Apollo Group Inc. (APOL, Financial) provides online and on-premise educational programs and related services to undergraduate, masters and doctoral students.

The company is best known for the University of Phoenix, which in 2012 constituted 89% of revenues and 100% of operating profits. The remaining 11% of revenue comes from Apollo Global, which consists of a few small universities in Latin and South America and one in the UK.

With an EV to EBITDA valuation of only 1.6, it is safe to say that Apollo Group has a lot of negativity priced in and is now trading at a rock-bottom valuation. Despite criticism and headwinds in the for-profit education sector in general, the long-term prospects for higher education remain bright. This coupled with organizational reforms and a shifting strategy at Apollo make it increasingly likely that the company will bounce back strongly within the next few years.

Note: All Financial details referenced in this article can be found in the company's latest 10-K filing or most recent Q2 2013 conference call.

Company Overview

The University of Phoenix is probably the best-known for-profit education institution in America. The University was founded by Dr. John Sperling in 1973, after the educator was frustrated with the lack of study programs that suited working adult students who were often treated as second class citizens on many campuses. Nearly 40 years running, and the university is one of the largest educators in North America. However enrollments have dropped drastically in the past few years, from about 460,000 students in 2010 to only 357,000 in 2012 according to the most recent annual report. In the second quarter conference call at the end of March 2013, CEO Gregory Cappelli reported that enrollments were down to about 301,000 students, a 20% year-over-year drop. Financially speaking revenues have dropped about 15% in this period, and earnings, FCF/share and operating margins have all fallen as well. These metrics over the past three full fiscal years are summarized below:

Over the past 10 years the company grew FCF and EBITDA by more than 13% annually (even including the recent down years), and it has only been very recently that business has taken a turn for the worse. Hammering this home has been the rapid fall in share price from about $64/share in August 2010 to the current level of $17.41/share in May 2013.

Difficult Times in the For-Profit Education Sector

So what has caused this drastic change in fortunes for Apollo? Part of the trouble has been some harsh rhetoric and politicking out of Washington on the industry, as the federal government has taken a hard line against for-profits, claiming deceptive marketing practices and other aggressive tactics to attract students. Increasing enrollments was a number one priority at many of these institutions over the years, as this increased revenues (via federal loans) and thereby improving profits. As described more in the risk section below, students at for-profit institutions have traditionally relied heavily on federally funded financial aid packages. Due to high dropout rates and lower graduation figures than the non-profit education sector, the federal government has come down very hard on the industry recently. A lot of this negative publicity coupled with the rising costs of education has been the primary driver in a drastic decrease in enrollment starts.

Despite Challenges, Long-Term Prospects for Higher Education Remain Bright

Looking at the broader picture, however, and at the continuing challenges in America for higher education, recently the University of Phoenix released a very detailed report. In this report I believe the University has made a very good case that in order to continue to compete successfully in an ever increasing global environment, the U.S. really needs to get serious about more focused education and to provide specific training to ensure students have the right skills. The university's strategy which focuses more on part-time adult students to help retrain and improve their skills to be more relevant in the marketplace is a logical method to help close the current gap. The report goes in depth to explain how America is behind other major developed nations by more than 100 million years of education, which is leading to a loss of economic productivity. This gap sounds huge in real terms, but put in perspective it can virtually be made up entirely if all Americans were to simply spend an extra one year on higher education than they currently do.

Interestingly, if you read the Obama Administration's vision on higher education you will find striking similarities to the report referenced above from Apollo. The federal government also recognizes the skill gap, and President Obama has also set a goal that by 2020 every American should commit to at least one year of post-secondary training or higher education.

Although there is a lot of criticism on for-profit universities including the University of Phoenix, the bottom line is that everyone seems to recognize there is a growing problem in America and a gap between the skills that workers have and what the increasingly demanding global economy needs.

If you ignore for a moment all the noise coming out of Washington politicians on this industry, I think it becomes clear that in order to reach these goals to improve education overall, the for-profit section including University of Phoenix will be part of the picture. This is especially true because the government is advocating every American to commit to "at least one year" of post-secondary training. For many people this could be vocational-type training or associate's degrees which they might look to do online or in non-traditional manners. The University of Phoenix has one of the most extensive online education systems available, and is in the "sweet spot" so to speak in order to target and take on these types of students.

