National Presto Industries (NPK, Financial) is an oddly diversified producer of military arms, adult diapers, and small cooking appliances with a market capitalization of well under $1 billion.

-Seven Year Average Revenue Growth Rate: 15.3%

-Seven Year Average EPS Growth Rate: 17.5%

-Recently, Growth has Stalled

-Dividend Yield: 7.67%

-Balance Sheet: Perfect

National Presto has been disappointing over the last year, with revenue and profit reductions, but the current numbers still imply a decent potential investment. I advise potential investors to individually cautiously weigh the potential rewards and risks.

National Presto has been in business for over 100 years, and currently consists of three business segments:

Housewares/Small Appliance Segment

This segment accounts for 30% of revenue and 23% of operating profit, and producers a range of household small appliances, mostly kitchen-related, ranging from pressure cookers to deep fryers, to products for pizza.

Defense Products Segment

This segment accounts for 47% of revenue and 74% of operating profit, and produces 40mm ammunition for the Army, as well as fuses, cartridges, less-than-lethal products for law enforcement, and precision electro-mechanical assemblies.

Absorbent Products Segment

This segment accounts for 23% of revenue and 3% of operating profit, and produces adult diapers.

Price to Free Cash Flow: 12.2

Price to Book: 1.6

Return on Equity: 14%

Revenue and free cash flow for National Presto have been rather erratic over the period. Management made excellently timed acquisitions of defense businesses during an early period of a long set of wars. In 2011, the company faced decreases in volume and profitability, especially in the appliances segment.

Earnings and dividends have been substantial due to smart value investment on the part of management, but in 2011, they finally ran into problems.

What most blue-chip dividend growth businesses do is, they keep moderate dividend payout ratios, and use extra capital for share repurchases. Instead of doing that, National Presto pays out basically all of their free cash as dividends, which makes the dividend larger, but makes it less resilient to declines in earnings. If you take a look at the combined dividends and share repurchases of any dividend growth business, you’ll see that they grow and shrink with business conditions, even as the dividend segment continues to grow. NPK is the same, except that 100% of it is dividends, and so the dividend segment puts aside consistent growth in favor of pure dividend payouts.

With a market cap of under $550 million, the National Presto holds $133 million in cash and cash equivalents on their balance sheet. The company has zero debt, a rather small amount of goodwill, and a current ratio of around 5. The balance sheet, therefore, is perfect.

In addition, the long-tenured chairperson and CEO Maryjo Cohen currently owns an impressive chunk of the company. Her interests are therefore aligned with shareholders, and aligned with long term success rather than short term expectations. That explains why this has been such a shareholder friendly company over the last several years.

The conglomerate is value-oriented, with small overhead, fair and simple executive compensation, and plenty of insider ownership.

Management can allocate resources to make smart acquisitions, and tends to return most of the profits back to shareholders in the form of an annual special dividend.

-In late 2011, the company acquired manufacturing assets of less than lethal ammunition. This includes tear gas grenades, specialty impact ammo, gas masks, and more, along with the associated training with these devices. Customers include law enforcement and corrections facilities. Annual sales are estimated at $7.5 million, and it’s good that this diversifies the defense segment a little bit away from the Department of Defense, and warfare.

-National Presto appliances could rebound from their poor 2011 performance. The CEO attributed much of the performance due to consumer and retailer habits mismatch, but also due to private label competition. National Presto will be introducing some new and exclusive products in 2012.

-I previously identified the absorbent products segment as a risk area due to the concentration of the customer base, but the company has begun successfully diversifying and growing their customer base.

-The company has $133 million, or approximately a quarter of the market capitalization, held in cash-equivalents. Low interest rates have been hurting them here, and so eventual increases in interest rates can provide better returns on this capital. Or, this can be viewed as substantial resources for smart acquisitions.

On the other hand, NPK does have a fair number of significant risks, and these risks have strongly demonstrated themselves in 2011.

Their appliance and absorbent products segments face commodity cost issues and have a concentrated customer base. There is little economic moat to speak of, so pricing power is limited, and private label products have been threatening NPK market share.

Their defense segment has irregular timing of contracts, so money doesn’t flow in regularly. The largest risk of all is how the defense segment (National Presto’s largest segment) is mostly reliant on the Department of Defense, which has been winding down operations. Some of the products are training related, as these are ammo and other types of products rather than, say, multi-billion-dollar fighter jet contracts, so there is some defensiveness there. In addition, the acquisition of less than lethal products for law enforcement is a smart one, in my view.

