Most great investments are easy to understand, and Bio-Reference Labs (BRLI) fits the bill.

Bio-Reference Labs perform clinical laboratory diagnostic services which includes tests such as blood and urine analysis, hematology services, tissue analysis and cancer cytogenetic testing with most of the revenue coming from the New York metropolitan area.

Here are five reasons why Bio-Reference Labs is a solid business and worth putting on your buy or waiting list.

1. A Strong and Resilient Business

The business model is recession proof ,as companies will continue to use the services of a company such as Bio-Reference Labs to perform tests on their employees and potential employees.

Bio-Reference Labs has been increased revenue every year since 1993 with an average gross margin of 49.7%. In the past five years, the average gross margin has been 51%, which clearly indicates how strong this business is.

Despite the fact that the clinical labs industry is fragmented, there clearly is a competitive advantage at work here.

2. Solid Fundamentals with Excess Returns

Check out these numbers

A CROIC of 24.7% shows that BRLI is able to generate 20 cents of every $1 of owner earnings used to invest.

The balance sheet is healthy with a quick ratio of 3 and minuscule debt ratio of 4%.

3. Excellent Quality of Accounting and Earnings

When I look at a company, I want to make sure that the company is not manipulating its numbers.

I check earnings quality and accounting using several measures.

The Piotroski Score is a scoring system based on checking nine accounting principles compared to the prior year.

BRLI scores a perfect 9 for the Piotroski score.

The Altman Z score signals how likely a company it is that a company will go bankrupt within a couple of years.

BRLI has a strong balance sheet, and there is no risk of bankruptcy.

The Beneish M Score is a financial model based on detecting earnings manipulation.

Again, BRLI is completely in the green — no signs of accounting manipulation.

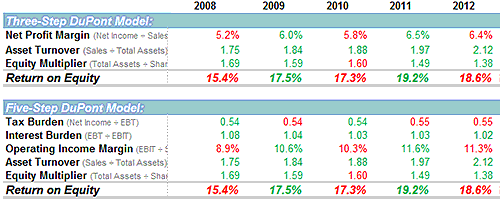

The fourth part of checking earnings quality is by using the DuPont analysis method to break down ROE to see how the company is achieving its current numbers.

With the DuPont analysis, you want to make sure that ROE is not increased due to debt. Remember that an increase in debt will also increase ROE.

ROE has remained at an above-average level due to consistent margins, increase in asset turnover and decreases in the equity multiplier.

All are very healthy signs.

(click to enlarge)

4. Good Insider Ownership

Management has done a good job with the business. Accounting is the language of business and the numbers show that BRLI has been very well managed and executed.

With an insider ownership of over 11%, with the CEO owning 10%, it shows that insiders are committed to the business and will act in the interest of shareholders.

The founder still runs the business and is chairman and CEO.

5. Best of Breed Company

BRLI really only has two main public competitors. There are other small and specialized competitors, but it wouldn't be comparing apples to apples.

Here is an image showing how well BRLI stacks up against its much bigger competition.

Valuation Targets

Looking at how stable the company is, projecting future cash flow and earnings will be easier.

Using the Old School Value valuation tools to value BRLI, here are the valuation numbers that I get.

The current price of $26 is within this range and shows that it is priced around fair value.

As much as I like the company, without a big enough margin of safety, I will just have to wait for BRLI to come back down.

