each year. Entry has been highly cyclical. Remarkably, entry rates have shown no sign of slowing down despite low industry profitability.

- Economies of scale exist on the demand side, i.e.. it is easier to generate demand with a strong brand, a wide distribution presence, and a large network of connections. There are also benefits from established operations in generating route density to allow larger aircraft (lower costs) and higher frequency (higher price). But since most of the entry is through existing airlines operating in adjacent geographies that do not face these barriers, these factors do not significantly deter entry.

- Supply-side economies of scale are limited as airlines grow beyond a level of around 50 aircraft. This creates some disadvantages for new airlines but not for existing ones looking to expand into new markets. Because capacity comes in lumps, airlines operating in adjacent geographies face the lowest entry barriers. They can serve a new destination through spare capacity on existing airplanes

- Access to distribution channels is easy for new entrants, much more so than in the past. GDSs and the internet now enable new airlines to list and make their flights available through a larger number of aggregator websites and travel agencies. This is a big change from the past where reservation systems and travel agents were controlled by incumbents.

- Legacy rights on slots give some advantages but there is secondary trading of slots at congested airports and thus no advantages until slot capacity is reached. If infrastructure does not grow in line with travel volumes, however, it can become an increasing bottleneck limiting entry at most frequented hubs.

- Substantial capital is needed to acquire a new aircraft. Prior to the financial crisis, however, external financing was widely available. The growing presence of leasing companies reduces capital requirements. However, it remains hard for new entrants to meet operational cash flow requirements during persistent downturns.

As you can see, the airline industry is squeezed by all the five forces causing it to have the worst economics for any industry. In fact, airlines capture the least value among all the players in the entire supply chain.

This concludes our discussion on the first question we raised at the beginning of this article: "Why does an industry have a high or low ROIC?" It's primarily a result of the five competitive forces that shape the industry structure.

Just because the industry on the whole has been destroying value doesn't mean that there aren't individual operators that aren't achieving returns above the cost of capital. As a matter of fact, there are quite a few that have generated large economic value. This will be the purpose of the article in the next part in this series. We'll use the example of Southwest airlines to answer the remaining two questions raised at the beginning: "Why does a company have ROIC much higher than the rest of the industry?" and "What will be result of management's current actions on future ROIC?"

Southwest airlines, a low-cost carrier, had a strong value creator record in 1980s and 1990s. However, during the 2000s, once the impact of the well-timed fuel hedging was removed, Southwest seems to have destroyed capital. Thus, it is instructive to closely examine Southwest because it will answer both the remaining questions. To be continued...

References:

- Valuation: Measuring and Managing the Valuation of Companies, McKinsey & Company

- What is Strategy, Michael Porter, Harvard Business Review

- The Five Competitive Forces that Shape Strategy, Michael Porter, Harvard Business Review

- Understanding Porter, Joan Magretta, Harvard Business Review Press

- Vision 2050, International Air Transport Association, Feb 2011