Still, the possibility of a major contract loss in this segment is probably the largest risk. That’s the one thing that could quickly turn this into a poor investment. I wouldn’t be surprised to see decreased profitability from this segment since margins are so high and will have to come down, and it appears that this is factored into the current stock price in the high $70”²s. There was a major five-year contract awarded to National Presto in 2005, and another major five-year contract awarded in 2010. The customer can cancel these contracts at their convenience.

The CEO has predicted the same troubles for 2012 as came to pass in 2011: high commodity and energy costs, and low interest rates.

In my analysis from last year, I discussed the risks, and many of them came to pass. Commodity costs impacted the absorbent products and appliance segments, in particular. I mentioned that they have a lack of moat, and therefore a lack of pricing power, and this has indeed been the case.

Some of my estimates have apparently been incorrect here. I had expected that a recession would indeed impact the business, but that if anything, consumers would eat at home more and dine out less to save money, and therefore would purchase more of National Presto’s appliances, or at least wouldn’t decrease their purchases too much. That has not been the case.

More particularly, CEO Cohen has stated that in addition to private label products taking market share from National Presto, part of the problem has to do with retailers and consumer habits, which is something I didn’t factor in. As she described it in a press release, customers are no longer stockpiling products such as National Presto small cooking appliances in advance. Instead, they are buying just when they need them. This has meant that retailers have kept inventories very low, so during the holiday season when they actually were to be purchased, consumers often found shelves empty. So a combination of private label competition and misaligned customer and retailer habits, have resulted in a larger impact to National Presto’s appliance segment than I had anticipated, and have more than offset my expectation that small cooking appliances would be rather defensive.

I’m still holding my position, but not increasing it. My current holding value is down considerably compared to my cost basis, but factoring in the large dividends received, my cost basis is not much lower than my initial investment. I have to reduce the fair valuation of the company, because valuation is based on growth rates, and while I had previously factored in modest growth, I can no longer do so.

Going forward, the company is currently priced for no growth. With a P/E and P/FCF of around 11 and 12, and even lower than that if a portion of the cash is factored out of the valuation, which is a common valuation practice, the company already has a lot of risk factored in.

If the business were to merely stay static from this point, the large single-digit dividend yield would provide a reasonable return. If National Presto were to lose substantial military contracts or face continued appliance decreases, then the investment could prove to be a poor one. I observe that assumed decline in defense profitability is factored into the stock price. On the other hand, if the company fixes a few problematic areas, keeps a substantial portion of its backlog of contracts, and continues to make smart acquisitions, modest long term growth combined with the dividend could result in solid returns.

Full Disclosure: I own shares of NPK.

-Seven Year Average Revenue Growth Rate: 15.3%

-Seven Year Average EPS Growth Rate: 17.5%

-Recently, Growth has Stalled

-Dividend Yield: 7.67%

-Balance Sheet: Perfect

National Presto has been disappointing over the last year, with revenue and profit reductions, but the current numbers still imply a decent potential investment. I advise potential investors to individually cautiously weigh the potential rewards and risks.

Overview

National Presto Industries Inc. (NYSE: NPK) was founded in 1905 in Wisconsin. The company has long since produced a wide range of small cooking appliances, and in the past several years has made acquisitions to be a producer of small military products and adult absorbent products. The defense acquisitions have been the primary driver of growth.National Presto has been in business for over 100 years, and currently consists of three business segments:

Housewares/Small Appliance Segment

This segment accounts for 30% of revenue and 23% of operating profit, and producers a range of household small appliances, mostly kitchen-related, ranging from pressure cookers to deep fryers, to products for pizza.

Defense Products Segment

This segment accounts for 47% of revenue and 74% of operating profit, and produces 40mm ammunition for the Army, as well as fuses, cartridges, less-than-lethal products for law enforcement, and precision electro-mechanical assemblies.

Absorbent Products Segment

This segment accounts for 23% of revenue and 3% of operating profit, and produces adult diapers.

