Following the herd is the surest way of achieving mediocre performance. To produce superior returns, we have two options.

First, be smarter or know more than the other guy. Howard Marks (Trades, Portfolio) refers to this as “second level thinking." For example, “Everyone thinks Apple has peaked and sales will begin to suffer. But I believe they are wrong and the company's brand loyalty and continued innovation will generate greater-than-expected sales and profits. Therefore, I'm going to buy the stock even though the talking heads on CNBC prefer Samsung.”

Some people possess the superior intellect and forward thinking necessary to invest in this manner. Sure, we may be right a few times and reap the rewards, but the ability to be consistently right in these contrarian approaches is a rare feat.

Our second option is to invest tactically – in areas where most dare not venture. One such arena is the field of stock spin-offs. Ask your neighbor, co-worker or even investment advisor what spin-offs look attractive to them. If he even knows what you're talking about, the odds that he follows this action are slim. And this is exactly why it is attractive. With fewer market participants, the chance for price inefficiencies rises significantly.

So let's talk about spin-offs.

What is a stock spinoff and how can I profit from it?

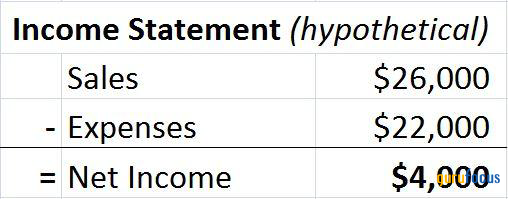

Let me give you an elementary example (forgive me if you're already familiar – I'll make it quick). Let's pretend that Apple was a very simple business that made only three products: iPhones, iPads and iPods. The company's income statement (again, hypothetical for simplicity's sake) looks like this:

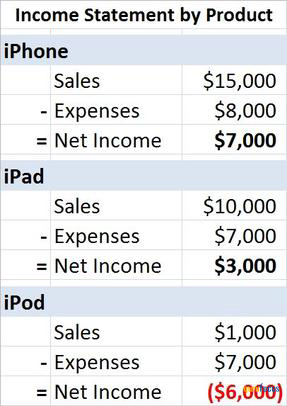

We then examine the three product lines and find the following financial results:

This data paints a pretty clear picture for investors. We want to own the iPhone unit and maybe iPad as well, but not iPod. In fact, the iPod division has been holding the company back. Net income came in at $4,000 but separated from the other products, the iPhone business is worth almost twice as much.

The owners of this fictitious Apple business are shareholders like us. They either own a substantial amount of the company's stock, are compensated based on stock performance, or both. So they share our desire to maximize shareholder value.

The simplest solution would be to stop producing iPods. But management is hesitant to do so. They believe the unit will turn around and they are investing in R&D to bring new innovative iPods to market. But this will take time. So what options do they have to unlock value now?

Most stocks, with a few exceptions, are priced according to an industry-standard multiple of earnings. If our fictitiously simple Apple is earning $4,000 and that represents, say, $30 a share, the stock price is likely in the neighborhood of $450 – a price equal to 15 times earnings. But the iPhone is earning $7,000, or $52.50 per share. On its own, just that portion of the business should be worth almost $800 per share. To unlock that value, management performs a spin-off. The iPhone becomes its own business, separate from the rest of Apple. A new company is formed, a new ticker symbol is assigned to the newly formed iPhone company, and shares are disbursed to existing Apple shareholders. Everyone who owned Apple stock now owns one additional share of iPhone for every share of Apple.

The Result

The original Apple stock will no doubt take a dive. Without the iPhone division its sales are cut in half and profits suffer as well. But the stock will still be worth something. For argument's sake, let's say that it fell from $450 all the way down to $100. Shareholders have still come out ahead since instead of owning Apple stock worth $450, they now own an $800 share of iPhone AND a $100 share of Apple for a combined value of $900. Even though the Apple stock price suffered, they doubled their money through the spin-off.

In general, this is the goal of spin-offs. They seek to unlock value from profitable divisions by separating them from the larger parent company. This was obviously an extreme example, but the illustration should serve its purpose.

Other Benefits of Spin-offs

The previous example showed how shareholders can profit from a spinoff, but what if you are not one of them? Can you still profit from these special situations? Absolutely. And here's how.

Most spin-offs are not as substantial as the Apple example. They generally involve smaller divisions of a company, and the new company represents only a small fraction of the parent. For this reason, spin-offs tend to be small cap stocks after the transition. Examples include Twenty-First Century Fox (FOXA, Financial) spinning off News Corp (NWSA, Financial), Valero Energy (VLO, Financial) spinning off CST Brands CST) and Sears Holdings Corp (SHLD, Financial) unloading Lands' End (LE, Financial) – more on this one in a minute.