The Company Is Changing Its Strategy to Adapt to the New Realities

On the second quarter conference call results showed a continued rapid deterioration of student enrollment, and the company indicated that the start of the third quarter was also trending down at a similar rate of decline. For the full year 2013 operating profits excluding special charges are supposed to be about $525 million, or a margin of just over 14%. So this is a slowdown in margin decline from last year, but is still negative. To counter this, costs are being trimmed to the tune of $350 million in savings through 2014 and the organization is becoming leaner with fewer campuses. Although it takes some time to stop the bleeding, by significantly reducing its cost base Apollo is putting itself in a better position to turnaround.

In my opinion, the company management is listening to and learning lessons from the intense criticism the industry has received in the past few years. It's in the midst of restructuring and repositioning the University of Phoenix brand and does expect enrollment starts to return to positive territory in the near future, although whether that is late 2013 or 2014 is not clear. In the past few conference calls management has discussed strategic initiatives which are underway in order to improve the student experience and help students find jobs. This includes initiatives like their interactive career portal, which more than 25% students are already using and they are adding employers to this portal aggressively in order to better connect students with prospective jobs after graduation.

There are now 2,200 corporate partnerships and a strong focus on education to careers. The increased emphasis on industry partnerships seems to be gaining real traction: Back in October 2012 when I first researched Apollo, it reported 1,800 such partnerships, which means in only six months this has increased by more than 20%. The emphasis seems to be clearly shifting away from just spending resources on marketing to lure in students (and their financial aid money), and really focusing strongly on improving graduation and drop out rates.

In addition to this the company is focusing not only on degree granting programs, but also on vocational and certificate granting programs. This plays to the company’s core strengths in attracting working adults who want to acquire tangible skills for their jobs but don’t necessarily need a four-year degree. Eighty million adults in the U.S. don’t have a bachelor’s degree, and of those 50 million never tried to get one, so there is ample room for growth in this market.

In summary I see that the long term prospects of the higher education industry will remain positive, and the University of Phoenix is poised to be part of this. With more than 300,000 enrolled students, the University is a major force in education. The for profit industry as of 2010 had 2.4 million enrollments, which out of approximately 20 million higher education students in the US this is greater than 10%. So this industry is not just going to disappear, especially with the demand for more higher education continuing to grow.

Financial Strength

The company reported to have over $821 million in unrestricted cash in the most recent quarter vs. about $91m of debt. With a debt/equity ratio of less than 0.10 and an interest coverage ratio of over 50, the company is clearly in no near term risk of financial problems. This gives the company a lot of flexibility in being able to restructure itself quickly or also buyback more shares, which the company has done consistently over the past 10 years, as discussed below in more detail in the valuation section.

Management

The University of Phoenix was founded by now Exec. Chairman Dr. John G. Sperling (Ph.D), in 1973. An interesting note is that Dr. Sperling is still at it - at the young age of 91! A former professor at San Jose State, he founded The University of Phoenix with a goal in mind to better reach out to students who had a desire to work and study part time, a trend that was growing significantly at the time. Dr. Sperling currently holds the position of Chairman emeritus. His son Peter Sperling is the acting chairman of the board, having held various executive positions since 1983 at the company. The Sperlings together own about 2.5% of the company. Collectively insiders do hold about 13% of the company.

The CEO of Apollo, Gregory Cappelli, has been at the company since 2007 and has held the position of CEO since 2009. Initially he was co-CEO, but Charles Edelstein retired in mid-2012. Interestingly, the 44 year old was a managing director and research analyst at Credit Suisse and Abn Amro previously, so he should be well in tune with Wall Street and the investment business in general and bodes well for his credibility in terms of capital allocation decisions. Although Cappelli has taken the reigns at a very tough time in the industry, he has so far continued to make very rational and tough decisions and has stuck to them. This includes: $350 million in cost savings including the closing of many campuses, changes to marketing practices, having a new focused strategy on improving graduation rates and connecting students with prospective employers, and finally the smart decision to buy back significant amounts of stock at very cheap prices. In summary I think the management of the company is solid, and I don’t see any reasons to be majorly concerned on this front.