Stock Metrics

Price to Earnings: 11.2Price to Free Cash Flow: 12.2

Price to Book: 1.6

Return on Equity: 14%

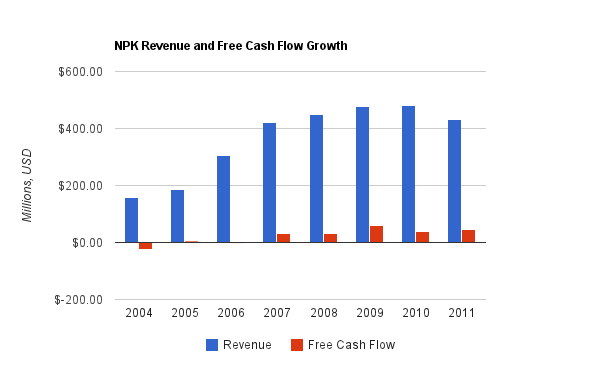

Revenue and Free Cash Flow

Revenue and free cash flow for National Presto have been rather erratic over the period. Management made excellently timed acquisitions of defense businesses during an early period of a long set of wars. In 2011, the company faced decreases in volume and profitability, especially in the appliances segment.

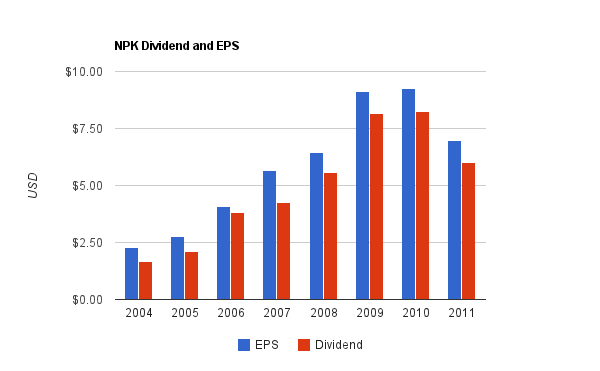

Earnings and Dividends

Earnings and dividends have been substantial due to smart value investment on the part of management, but in 2011, they finally ran into problems.

Special Dividend

National Presto is rather unique in its dividend policy. Once per year, they pay out approximately 90% of earnings as a combination of a regular and special dividend. There has been 68 unbroken years of dividends, although the total number of years of consecutive dividend growth was not nearly this long, and in 2011, they broke their streak and paid a smaller, but still rather large, dividend.What most blue-chip dividend growth businesses do is, they keep moderate dividend payout ratios, and use extra capital for share repurchases. Instead of doing that, National Presto pays out basically all of their free cash as dividends, which makes the dividend larger, but makes it less resilient to declines in earnings. If you take a look at the combined dividends and share repurchases of any dividend growth business, you’ll see that they grow and shrink with business conditions, even as the dividend segment continues to grow. NPK is the same, except that 100% of it is dividends, and so the dividend segment puts aside consistent growth in favor of pure dividend payouts.

Balance Sheet

National Presto’s balance sheet is almost too good. It’s kind of like Apple (AAPL), where they have so much cash, it could almost be viewed as a problem, albeit a good problem to have. They have continually held a rather enormous sum of cash on the balance sheet over the last decade. It’s a very large buffer against problems, and could support an acquisition opportunity at any time.With a market cap of under $550 million, the National Presto holds $133 million in cash and cash equivalents on their balance sheet. The company has zero debt, a rather small amount of goodwill, and a current ratio of around 5. The balance sheet, therefore, is perfect.

Investment Thesis

Sometimes dividend portfolios can be too concentrated in large-cap stocks. What I like to see is a small or medium sized company paying a dividend. National Presto Industries, Inc. is a quirky company that fits the bill.In addition, the long-tenured chairperson and CEO Maryjo Cohen currently owns an impressive chunk of the company. Her interests are therefore aligned with shareholders, and aligned with long term success rather than short term expectations. That explains why this has been such a shareholder friendly company over the last several years.

The conglomerate is value-oriented, with small overhead, fair and simple executive compensation, and plenty of insider ownership.

Management can allocate resources to make smart acquisitions, and tends to return most of the profits back to shareholders in the form of an annual special dividend.

Growth Areas

National Presto has had a disappointing 2011, but there are some potential areas for improvement.-In late 2011, the company acquired manufacturing assets of less than lethal ammunition. This includes tear gas grenades, specialty impact ammo, gas masks, and more, along with the associated training with these devices. Customers include law enforcement and corrections facilities. Annual sales are estimated at $7.5 million, and it’s good that this diversifies the defense segment a little bit away from the Department of Defense, and warfare.