Since most securities are held by institutions through mutual funds, ETFs and the like, they become the owners of these newly formed entities. But most large funds have charters which dictate the type of stocks they are able to hold. Some prohibit owning stocks that trade for less than five dollars. Others are restricted from owning stock in companies with market caps below $10 billion. Or in the Apple example, the stock might have been held for its exposure to the tablet market which the spinoff no longer possesses.

For these and countless other reasons, the unwilling owners of newly formed spin-offs often do not want to own them. So, naturally, they sell the shares on the open market and collect the cash.

This selling pressure often causes a short-term decline in the price of the security and creates an environment of inefficiency from which value investors can profit. Of the eight spin-offs that have occurred since the start of the year, only two are in positive territory.

Additionally, parent companies do not want to see spin-offs fail. It reflects poorly on management and disappoints shareholders who held onto the new shares. Therefore, they generally form them with healthy balance sheets. And when a “new” company begins day one with no debt and a steady flow of revenue it has a serious leg up on its competitors.

Why Spinoffs Outperform

According to a Penn State 25-year study, "stocks of spinoff companies outperformed their industry peers and the S&P 500 by about 10 percentage points per year." A Barron's article cited similar observations stating, "spin-offs historically have generated far better returns than the overall stock market, and they continue to shine."

Why does this phenomenon exist?

In addition to the benefits mentioned previously, most businesses are run better when they are out from under control of the parent. The subsidiary is often a small piece of the larger pie and its profits are frequently allocated to the R&D of other company products or divisions. However, once freed from the restraints of the parent, the spinoff gains the ability to devote profits to furthering its own objectives.

Spinoffs often outperform even the parent, especially if the spin-off company's management has set themselves up for a big payday. Executives are issued options, stock appreciation rights, restricted stock, or an ownership stake. These issues create an incentive for the spin-off's management to downplay the company's prospects prior to being separated from the parent company. Doing so will cause management's initial stock and/or options to be priced as low as possible in order to maximize their eventual gain. They are investors just like us. They want to buy low and sell high.

Avoiding the Dogs

Make no mistake; this group has its share of dogs just like any other group of securities. All spin-offs are not created equal. The inverse of our earlier Apple illustration might be the company wanting to spin off the iPod division just to get it off their books. If they are unable to unload it in an outright sale, clever executives might load it up with debt and dump it on the market for whatever pennies they can get for it. This would unlock the value of the parent in the same fashion but at a slower pace since the market would likely wait for future earnings reports to assess the results.

To avoid holding stock in such a disaster, here are a few things to look for in selecting quality spin-offs worth your investment dollar:

Management Moves – Which executives are taking positions with the new company? If the company is looking to dump toxic assets, no one at the firm will want much to do with it. However, if the CEO, CFO or other high-ranking executives leave the parent to take new positions in the spin-off, this is usually a good sign.

Insider Buying – We have to dig through company reports and SEC filings to uncover the details of these ventures. Company insiders, on the other hand, have intimate knowledge of the new structure. After all, they created it. This is a basic “follow the money” tactic. If insiders are buying up shares of the new firm, or better yet, selling their stock in the parent company to do so, it's time to get interested.

Stock-Based Compensation – Executive compensation packages can be complex, but try to focus on those where the CEO is rewarded primarily through stock. If an executive leaves the company to take a position at the new spin-off even though the salary is lower, he could be eying a windfall from stock appreciation.

Debt Level – We touched on this earlier, but it is worth mentioning again. Quality spin-offs , i.e. those with the greatest potential for success, start with a clean balance sheet. If a new company is forced to borrow large sums before separating from the parent, the ensuing interest payments will greatly inhibit their ability to generate profits.

In addition to the hard metrics above, ask yourself these questions:

1. Will the spin-off allow a great business to be separated from an average one and be better appreciated?

2. Or, does the spin-off allow the parent to rid itself of a business it cannot sell and/or off load debt?

3. Is the valuation multiple of the company low in relation to competitors which the spin-off will fix?

4. What are the insiders' motives for the spin-off?

Timing Your Entry

Most investors with proven track records in this field suggest waiting one to three months before taking a position. In a 2012 article on the subject, Bespoke Investment Group commented, “By waiting, investors will not be subject to the initial selling that inevitably takes place as existing shareholders sell shares of the child stocks that may not fit in with their investment criteria or guidelines.”

Joel Greenblatt (Trades, Portfolio) is an absolute legend in this area. To learn more about his process, I would suggest reading his book, "You Can Be a Stock Market Genius" (cheesy title, but a great read).

There is no precise formula on the execution side, but the one to three month wait window should help to avoid being caught in the stampede of sellers.