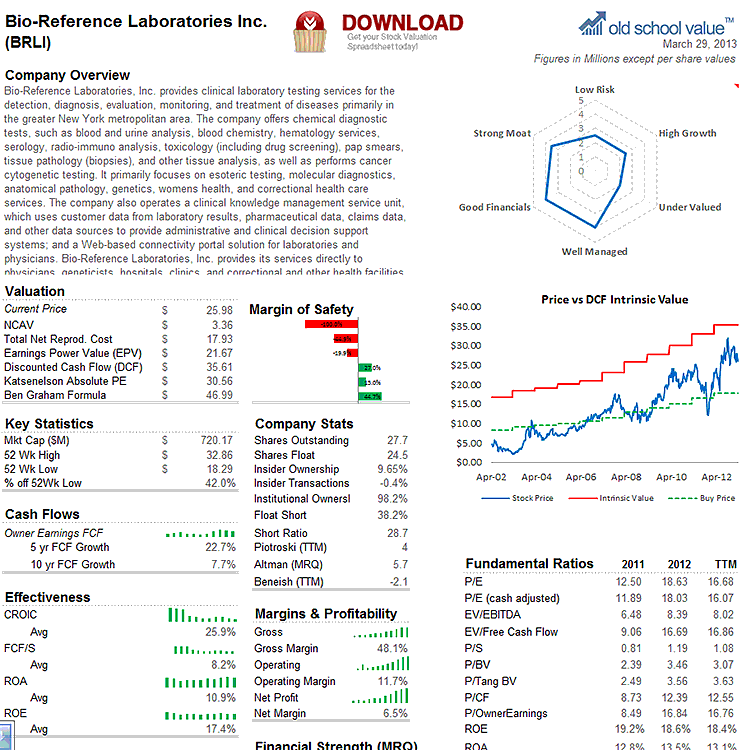

Here's an overview of BRLI.

Disclosure

No position

Bio-Reference Labs perform clinical laboratory diagnostic services which includes tests such as blood and urine analysis, hematology services, tissue analysis and cancer cytogenetic testing with most of the revenue coming from the New York metropolitan area.

Here are five reasons why Bio-Reference Labs is a solid business and worth putting on your buy or waiting list.

1. A Strong and Resilient Business

The business model is recession proof ,as companies will continue to use the services of a company such as Bio-Reference Labs to perform tests on their employees and potential employees.

Bio-Reference Labs has been increased revenue every year since 1993 with an average gross margin of 49.7%. In the past five years, the average gross margin has been 51%, which clearly indicates how strong this business is.

Despite the fact that the clinical labs industry is fragmented, there clearly is a competitive advantage at work here.

2. Solid Fundamentals with Excess Returns

Check out these numbers

- 5 year ROIC of 18.7%

- 5 year ROE average of 17.6%

- 5 year CROIC of 24.7%

A CROIC of 24.7% shows that BRLI is able to generate 20 cents of every $1 of owner earnings used to invest.

The balance sheet is healthy with a quick ratio of 3 and minuscule debt ratio of 4%.

3. Excellent Quality of Accounting and Earnings

When I look at a company, I want to make sure that the company is not manipulating its numbers.

I check earnings quality and accounting using several measures.

The Piotroski Score is a scoring system based on checking nine accounting principles compared to the prior year.

BRLI scores a perfect 9 for the Piotroski score.

The Altman Z score signals how likely a company it is that a company will go bankrupt within a couple of years.

BRLI has a strong balance sheet, and there is no risk of bankruptcy.

The Beneish M Score is a financial model based on detecting earnings manipulation.

Again, BRLI is completely in the green — no signs of accounting manipulation.

The fourth part of checking earnings quality is by using the DuPont analysis method to break down ROE to see how the company is achieving its current numbers.

With the DuPont analysis, you want to make sure that ROE is not increased due to debt. Remember that an increase in debt will also increase ROE.

ROE has remained at an above-average level due to consistent margins, increase in asset turnover and decreases in the equity multiplier.

All are very healthy signs.

(click to enlarge)

4. Good Insider Ownership

Management has done a good job with the business. Accounting is the language of business and the numbers show that BRLI has been very well managed and executed.

With an insider ownership of over 11%, with the CEO owning 10%, it shows that insiders are committed to the business and will act in the interest of shareholders.

The founder still runs the business and is chairman and CEO.

5. Best of Breed Company

BRLI really only has two main public competitors. There are other small and specialized competitors, but it wouldn't be comparing apples to apples.

Here is an image showing how well BRLI stacks up against its much bigger competition.

- Priced at a very slight premium

- Strong earnings growth in the past and expected

- Great business returns as mentioned above

- Fabulous financial position

- Lacks in the margins area compared to competitors but that could be due to economies of scale

Valuation Targets

Looking at how stable the company is, projecting future cash flow and earnings will be easier.

Using the Old School Value valuation tools to value BRLI, here are the valuation numbers that I get.

- DCF: Conservative target price of $26 with a more normalized target of $35

- Ben Graham Growth valuation: Conservative price of $39 and a more normal target price of $46

- Absolute PE valuation method: Fair value of $30 with a fair value PE being 19.6

- EBIT valuation: Conservative price of $23.9 with a more optimistic fair value of $39.

The current price of $26 is within this range and shows that it is priced around fair value.

As much as I like the company, without a big enough margin of safety, I will just have to wait for BRLI to come back down.

Here's an overview of BRLI.

Disclosure

No position