Whirlpool Corp (WHR, Financial) has recently shown a daily gain of 2.22%, yet over the past three months, it has experienced a decline of 4.96%. With a notable Loss Per Share of 29.54, investors are faced with the critical question: Is Whirlpool modestly undervalued? This valuation analysis aims to delve into Whirlpool's financial nuances to provide an answer. We invite you to explore the following comprehensive analysis to understand the true value of Whirlpool Corp (WHR).

Company Introduction

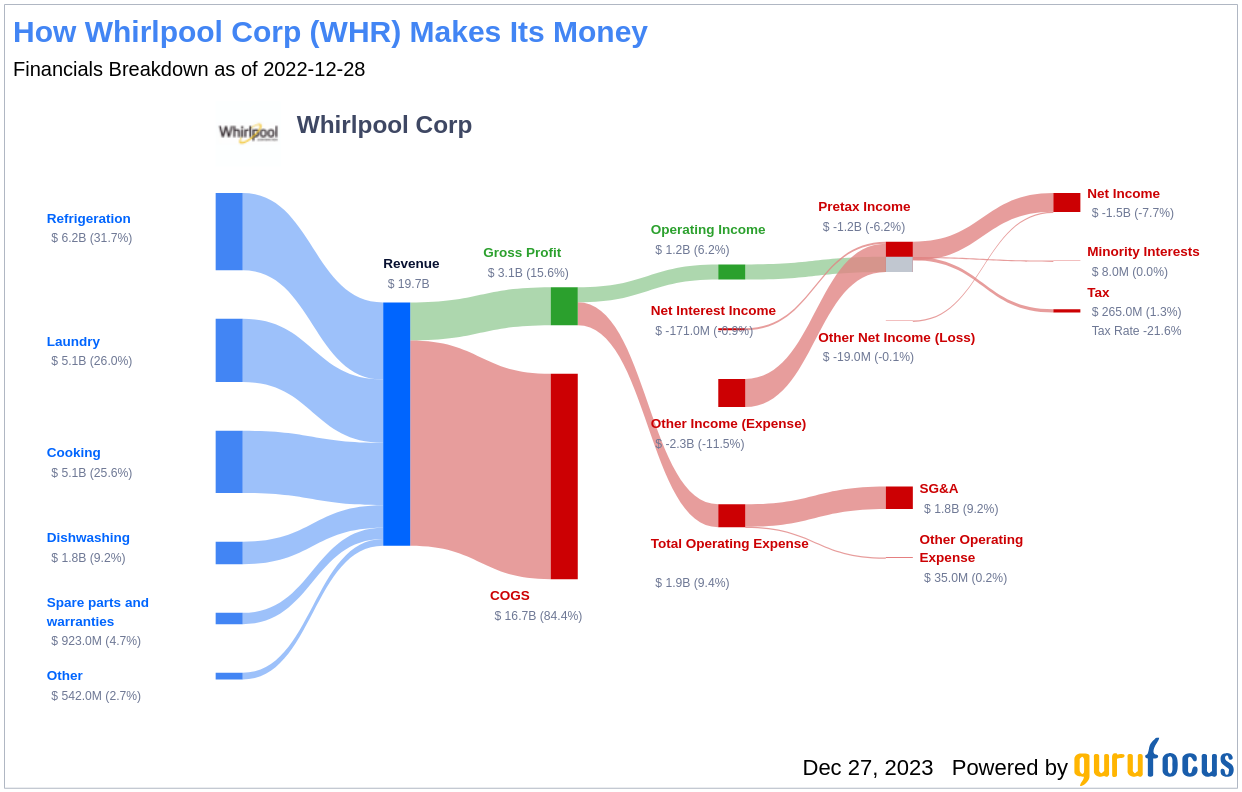

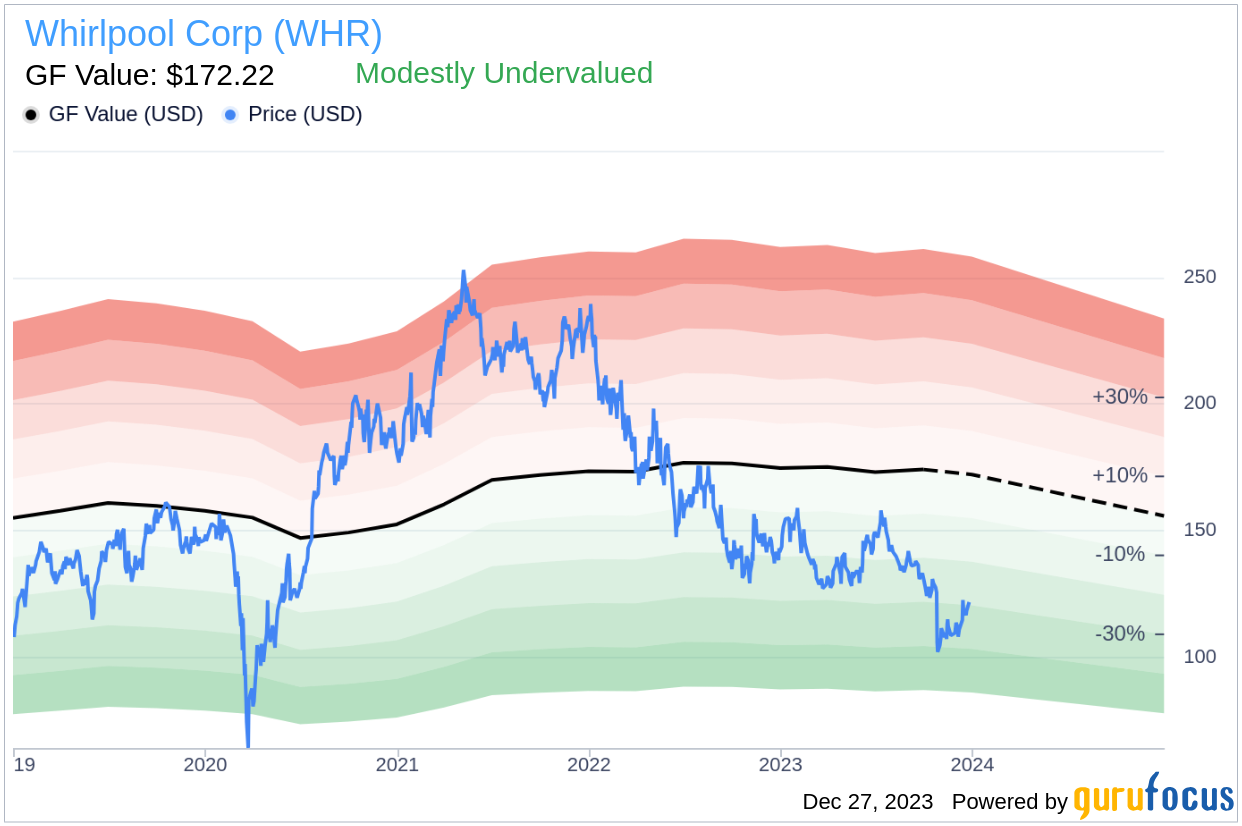

Whirlpool Corp is a prominent player in the home appliances market, with a diverse portfolio that includes refrigeration, laundry, cooking, and dishwashing products. It operates globally under renowned brands such as Whirlpool, KitchenAid, Maytag, Consul, and Brastemp. When comparing Whirlpool's current stock price of $121.78 to the GF Value of $172.22, a measure of its estimated fair value, there appears to be a significant discrepancy. This comparison suggests that Whirlpool might be trading below its intrinsic value, warranting a deeper investigation into its financial standing and market performance.

Summarize GF Value

The GF Value is a proprietary metric that represents the intrinsic value of a stock based on historical trading multiples, a GuruFocus adjustment factor, and future business performance estimates. Whirlpool (WHR, Financial) stock appears to be modestly undervalued according to this calculation. With a market cap of $6.70 billion, the stock's price suggests a potential for higher long-term returns relative to its business growth. The GF Value serves as a benchmark, indicating that stocks priced significantly below it may offer better future returns.

Link: These companies may deliver higher future returns at reduced risk.