Valuation

With an EV/EBITDA of 1.6, Apollo is clearly cheap. The company still generates a lot of cash, has relatively low capital expenditures and has a very solid balance sheet. FCF/share is currently projected to be close to $3.40/share for FY13. Discounting this at a conservative 12%, with 0% projected growth over 10 years, and the fair value is $25.40/share, a margin of safety of more than 30%. This assumes 0% terminal growth as well. When you consider the more than $6/share in net cash on the balance sheet, there seems to be an upside potential of 50-75% to fair value from current prices.

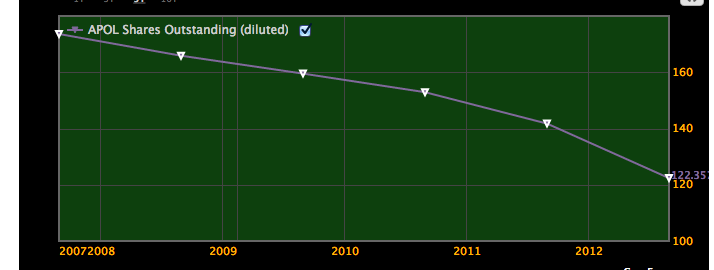

Of course this assumes that the company can stop the bleeding and stop the decreases in enrollments. I think several factors make it exceedingly likely that long term at least 0% growth is achievable. For one, as discussed above. long term prospects in demand for higher education continue to be positive. Global spend is expected to grow 7% annually from 2012 to 2017. In addition, the company has a fresh $250 million share buyback program that is authorized, and the company should continue to retire shares and increase EPS by several percent per year this way. Outstanding shares have decreased from about 170 million to 122 million over the past five years, an annual decrease of almost 7%, as shown in the figure below. With an earnings yield at a ridiculous 46%, the company cannot really get any cheaper based on fundamentals.

Investment Risks

Shareholder control - Interesting to note is that the company has two classes of shares, Class A and B. The common stock, Class A shares which are available for purchase on the open market actually have no voting rights. The voting rights are exclusively held by Class B shares, which are all owned by the Executive Chairman Dr. Sperling and his son Peter Sperling (who is vice chairman of the board). If Dr. Sperling passes away, his voting rights pass to three trustees which are all current directors on the board (his son and two others). I don’t see this is a major negative for an investment in the company, but it surely is a negative in the sense that it keeps off the pressure from activist shareholders or other big investors who might positively influence the capital allocation strategies of Apollo going forward. That being said, so far CEO Cappelli seems to be doing a reasonable job here and I don’t see any cause for concern.

Access to Title IV funding remains a constant threat - One important aspect to understand about the University of Phoenix as well as other for-profit universities is that they receive most of their revenue from student financial aid, much of which comes from the U.S. government. Under the 90/10 Rule as part of the Higher Education Act, for-profit educational institutions must receive at least 10% of their funding from non-governmental sources, and can receive a maximum of 90% from Pell Grants and federal student loans. If an institution breaches this rule 1 year, it must comply the following year or it will lose access to all financial aid. Many of these institutions are very close to the 90% threshold currently.

In 2012 the University of Phoenix generated 84% of revenue from Title IV financial aid program funds, coming very close to the limit. The good news is that this has dropped from 86 and 88% in 2011 and 2010 respectively.

The community college push - The Obama Administration has publicly declared its preference for community colleges over the for-profit sector. Obviously, Apollo cannot compete on price alone here. The company must continue to stay relevant in order to stop losing market share, and it must prove that its programs are worth the money for many students because of the additional benefits that they offer compared to cheaper alternatives. This is a constant risk going forward and is a perception that the company must be on top of in order to keep its place in the higher education segment.

The Bottom Line

In conclusion, I think an investment in Apollo today is an incredible value for the money. The company is about as cheap as it gets in terms of earnings yield and is trading significantly below historical averages. Using any standard valuation techniques with conservative growth assumptions and it is easy to justify that the company is undervalued by at least 50% to 100%. With an additional $250 million authorized for share buybacks, and the company’s history of repurchasing large amounts of shares, look for continued inorganic growth in EPS of 5% or more in the coming year based on this alone. Although further declines in enrollments will probably offset this in the near term, if the company can show any signs of a turnaround in the decline rate ( which it is taking many credible steps to do so), then the stock should appreciate significantly to perhaps $30 per share or more. Even if the company continues to have lackluster results, the downside should be minimal as the balance sheet is strong and the headline negativity of the industry is already well baked into the price.

