SolarEdge Technologies Inc (SEDG, Financial) recently experienced a daily loss of 2.85%, with a 3-month loss of 43.35%. Despite this, the company reported Earnings Per Share (EPS) of 5.17. This raises the question: is SolarEdge Technologies significantly undervalued? In this article, we will delve into the company's valuation analysis to answer this question.

Introduction to SolarEdge Technologies

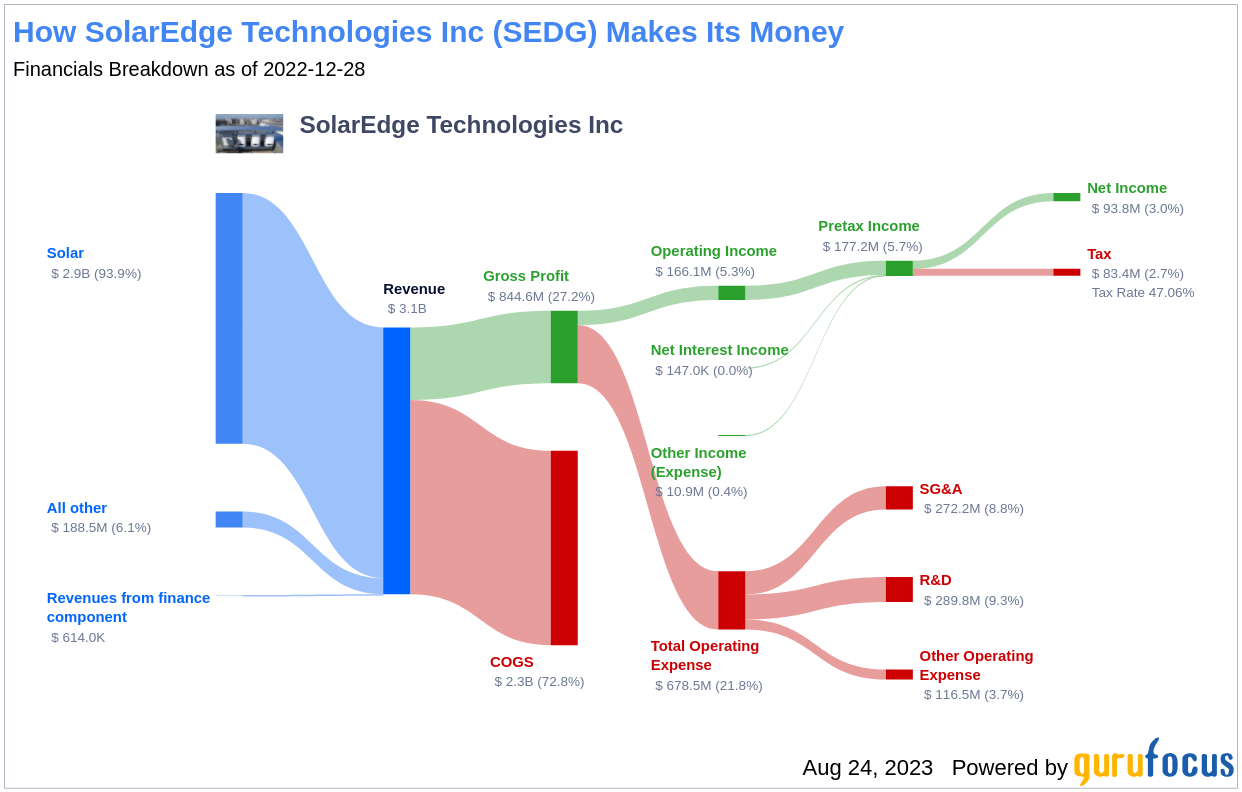

SolarEdge Technologies designs, develops, and sells direct current optimized inverter systems for solar photovoltaic installations. The company's system includes power optimizers, inverters, and a cloud-based monitoring platform. It caters to a broad range of solar market segments, from residential to commercial and small utility-scale solar installations. The company sells its products directly to solar installers, engineering, procurement, and construction firms, and indirectly through distributors and electrical equipment wholesalers. SolarEdge Technologies also offers nonsolar products targeting energy storage and e-mobility.

