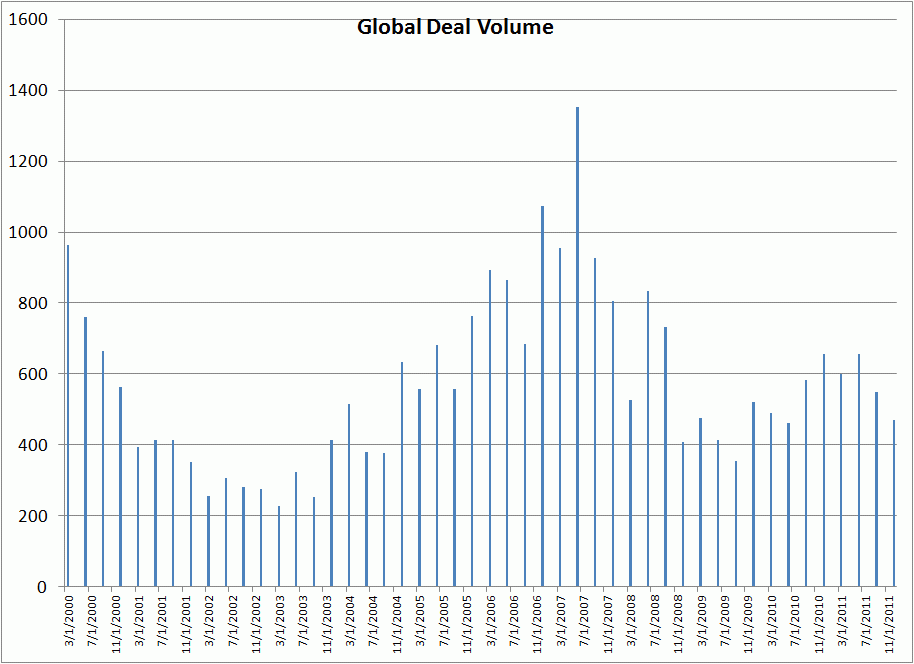

In 2011, companies worldwide announced 27,668 mergers, acquisitions and divestitures, bringing the total transaction value to USD2.22 trillion. Two major up-cycles in corporate dealmaking have occurred in the 12 years. Check out this graph of quarterly deal flow.

Source: Bloomberg

The 2000-02 technology bust and the collapse of the high-flying Nasdaq halted the late 1990s boom in merger and acquisitions (M&A). The technology sector drove much of this deal flow, with aggressive large-capitalization acquirers such as Cisco Systems (CSCO, Financial) leading the way.

M&A activity bottomed in 2003-04, following the economy's lead. But dealmaking boomed during the subsequent three years, bolstered by robust economic growth and benign credit conditions. Private-equity firms fueled much of the surge in mergers and acquisitions, taking advantage of low interest rates to borrow vast sums of money for their war chests.

The intensifying financial crisis ended this historic M&A boom in 2008.

Since deal flow bottomed in 2009, M&A activity has accelerated substantially, with the energy sector leading the way. In 2011 takeovers of oil and gas exploration and production (E&P) firms totaled more than $105 billion. The pipeline industry ranks third in the 2011 M&A league table, with more than $57 billion in announced deals. The midstream sector also furnished the biggest deal of 2011, Kinder Morgan Inc.'s (KMI) takeover of El Paso Corp (EP) for $39 billion in cash, stock and assumed debt.

More important, the stage is set for the M&A boom to continue in 2012.

With their bulletproof balance sheets, blue chips such as Microsoft Corp (MSFT, Financial) and ExxonMobil Corp (XOM, Financial) have enough cash on hand to close major deals regardless of conditions in global credit markets. However, smaller companies usually need to fund a portion of their acquisitions through borrowing. Private-equity outfits often borrow heavily to finance their deals.

When the credit is readily available, the universe of potential acquirers expands and deal premiums rise.