Well-respected value investors, such as Donald Yacktman, have already seen the compelling story here and have taken the plunge on Apollo. It’s now time for you to consider doing so as well.

Disclosure: I am long APOL

The company is best known for the University of Phoenix, which in 2012 constituted 89% of revenues and 100% of operating profits. The remaining 11% of revenue comes from Apollo Global, which consists of a few small universities in Latin and South America and one in the UK.

With an EV to EBITDA valuation of only 1.6, it is safe to say that Apollo Group has a lot of negativity priced in and is now trading at a rock-bottom valuation. Despite criticism and headwinds in the for-profit education sector in general, the long-term prospects for higher education remain bright. This coupled with organizational reforms and a shifting strategy at Apollo make it increasingly likely that the company will bounce back strongly within the next few years.

Note: All Financial details referenced in this article can be found in the company's latest 10-K filing or most recent Q2 2013 conference call.

Company Overview

The University of Phoenix is probably the best-known for-profit education institution in America. The University was founded by Dr. John Sperling in 1973, after the educator was frustrated with the lack of study programs that suited working adult students who were often treated as second class citizens on many campuses. Nearly 40 years running, and the university is one of the largest educators in North America. However enrollments have dropped drastically in the past few years, from about 460,000 students in 2010 to only 357,000 in 2012 according to the most recent annual report. In the second quarter conference call at the end of March 2013, CEO Gregory Cappelli reported that enrollments were down to about 301,000 students, a 20% year-over-year drop. Financially speaking revenues have dropped about 15% in this period, and earnings, FCF/share and operating margins have all fallen as well. These metrics over the past three full fiscal years are summarized below:

| Metric | 2010 | 2011 | 2012 |

EPS | $3.62 | $4.04 | $3.45 |

| FCF/share | $5.73 | $5.18 | $3.56 |

| Operating Margin % | 20.5% | 20.3% | 15.9% |

Over the past 10 years the company grew FCF and EBITDA by more than 13% annually (even including the recent down years), and it has only been very recently that business has taken a turn for the worse. Hammering this home has been the rapid fall in share price from about $64/share in August 2010 to the current level of $17.41/share in May 2013.

Difficult Times in the For-Profit Education Sector

So what has caused this drastic change in fortunes for Apollo? Part of the trouble has been some harsh rhetoric and politicking out of Washington on the industry, as the federal government has taken a hard line against for-profits, claiming deceptive marketing practices and other aggressive tactics to attract students. Increasing enrollments was a number one priority at many of these institutions over the years, as this increased revenues (via federal loans) and thereby improving profits. As described more in the risk section below, students at for-profit institutions have traditionally relied heavily on federally funded financial aid packages. Due to high dropout rates and lower graduation figures than the non-profit education sector, the federal government has come down very hard on the industry recently. A lot of this negative publicity coupled with the rising costs of education has been the primary driver in a drastic decrease in enrollment starts.

Despite Challenges, Long-Term Prospects for Higher Education Remain Bright

Looking at the broader picture, however, and at the continuing challenges in America for higher education, recently the University of Phoenix released a very detailed report. In this report I believe the University has made a very good case that in order to continue to compete successfully in an ever increasing global environment, the U.S. really needs to get serious about more focused education and to provide specific training to ensure students have the right skills. The university's strategy which focuses more on part-time adult students to help retrain and improve their skills to be more relevant in the marketplace is a logical method to help close the current gap. The report goes in depth to explain how America is behind other major developed nations by more than 100 million years of education, which is leading to a loss of economic productivity. This gap sounds huge in real terms, but put in perspective it can virtually be made up entirely if all Americans were to simply spend an extra one year on higher education than they currently do.

Interestingly, if you read the Obama Administration's vision on higher education you will find striking similarities to the report referenced above from Apollo. The federal government also recognizes the skill gap, and President Obama has also set a goal that by 2020 every American should commit to at least one year of post-secondary training or higher education.

Although there is a lot of criticism on for-profit universities including the University of Phoenix, the bottom line is that everyone seems to recognize there is a growing problem in America and a gap between the skills that workers have and what the increasingly demanding global economy needs.