Financial Strength

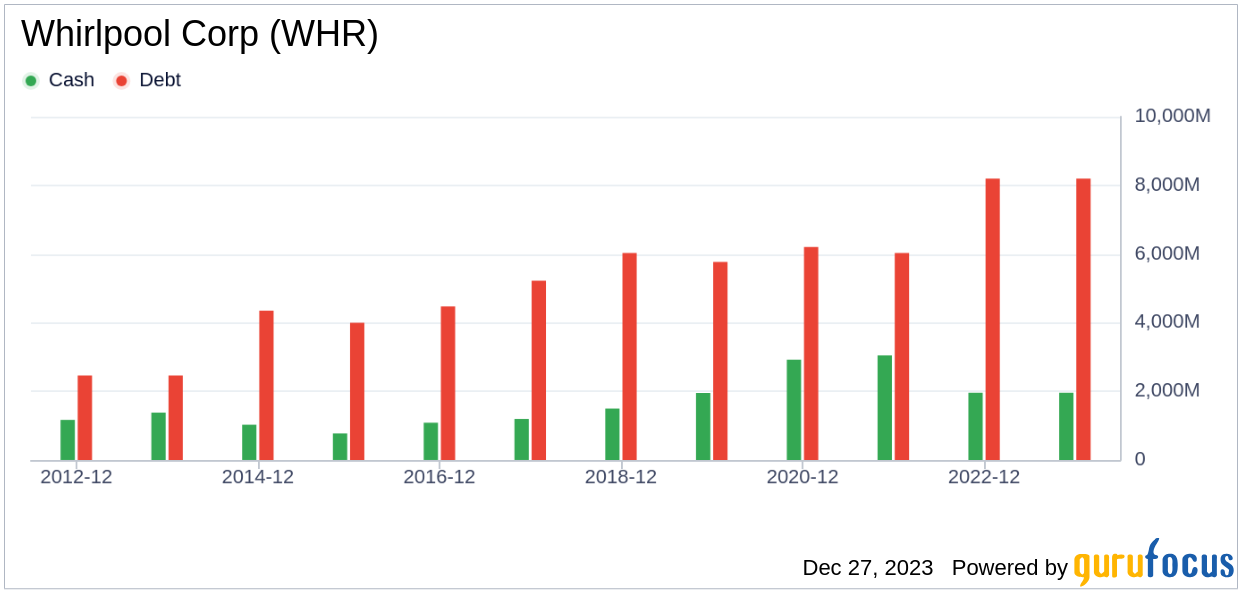

Investors must assess a company's financial strength to mitigate the risk of permanent capital loss. Whirlpool's cash-to-debt ratio of 0.14 ranks lower than the majority of its industry peers, suggesting a weaker financial position. The company's overall financial strength is rated as 4 out of 10, highlighting potential concerns regarding its financial robustness.

Profitability and Growth

In terms of profitability, Whirlpool has maintained profitability for 8 out of the past 10 years. With an operating margin surpassing half of its industry competitors, the company's profitability stands as fair. However, Whirlpool's revenue and EBITDA growth rates over the past three years have been less impressive, falling behind more than half of the companies within the industry.

ROIC vs WACC

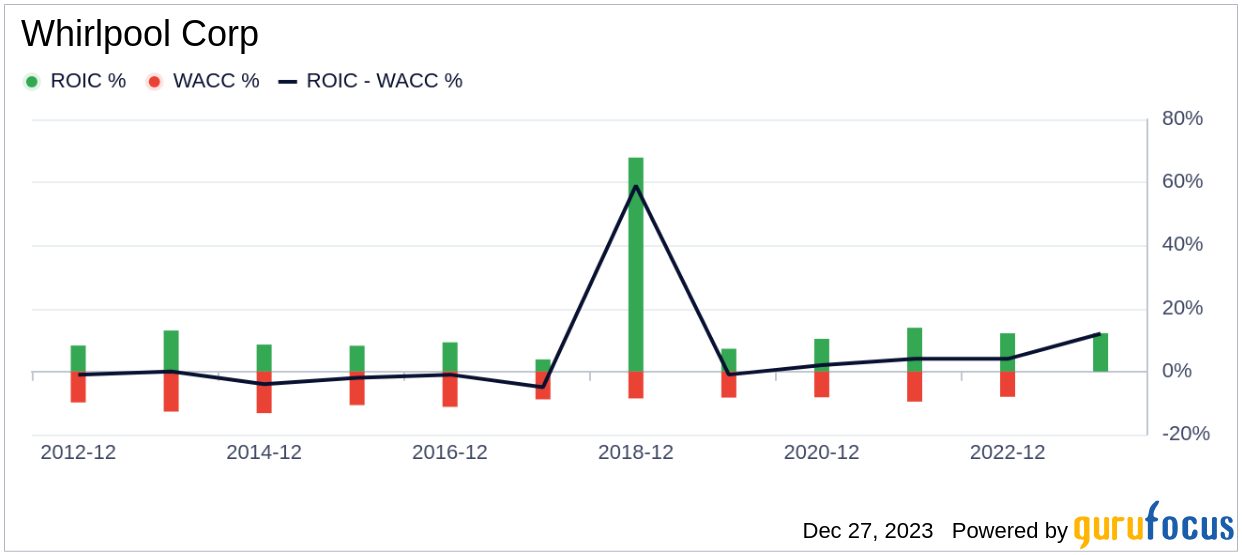

An essential aspect of profitability analysis is comparing a company's Return on Invested Capital (ROIC) with its Weighted Average Cost of Capital (WACC). Whirlpool's ROIC of 10.21% exceeds its WACC of 7.61%, indicating efficient capital utilization and promising value creation for shareholders.

Conclusion

In conclusion, Whirlpool (WHR, Financial) presents signs of being modestly undervalued. While the company's financial condition raises some concerns, its profitability remains reasonable. However, its growth performance does not compare favorably with industry standards. For a more detailed financial overview of Whirlpool, you can explore its 30-Year Financials here.

To discover high-quality companies that may offer above-average returns, please visit the GuruFocus High Quality Low Capex Screener.

This article, generated by GuruFocus, is designed to provide general insights and is not tailored financial advice. Our commentary is rooted in historical data and analyst projections, utilizing an impartial methodology, and is not intended to serve as specific investment guidance. It does not formulate a recommendation to purchase or divest any stock and does not consider individual investment objectives or financial circumstances. Our objective is to deliver long-term, fundamental data-driven analysis. Be aware that our analysis might not incorporate the most recent, price-sensitive company announcements or qualitative information. GuruFocus holds no position in the stocks mentioned herein.