PR Newswire

SAN FRANCISCO, Dec. 15, 2022

Half of Consumers Say Inflation Has Diminished Their Capacity to Reach Their Long-Term Financial Goals

SAN FRANCISCO, Dec. 15, 2022 /PRNewswire/ -- LendingClub Corporation (NYSE: LC), the parent company of LendingClub Bank, America's leading digital marketplace bank, today released findings from the 17th edition of the Reality Check: Paycheck-To-Paycheck research series, conducted in partnership with PYMNTS. The Financial Goals Edition examines the motivations behind consumers' ability to save and plan for future large expenses as well as their long-term financial goals and expectations.

Today's Paycheck-to-Paycheck Landscape

Sixty-three percent of consumers reported living paycheck to paycheck in November 2022. Consumers of all income brackets are increasingly feeling the strain of inflation, and a growing share of high earners report living paycheck to paycheck. In November 2022, 47% of consumers earning more than $100,000 per year reported living paycheck to paycheck, a 4 percentage point increase from 43% in October 2022.

All income groups experienced a rise in paycheck-to-paycheck consumers between October and November 2022. In November 2022, 76% of consumers earning less than $50,000 annually were living paycheck to paycheck, compared to 74% the month prior, and 66% of consumers earning between $50,000 and $100,000 annually were living paycheck to paycheck, up from 65% the month prior.

Consumers Are Saving Less Overall

One-third of consumers report they are not currently saving any money, with 60% of such consumers also saying they have no pre-existing savings. While 36% of consumers overall describe themselves as stable savers, which are consumers able to save a fraction of their income on a regular basis (such as monthly or quarterly), paycheck-to-paycheck consumers are half as likely to be stable savers and seven times more likely to have neither savings nor saving capacity than other financial lifestyles. Forty-one percent of paycheck-to-paycheck consumers living without difficulty paying their bills are sporadic savers.

Financially struggling consumers report having significantly less savings than they had in 2021. In fact, half of financially struggling consumers are unable to save and have no savings at all. Compared to a year ago, 32% of all consumers have diminished saving capacity. For those consumers living paycheck-to-paycheck with issues paying their monthly bills, 42% say their ability to save has decreased, making them the group most likely to say so. This group is followed closely by paycheck-to-paycheck consumers living without difficulty, at 37%. Even among consumers not living paycheck to paycheck, 25% report that their ability to save has decreased.

"As we've seen from previous reports, Americans are cash-strapped and their everyday spending continues to outpace their income which is impacting their ability to save and plan," said Anuj Nayar, Financial Health Officer at LendingClub. "With average savings stagnating, if not decreasing, setting financial goals for the new year will become increasingly difficult for many consumers."

Inflationary Impacts on Short-Term and Long-Term Financial Goals

Inflationary pressures continue to weigh on consumers as they set both short-term and long-term financial goals. In fact, 50% of all consumers surveyed and 43% of those not living paycheck to paycheck say high inflation has diminished their capacity to reach their long-term financial goals. This increases to 57% among all paycheck-to-paycheck consumers. Inflation has also impacted the short-term objectives of 49% of all consumers and 41% of those not living paycheck to paycheck, with older consumers and those with lower incomes the most likely to say so.

Financial lifestyle is also a strong differentiator of the likelihood of having clearly defined financial goals. For example, financially struggling consumers are the most likely to lack both long-term and short-term financial goals. On top of that, more than a third (36%) of all U.S. consumers have not identified short-term financial goals, nor have 38% defined long-term objectives.

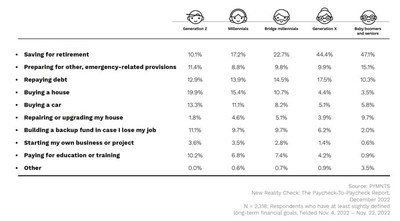

Saving for retirement is the main reason consumers – especially baby boomers, seniors and Generation X – set a long-term financial goal, with 33% of all consumers citing this as their most important motivation. Building up emergency savings is the second most common reason, yet only 11% cite it as their most important motivation. Repaying debt, cited by 14% of consumers, is the second-most important motivation for setting long-term financial plans.

While the main driver for consumers to set a long-term financial goal is saving for retirement, one-third of consumers overall cite repaying financial obligations as a short-term financial objective, with 18% citing this as their top short-term goal. The most common motivation for setting short-term financial goals overall is paying for a trip or vacation, which is cited by 49% of consumers, yet only 17% say it is their most important reason.

To view the full report, visit: https://www.pymnts.com/study/reality-check-paycheck-to-paycheck-financial-goals-consumer-savings-inflation/

Methodology

New Reality Check: The Paycheck-To-Paycheck Report — The Financial Goals Edition is based on a census-balanced survey of 3,895 U.S. consumers conducted from Nov. 4 to Nov. 22, as well as analysis of other economic data. The Paycheck-To-Paycheck series expands on existing data published by government agencies, such as the Federal Reserve System and the Bureau of Labor Statistics, to provide a deep look into the core elements of American consumers' financial wellness: income, savings, debt and spending choices. Our sample was balanced to match the U.S. adult population in a set of key demographic variables: 51% of respondents identified as female, 31% were college-educated and 36% declared incomes of more than $100,000 per year.

LendingClub Corporation (NYSE: LC) is the parent company of LendingClub Bank, National Association, Member FDIC. LendingClub Bank is the leading digital marketplace bank in the U.S., where members can access a broad range of financial products and services designed to help them pay less when borrowing and earn more when saving. Based on more than 150 billion cells of data and over $80 billion in loans, our advanced credit decisioning and machine-learning models are used across the customer lifecycle to expand seamless access to credit for our members, while generating compelling risk-adjusted returns for our loan investors. Since 2007, more than 4 million members have joined the Club to help reach their financial goals. For more information about LendingClub, visit https://www.lendingclub.com.

CONTACT:

For Investors: [email protected]

Media Contact: [email protected]

PYMNTS Contact: [email protected]

![]()

![]() View original content to download multimedia:https://www.prnewswire.com/news-releases/one-third-of-consumers-report-they-are-not-currently-saving-any-money-301703795.html

View original content to download multimedia:https://www.prnewswire.com/news-releases/one-third-of-consumers-report-they-are-not-currently-saving-any-money-301703795.html

SOURCE LendingClub Corporation