Though it might seem absurd to value investors, there are market participants out there who buy (sell) securities only because they have gone up (down). They profess the superiority of momentum investing. Are they right?

In decades past, making such a determination was a laborious undertaking, available only to those academics with the time and inclination, and the financial firms with the scale to be able to profit from such an effort. Today, however, the proliferation of powerful computing tools has democratized this process. Below I discuss a quick test of momentum I conducted in the shares of a highly liquid (Apple) company, and one that isn't so liquid (Manhattan Bridge Capital).

When testing for momentum, the first thing one has to choose is the time period of the test. Are we testing momentum from minute to minute, month to month or year to year, for example? For this test, I chose something in the middle: day to day. In other words, the test is to determine whether a stock goes up the day after it has already gone up.

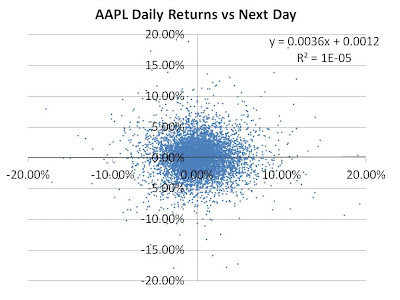

Thanks to the good people at Yahoo! (yes, the company still exists!), I was able to download the daily closing price of Apple shares from 1984 to today into a spreadsheet! I then plotted each day's return against the previous day's return. See a pattern?

Looks pretty random, and Excel's regression statistics confirm this finding. In other words, there is no reason to believe the correlation between one day's returns and the next day's returns is anything but 0.

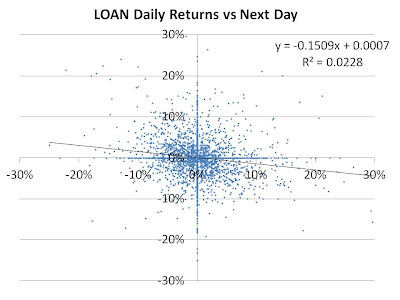

But take a look at the pattern now for the illiquid stock, Manhattan Bridge Capital (LOAN):

If you see a slightly negatively sloped line, you're not alone. Excel believes this correlation to be significantly different than 0. But wait, the correlation is actually negative! So this stock has experienced negative momentum! For every 1% move in LOAN one day, it can be expected to move 0.15% (with a large deviation of course) the next day in the opposite direction.

Though I was surprised by the result, it does make sense to a certain degree. A stock cannot simply "randomly walk" too far away from it's intrinsic value. At some point, market forces (short sellers, value buyers etc) will pressure a stock back to where it should be. Maybe that's what we're seeing with LOAN here. So much for positive momentum!

Humans, it seems, look for patterns in what they see, even if there aren't any. This has likely been a positive selective trait in our evolution (or for those of you creationists out there: God has given us both the ability and the eagerness to seek out patterns wherever we look). At the same time, we seem to put more emphasis on recent events (over older events) in extrapolating expectations into the future. As such, whether momentum in financial markets is shown to exist or not, many are likely to believe in it anyway.

(As an aside, consider how momentum is regarded in sports. Commentators, coaches, players and fans constantly expect better performances from the player(s) with the "hot hand". As discussed in the excellent book Scorecasting: The Hidden Influences Behind How Games Are Won, studies have shown that the hot hand doesn't exist in basketball (among other sports). A player's chances of making his next shot are unrelated to whether he has made his last 1, 2, 3, 4, 5+ shots! Has this discovery changed how sports are marketed/discussed/coached? To me, it would appear not.)

Of course, this is by no means a conclusive study proving momentum theories are false. But you now have the ability to test any momentum theory that is put in front of you, thanks to the advances of computing software and hardware. Go for it!

In decades past, making such a determination was a laborious undertaking, available only to those academics with the time and inclination, and the financial firms with the scale to be able to profit from such an effort. Today, however, the proliferation of powerful computing tools has democratized this process. Below I discuss a quick test of momentum I conducted in the shares of a highly liquid (Apple) company, and one that isn't so liquid (Manhattan Bridge Capital).

When testing for momentum, the first thing one has to choose is the time period of the test. Are we testing momentum from minute to minute, month to month or year to year, for example? For this test, I chose something in the middle: day to day. In other words, the test is to determine whether a stock goes up the day after it has already gone up.