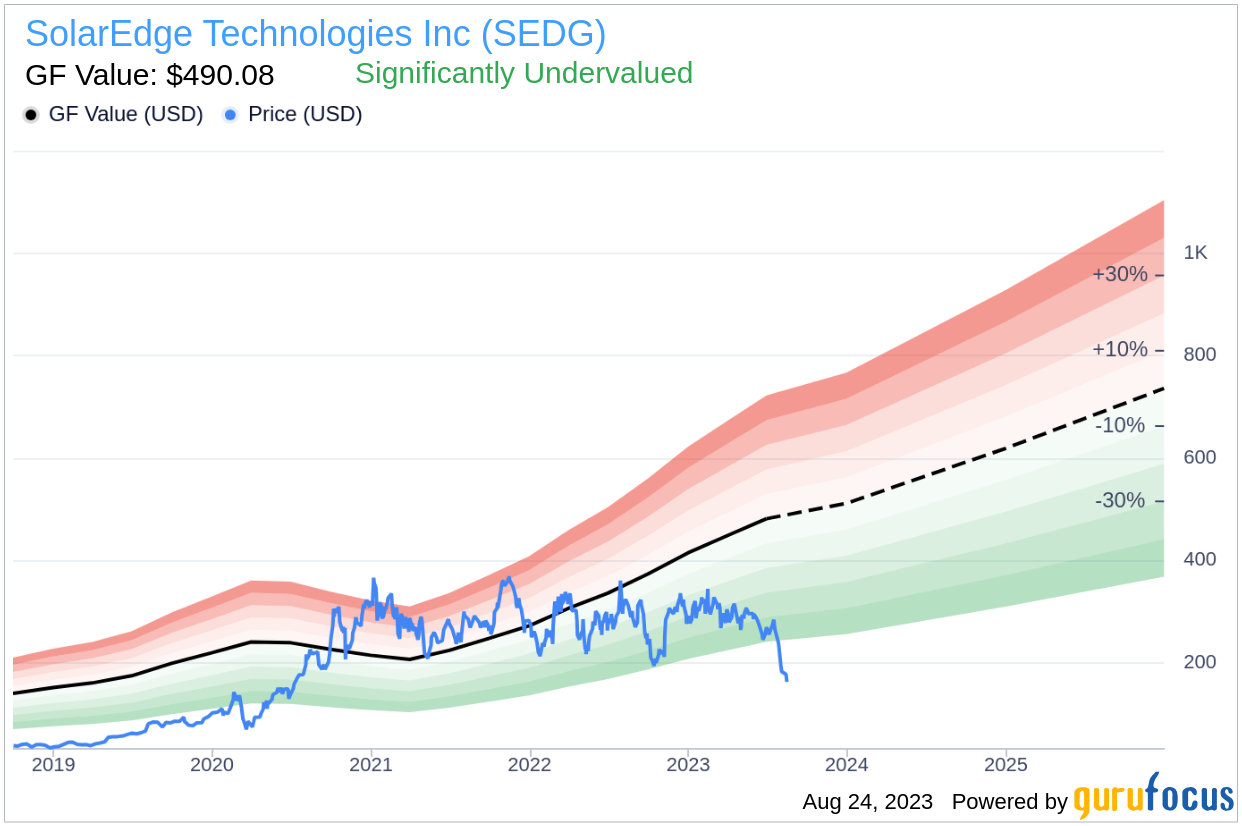

The company's stock price currently stands at $162.31, significantly lower than the GF Value of $490.08. This GF Value is an estimation of the stock's fair value, suggesting SolarEdge Technologies may be undervalued.