-National Presto appliances could rebound from their poor 2011 performance. The CEO attributed much of the performance due to consumer and retailer habits mismatch, but also due to private label competition. National Presto will be introducing some new and exclusive products in 2012.

-I previously identified the absorbent products segment as a risk area due to the concentration of the customer base, but the company has begun successfully diversifying and growing their customer base.

-The company has $133 million, or approximately a quarter of the market capitalization, held in cash-equivalents. Low interest rates have been hurting them here, and so eventual increases in interest rates can provide better returns on this capital. Or, this can be viewed as substantial resources for smart acquisitions.

Risks

NPK has an odd risk profile. On one hand, their diversification into completely different markets provides risk reduction, and their products across all categories are very practical. Combined with a beautiful balance sheet and conservative and frugal management with large insider ownership, along with very large dividends, NPK has some stability.On the other hand, NPK does have a fair number of significant risks, and these risks have strongly demonstrated themselves in 2011.

Their appliance and absorbent products segments face commodity cost issues and have a concentrated customer base. There is little economic moat to speak of, so pricing power is limited, and private label products have been threatening NPK market share.

Their defense segment has irregular timing of contracts, so money doesn’t flow in regularly. The largest risk of all is how the defense segment (National Presto’s largest segment) is mostly reliant on the Department of Defense, which has been winding down operations. Some of the products are training related, as these are ammo and other types of products rather than, say, multi-billion-dollar fighter jet contracts, so there is some defensiveness there. In addition, the acquisition of less than lethal products for law enforcement is a smart one, in my view.

Still, the possibility of a major contract loss in this segment is probably the largest risk. That’s the one thing that could quickly turn this into a poor investment. I wouldn’t be surprised to see decreased profitability from this segment since margins are so high and will have to come down, and it appears that this is factored into the current stock price in the high $70”²s. There was a major five-year contract awarded to National Presto in 2005, and another major five-year contract awarded in 2010. The customer can cancel these contracts at their convenience.

The CEO has predicted the same troubles for 2012 as came to pass in 2011: high commodity and energy costs, and low interest rates.

Conclusion and Valuation

Over the last several years, I’ve had a rather small number of disappointing investments, and NPK has been one of them.In my analysis from last year, I discussed the risks, and many of them came to pass. Commodity costs impacted the absorbent products and appliance segments, in particular. I mentioned that they have a lack of moat, and therefore a lack of pricing power, and this has indeed been the case.

Some of my estimates have apparently been incorrect here. I had expected that a recession would indeed impact the business, but that if anything, consumers would eat at home more and dine out less to save money, and therefore would purchase more of National Presto’s appliances, or at least wouldn’t decrease their purchases too much. That has not been the case.

More particularly, CEO Cohen has stated that in addition to private label products taking market share from National Presto, part of the problem has to do with retailers and consumer habits, which is something I didn’t factor in. As she described it in a press release, customers are no longer stockpiling products such as National Presto small cooking appliances in advance. Instead, they are buying just when they need them. This has meant that retailers have kept inventories very low, so during the holiday season when they actually were to be purchased, consumers often found shelves empty. So a combination of private label competition and misaligned customer and retailer habits, have resulted in a larger impact to National Presto’s appliance segment than I had anticipated, and have more than offset my expectation that small cooking appliances would be rather defensive.

I’m still holding my position, but not increasing it. My current holding value is down considerably compared to my cost basis, but factoring in the large dividends received, my cost basis is not much lower than my initial investment. I have to reduce the fair valuation of the company, because valuation is based on growth rates, and while I had previously factored in modest growth, I can no longer do so.

Going forward, the company is currently priced for no growth. With a P/E and P/FCF of around 11 and 12, and even lower than that if a portion of the cash is factored out of the valuation, which is a common valuation practice, the company already has a lot of risk factored in.

If the business were to merely stay static from this point, the large single-digit dividend yield would provide a reasonable return. If National Presto were to lose substantial military contracts or face continued appliance decreases, then the investment could prove to be a poor one. I observe that assumed decline in defense profitability is factored into the stock price. On the other hand, if the company fixes a few problematic areas, keeps a substantial portion of its backlog of contracts, and continues to make smart acquisitions, modest long term growth combined with the dividend could result in solid returns.

Full Disclosure: I own shares of NPK.