Despite ongoing concerns that the EU sovereign-debt crisis could spark a 2008-style credit crunch, capital markets remain open for business in the US. In fact, energy firms of all sizes continue to enjoy access to relatively inexpensive capital, a testament to the sector's favorable long-term growth prospects.

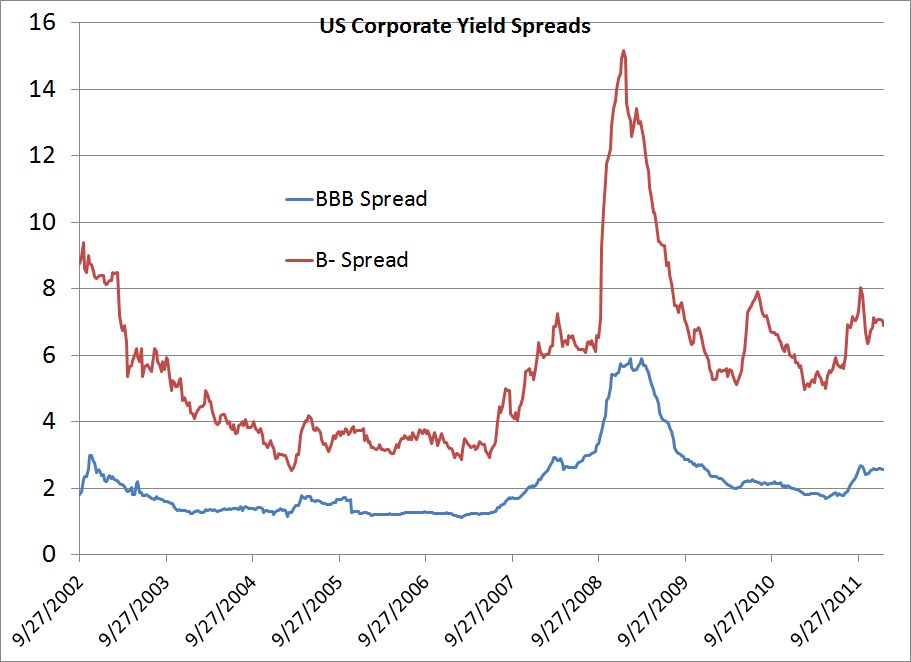

Check out this graph of the yield spreads between 10-year US corporate bonds that Standard & Poor's rates BBB and B- (several notches into junk territory) and Treasury bonds of the same duration. Note that a rising yield spread indicates that companies face a tightening credit market and higher borrowing costs.

Source: Bloomberg

Yield spreads between corporate bonds and US Treasuries spiked during the 2008-09 credit crunch. At the height of the crisis, companies with a B- credit rating from Standard & Poor's paid about 1,500 basis points (15 percent) more to borrow money than the US government-a prohibitive cost of borrowing that effectively closed the bond markets to these firms. Today, this yield spread sits at slightly less than 7 percent, in line with prevailing rates about a decade ago and an improvement from last summer's high of more than 8 percent.

Investors should also remember that the yield spread also hinges on 10-year Treasury bonds, which currently yield less than 2 percent. The extraordinarily low yield on US government debt reflects investors' flight to safety amid heightened concern about the EU sovereign-debt crisis and global economic growth. Depressed yields on US government debt have also inflated this spread.

In absolute terms, the current average yield on 10-year bonds issued by companies rated B- is less than 8.75 percent. That's only slightly higher than the 7.5 to 8 percent that such a corporation would have paid at the height of the credit boom.

Companies rated BBB can borrow money for 10 years at roughly 2.5 percent more than what the US government would pay. The yield spread on bonds issued by companies with a BBB credit grade ticked up slightly during the summer and has declined steadily since early October. In absolute terms, BBB-rated credits currently pay an average interest rate of 4.4 percent, much less than the 6 percent a company of equivalent credit standing paid to borrow money during the boom years.

Despite the negative headlines about Europe, credit market conditions should continue to support M&A activity.