Understanding the GF Value

The GF Value is a proprietary measure that represents the current intrinsic value of a stock. It is derived based on historical multiples that the stock has traded at, a GuruFocus adjustment factor based on the company's past returns and growth, and future estimates of the business performance.

The GF Value Line on our summary page gives an overview of the fair value that the stock should be traded at. If the stock price is significantly above the GF Value Line, it is overvalued and its future return is likely to be poor. On the other hand, if it is significantly below the GF Value Line, its future return will likely be higher.

Given its current price of $162.31 per share, SolarEdge Technologies stock appears to be significantly undervalued. As a result, the long-term return of its stock is likely to be much higher than its business growth.

Link: These companies may deliver higher future returns at reduced risk.

Examining SolarEdge Technologies' Financial Strength

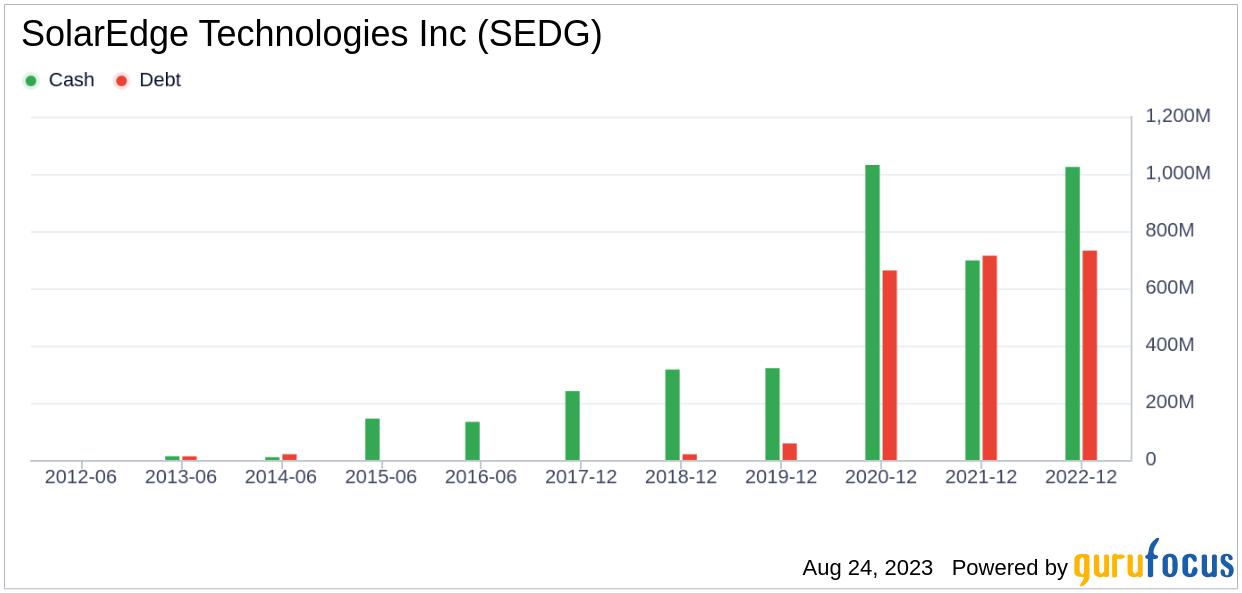

Investing in companies with poor financial strength carries a higher risk of permanent loss of capital. Therefore, it's crucial to carefully review a company's financial strength before deciding to buy its stock. A great starting point is looking at the cash-to-debt ratio and interest coverage.

SolarEdge Technologies has a cash-to-debt ratio of 1.43, which is worse than 57.07% of 820 companies in the Semiconductors industry. Despite this, GuruFocus ranks the overall financial strength of SolarEdge Technologies at 8 out of 10, indicating that its financial strength is strong.