Thanks to the good people at Yahoo! (yes, the company still exists!), I was able to download the daily closing price of Apple shares from 1984 to today into a spreadsheet! I then plotted each day's return against the previous day's return. See a pattern?

Looks pretty random, and Excel's regression statistics confirm this finding. In other words, there is no reason to believe the correlation between one day's returns and the next day's returns is anything but 0.

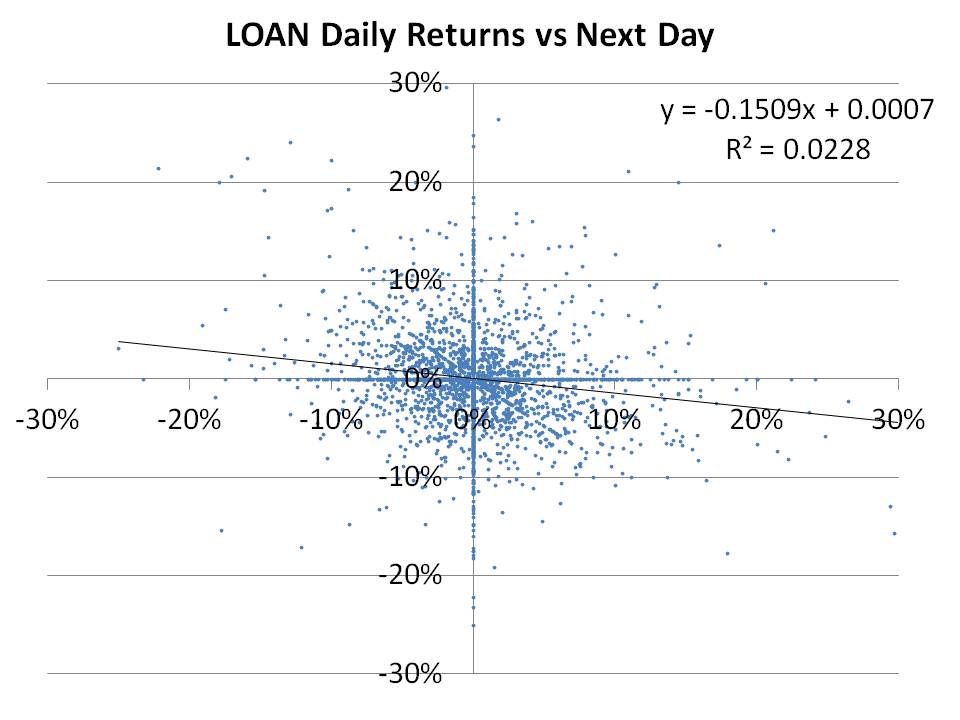

But take a look at the pattern now for the illiquid stock, Manhattan Bridge Capital (LOAN):

If you see a slightly negatively sloped line, you're not alone. Excel believes this correlation to be significantly different than 0. But wait, the correlation is actually negative! So this stock has experienced negative momentum! For every 1% move in LOAN one day, it can be expected to move 0.15% (with a large deviation of course) the next day in the opposite direction.

Though I was surprised by the result, it does make sense to a certain degree. A stock cannot simply "randomly walk" too far away from it's intrinsic value. At some point, market forces (short sellers, value buyers etc) will pressure a stock back to where it should be. Maybe that's what we're seeing with LOAN here. So much for positive momentum!

Humans, it seems, look for patterns in what they see, even if there aren't any. This has likely been a positive selective trait in our evolution (or for those of you creationists out there: God has given us both the ability and the eagerness to seek out patterns wherever we look). At the same time, we seem to put more emphasis on recent events (over older events) in extrapolating expectations into the future. As such, whether momentum in financial markets is shown to exist or not, many are likely to believe in it anyway.

(As an aside, consider how momentum is regarded in sports. Commentators, coaches, players and fans constantly expect better performances from the player(s) with the "hot hand". As discussed in the excellent book Scorecasting: The Hidden Influences Behind How Games Are Won, studies have shown that the hot hand doesn't exist in basketball (among other sports). A player's chances of making his next shot are unrelated to whether he has made his last 1, 2, 3, 4, 5+ shots! Has this discovery changed how sports are marketed/discussed/coached? To me, it would appear not.)

Of course, this is by no means a conclusive study proving momentum theories are false. But you now have the ability to test any momentum theory that is put in front of you, thanks to the advances of computing software and hardware. Go for it!