If you ignore for a moment all the noise coming out of Washington politicians on this industry, I think it becomes clear that in order to reach these goals to improve education overall, the for-profit section including University of Phoenix will be part of the picture. This is especially true because the government is advocating every American to commit to "at least one year" of post-secondary training. For many people this could be vocational-type training or associate's degrees which they might look to do online or in non-traditional manners. The University of Phoenix has one of the most extensive online education systems available, and is in the "sweet spot" so to speak in order to target and take on these types of students.

The Company Is Changing Its Strategy to Adapt to the New Realities

On the second quarter conference call results showed a continued rapid deterioration of student enrollment, and the company indicated that the start of the third quarter was also trending down at a similar rate of decline. For the full year 2013 operating profits excluding special charges are supposed to be about $525 million, or a margin of just over 14%. So this is a slowdown in margin decline from last year, but is still negative. To counter this, costs are being trimmed to the tune of $350 million in savings through 2014 and the organization is becoming leaner with fewer campuses. Although it takes some time to stop the bleeding, by significantly reducing its cost base Apollo is putting itself in a better position to turnaround.

In my opinion, the company management is listening to and learning lessons from the intense criticism the industry has received in the past few years. It's in the midst of restructuring and repositioning the University of Phoenix brand and does expect enrollment starts to return to positive territory in the near future, although whether that is late 2013 or 2014 is not clear. In the past few conference calls management has discussed strategic initiatives which are underway in order to improve the student experience and help students find jobs. This includes initiatives like their interactive career portal, which more than 25% students are already using and they are adding employers to this portal aggressively in order to better connect students with prospective jobs after graduation.

There are now 2,200 corporate partnerships and a strong focus on education to careers. The increased emphasis on industry partnerships seems to be gaining real traction: Back in October 2012 when I first researched Apollo, it reported 1,800 such partnerships, which means in only six months this has increased by more than 20%. The emphasis seems to be clearly shifting away from just spending resources on marketing to lure in students (and their financial aid money), and really focusing strongly on improving graduation and drop out rates.

In addition to this the company is focusing not only on degree granting programs, but also on vocational and certificate granting programs. This plays to the company’s core strengths in attracting working adults who want to acquire tangible skills for their jobs but don’t necessarily need a four-year degree. Eighty million adults in the U.S. don’t have a bachelor’s degree, and of those 50 million never tried to get one, so there is ample room for growth in this market.

In summary I see that the long term prospects of the higher education industry will remain positive, and the University of Phoenix is poised to be part of this. With more than 300,000 enrolled students, the University is a major force in education. The for profit industry as of 2010 had 2.4 million enrollments, which out of approximately 20 million higher education students in the US this is greater than 10%. So this industry is not just going to disappear, especially with the demand for more higher education continuing to grow.

Financial Strength

The company reported to have over $821 million in unrestricted cash in the most recent quarter vs. about $91m of debt. With a debt/equity ratio of less than 0.10 and an interest coverage ratio of over 50, the company is clearly in no near term risk of financial problems. This gives the company a lot of flexibility in being able to restructure itself quickly or also buyback more shares, which the company has done consistently over the past 10 years, as discussed below in more detail in the valuation section.

Management

The University of Phoenix was founded by now Exec. Chairman Dr. John G. Sperling (Ph.D), in 1973. An interesting note is that Dr. Sperling is still at it - at the young age of 91! A former professor at San Jose State, he founded The University of Phoenix with a goal in mind to better reach out to students who had a desire to work and study part time, a trend that was growing significantly at the time. Dr. Sperling currently holds the position of Chairman emeritus. His son Peter Sperling is the acting chairman of the board, having held various executive positions since 1983 at the company. The Sperlings together own about 2.5% of the company. Collectively insiders do hold about 13% of the company.

The CEO of Apollo, Gregory Cappelli, has been at the company since 2007 and has held the position of CEO since 2009. Initially he was co-CEO, but Charles Edelstein retired in mid-2012. Interestingly, the 44 year old was a managing director and research analyst at Credit Suisse and Abn Amro previously, so he should be well in tune with Wall Street and the investment business in general and bodes well for his credibility in terms of capital allocation decisions. Although Cappelli has taken the reigns at a very tough time in the industry, he has so far continued to make very rational and tough decisions and has stuck to them. This includes: $350 million in cost savings including the closing of many campuses, changes to marketing practices, having a new focused strategy on improving graduation rates and connecting students with prospective employers, and finally the smart decision to buy back significant amounts of stock at very cheap prices. In summary I think the management of the company is solid, and I don’t see any reasons to be majorly concerned on this front.