Profitability and Growth of SolarEdge Technologies

Investing in profitable companies, especially those with consistent profitability over the long term, is generally less risky. SolarEdge Technologies has been profitable 8 out of the past 10 years. Over the past twelve months, the company had a revenue of $3.70 billion and Earnings Per Share (EPS) of $5.17. Its operating margin is 10.04%, which ranks better than 57.8% of 936 companies in the Semiconductors industry. Overall, the profitability of SolarEdge Technologies is ranked 8 out of 10, indicating strong profitability.

Growth is probably the most important factor in the valuation of a company. The faster a company is growing, the more likely it is to be creating value for shareholders, especially if the growth is profitable. The 3-year average annual revenue growth rate of SolarEdge Technologies is 23.5%, which ranks better than 74.68% of 865 companies in the Semiconductors industry. However, the 3-year average EBITDA growth rate is -0.9%, which ranks worse than 78.65% of 768 companies in the Semiconductors industry.

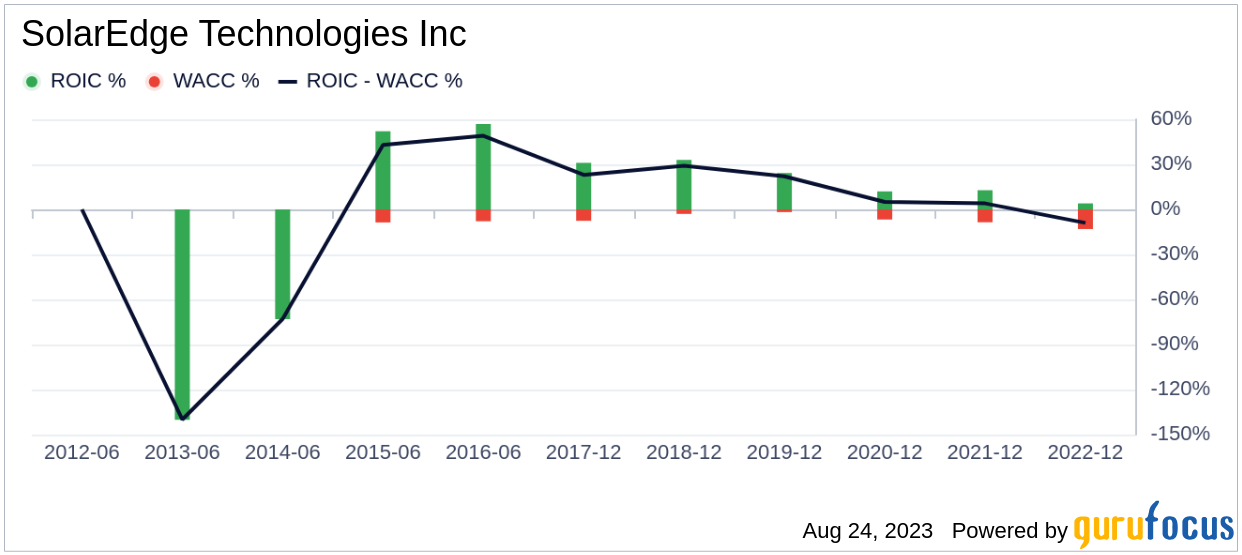

ROIC vs WACC

Another way to assess a company's profitability is to compare its return on invested capital (ROIC) with the weighted cost of capital (WACC). ROIC measures how well a company generates cash flow relative to the capital it has invested in its business. WACC is the rate that a company is expected to pay on average to all its security holders to finance its assets. For the past 12 months, SolarEdge Technologies's ROIC is 9.74, and its WACC is 11.14.

Conclusion

Overall, SolarEdge Technologies (SEDG, Financial) stock appears to be significantly undervalued. The company's financial condition is strong, and its profitability is strong. However, its growth ranks worse than 78.65% of 768 companies in the Semiconductors industry. To learn more about SolarEdge Technologies stock, you can check out its 30-Year Financials here.

To find out the high quality companies that may deliver above average returns, please check out GuruFocus High Quality Low Capex Screener.