Starbucks Corp (SBUX, Financial) experienced a daily loss of -1.63 % and a 3-month loss of -4.67%. With an Earnings Per Share (EPS) of 3.28, the question arises: is the stock modestly undervalued? This article provides a detailed valuation analysis of Starbucks (SBUX) to answer this question. Keep reading to gain valuable insights into the company's financial performance and prospects.

Company Introduction

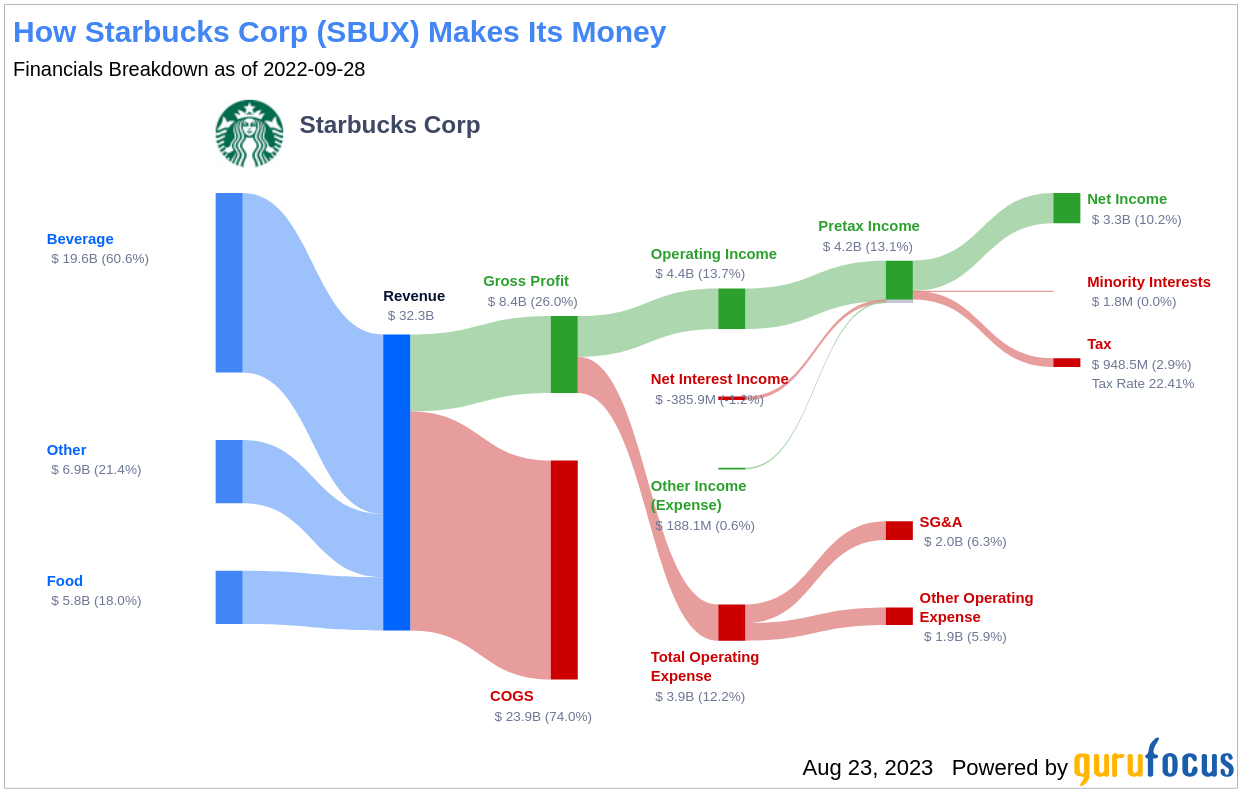

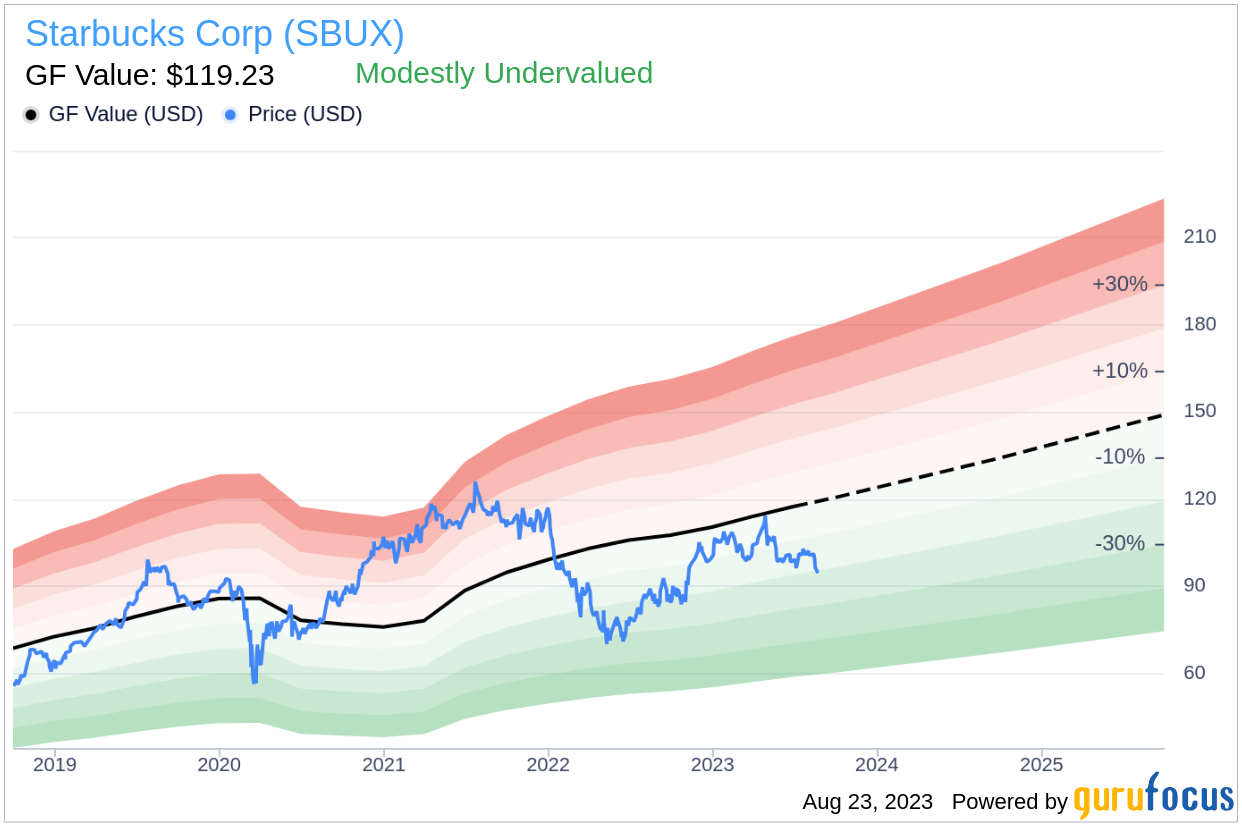

Starbucks is a globally recognized restaurant brand, operating nearly 36,000 stores across more than 80 countries. The company operates in three segments: North America, international markets, and channel development. It generates revenue from company-operated stores, royalties, sales of equipment and products to license partners, ready-to-drink beverages, packaged coffee sales, and single-serve products. With a current stock price of $94.5 and a GF Value of $119.23, Starbucks appears to be modestly undervalued.

Understanding the GF Value

The GF Value is a proprietary measure of a stock's intrinsic value, computed considering historical trading multiples, a GuruFocus adjustment factor based on past performance and growth, and future business performance estimates. The GF Value Line denotes the stock's ideal fair trading value.

Starbucks (SBUX, Financial) stock appears to be modestly undervalued based on the GuruFocus Value calculation. At its current price of $94.5 per share, Starbucks has a market cap of $108.20 billion, suggesting that the stock is modestly undervalued. Because Starbucks is relatively undervalued, the long-term return of its stock is likely to be higher than its business growth.