Valuation

With an EV/EBITDA of 1.6, Apollo is clearly cheap. The company still generates a lot of cash, has relatively low capital expenditures and has a very solid balance sheet. FCF/share is currently projected to be close to $3.40/share for FY13. Discounting this at a conservative 12%, with 0% projected growth over 10 years, and the fair value is $25.40/share, a margin of safety of more than 30%. This assumes 0% terminal growth as well. When you consider the more than $6/share in net cash on the balance sheet, there seems to be an upside potential of 50-75% to fair value from current prices.

Of course this assumes that the company can stop the bleeding and stop the decreases in enrollments. I think several factors make it exceedingly likely that long term at least 0% growth is achievable. For one, as discussed above. long term prospects in demand for higher education continue to be positive. Global spend is expected to grow 7% annually from 2012 to 2017. In addition, the company has a fresh $250 million share buyback program that is authorized, and the company should continue to retire shares and increase EPS by several percent per year this way. Outstanding shares have decreased from about 170 million to 122 million over the past five years, an annual decrease of almost 7%, as shown in the figure below. With an earnings yield at a ridiculous 46%, the company cannot really get any cheaper based on fundamentals.

Investment Risks

Shareholder control - Interesting to note is that the company has two classes of shares, Class A and B. The common stock, Class A shares which are available for purchase on the open market actually have no voting rights. The voting rights are exclusively held by Class B shares, which are all owned by the Executive Chairman Dr. Sperling and his son Peter Sperling (who is vice chairman of the board). If Dr. Sperling passes away, his voting rights pass to three trustees which are all current directors on the board (his son and two others). I don’t see this is a major negative for an investment in the company, but it surely is a negative in the sense that it keeps off the pressure from activist shareholders or other big investors who might positively influence the capital allocation strategies of Apollo going forward. That being said, so far CEO Cappelli seems to be doing a reasonable job here and I don’t see any cause for concern.

Access to Title IV funding remains a constant threat - One important aspect to understand about the University of Phoenix as well as other for-profit universities is that they receive most of their revenue from student financial aid, much of which comes from the U.S. government. Under the 90/10 Rule as part of the Higher Education Act, for-profit educational institutions must receive at least 10% of their funding from non-governmental sources, and can receive a maximum of 90% from Pell Grants and federal student loans. If an institution breaches this rule 1 year, it must comply the following year or it will lose access to all financial aid. Many of these institutions are very close to the 90% threshold currently.

In 2012 the University of Phoenix generated 84% of revenue from Title IV financial aid program funds, coming very close to the limit. The good news is that this has dropped from 86 and 88% in 2011 and 2010 respectively.

The community college push - The Obama Administration has publicly declared its preference for community colleges over the for-profit sector. Obviously, Apollo cannot compete on price alone here. The company must continue to stay relevant in order to stop losing market share, and it must prove that its programs are worth the money for many students because of the additional benefits that they offer compared to cheaper alternatives. This is a constant risk going forward and is a perception that the company must be on top of in order to keep its place in the higher education segment.

The Bottom Line

In conclusion, I think an investment in Apollo today is an incredible value for the money. The company is about as cheap as it gets in terms of earnings yield and is trading significantly below historical averages. Using any standard valuation techniques with conservative growth assumptions and it is easy to justify that the company is undervalued by at least 50% to 100%. With an additional $250 million authorized for share buybacks, and the company’s history of repurchasing large amounts of shares, look for continued inorganic growth in EPS of 5% or more in the coming year based on this alone. Although further declines in enrollments will probably offset this in the near term, if the company can show any signs of a turnaround in the decline rate ( which it is taking many credible steps to do so), then the stock should appreciate significantly to perhaps $30 per share or more. Even if the company continues to have lackluster results, the downside should be minimal as the balance sheet is strong and the headline negativity of the industry is already well baked into the price.

Well-respected value investors, such as Donald Yacktman, have already seen the compelling story here and have taken the plunge on Apollo. It’s now time for you to consider doing so as well.

Disclosure: I am long APOL