Financial Strength

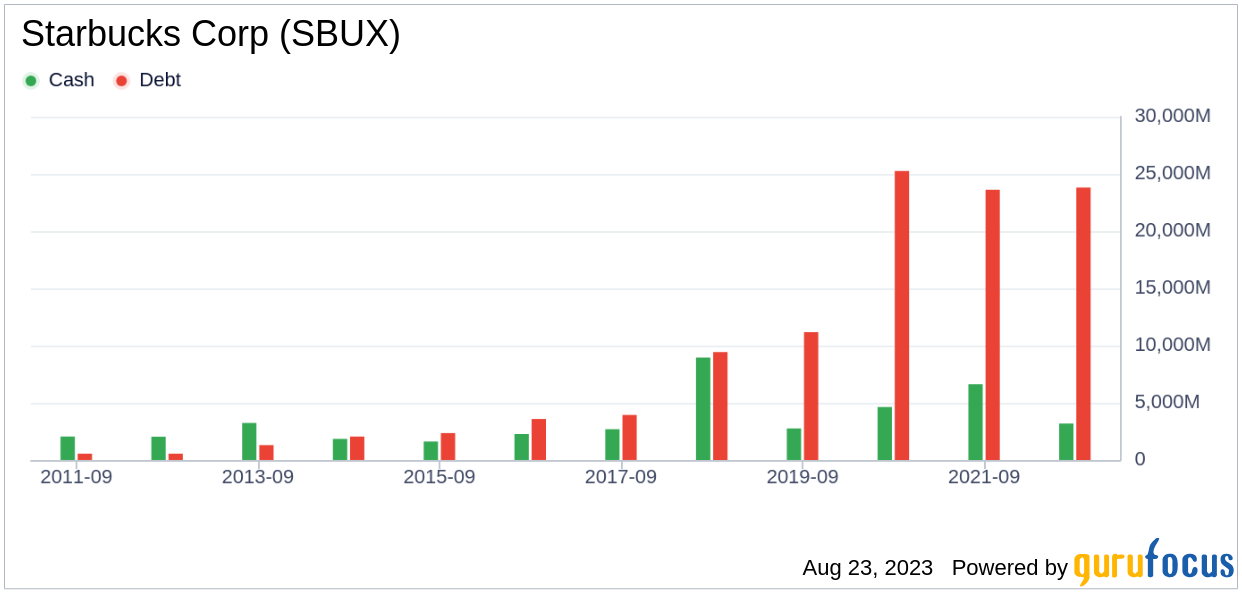

Investing in companies with low financial strength could result in permanent capital loss. Therefore, it's crucial to review a company's financial strength before deciding whether to buy shares. Starbucks has a cash-to-debt ratio of 0.15, which ranks worse than 70.89% of 347 companies in the Restaurants industry. Based on this, GuruFocus ranks Starbucks's financial strength as 5 out of 10, suggesting a fair balance sheet.

Profitability and Growth

Investing in profitable companies, especially those with consistent profitability over the long term, is generally less risky. Starbucks has been profitable 10 over the past 10 years. Over the past twelve months, the company had a revenue of $35 billion and Earnings Per Share (EPS) of $3.28. Its operating margin is 14.44%, which ranks better than 89.08% of 348 companies in the Restaurants industry. Overall, the profitability of Starbucks is ranked 9 out of 10, which indicates strong profitability.

Company growth is a crucial factor in the valuation of a company. The 3-year average annual revenue growth of Starbucks is 9%, which ranks better than 78.25% of 331 companies in the Restaurants industry. The 3-year average EBITDA growth rate is 2.1%, which ranks worse than 51.8% of 278 companies in the Restaurants industry.

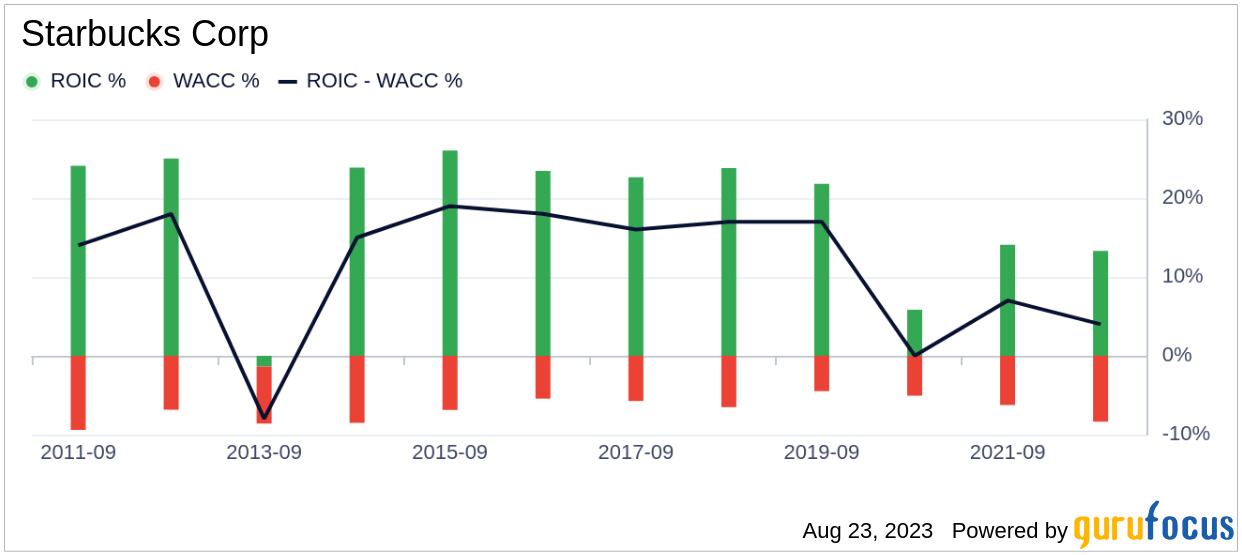

ROIC vs WACC

Another way to look at the profitability of a company is to compare its return on invested capital (ROIC) and the weighted cost of capital (WACC). For the past 12 months, Starbucks's return on invested capital is 14.79, and its cost of capital is 8.66.

Conclusion

Overall, Starbucks (SBUX, Financial) stock appears to be modestly undervalued. The company's financial condition is fair, and its profitability is strong. Its growth ranks worse than 51.8% of 278 companies in the Restaurants industry. To learn more about Starbucks stock, you can check out its 30-Year Financials here.

To find out the high-quality companies that may deliver above-average returns, please check out GuruFocus High Quality Low Capex Screener.