Where to Find Them

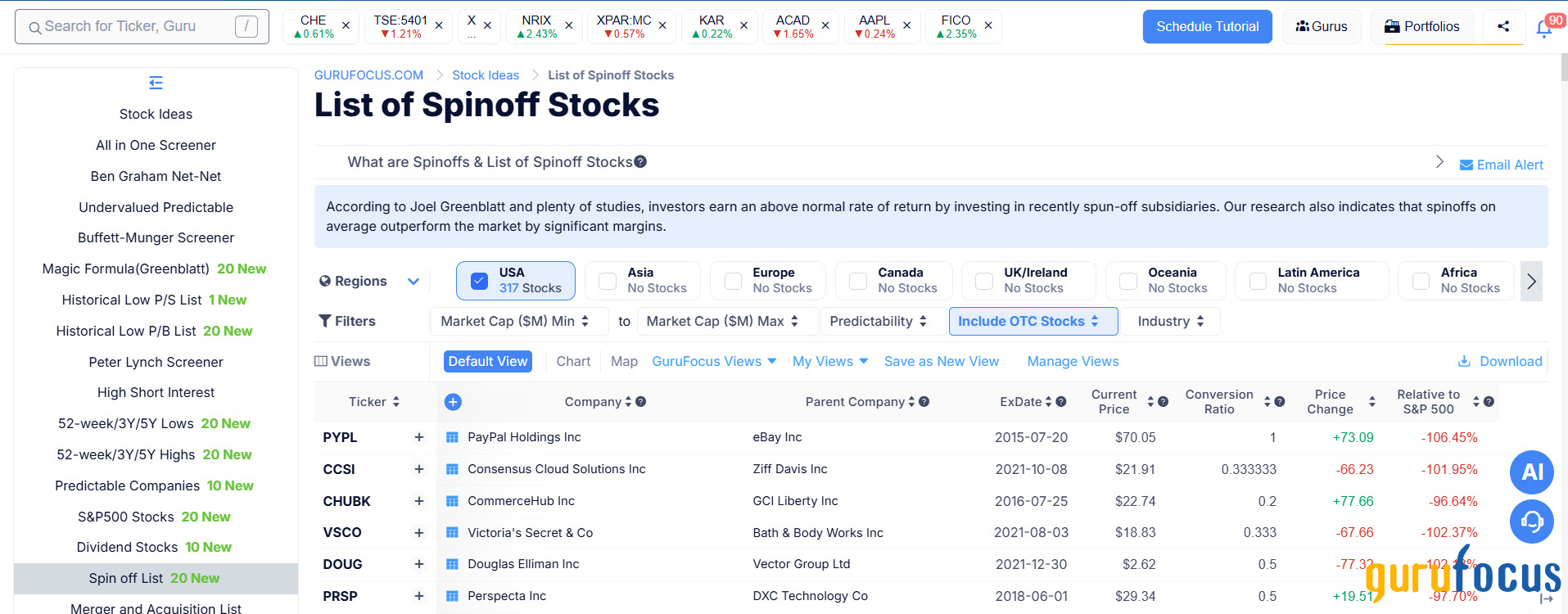

GuruFocus.com recently launched a new feature called the Spinoff List. It can be accessed here: https://www.gurufocus.com/screener/spinoff or found at the bottom of the dropdown list by hovering over the 'Screeners' heading at the top of the page.

This takes the work out of hunting these opportunities down and presents an abridged list of all publicly traded spin-offs in order by date. The list comes direct from the Morningstar feed so the data is top notch.

You'll probably notice that the list is not terribly long. Since the start of 2013, there are only 32 names – eight in the last quarter. This is fine since it takes a good bit of work to thoroughly research an idea.

After reviewing GuruFocus' Spinoff List, I came across a situation I had researched several months ago – the Lands' End spin-off from Sears which now trades under ticker symbol LE.

Facing declining sales, shrinking margins and lower same store sales, Sears (SHLD, Financial) stock has been in a death spiral since 2007. Sixty percent of outstanding shares are now held short and the stock is showing no signs of life. The company recently reported an annual loss of $12.87 per share. Even for a $42 stock, that's a serious club to the kneecap. The one beacon of light for the flailing company has been Lands' End.

Is Lands' End Healthy?

Bought by Sears for $1.9 billion in 2002, the newly spun unit now trades at a market cap of $841 million. Lands' End (LE, Financial) has been light on revenue growth the last few years but profits have been rising. Cost-cutting measures by management reduced SG&A expenditures by 6.4% last year and 3.6% in 2012.

Earnings for 2014 came in at $2.47, making today's $26.44 share price equivalent to 10.8 times earnings. This is a more than fair multiple for an established brand like Lands' End. Unlike many of today's suffering brick and mortar retailers, 83% of LE revenues come from online and catalog sales. The rest come from Sears boutiques and 16 stand-alone stores.

So far, the numbers look healthy. On the technical side, institutional sales pressure is also on our side. Sears is a roughly $5 billion company. Tiny by comparison, $840 million small cap Lands' End is likely to be an unsuitable investment for many of the funds that were issued shares. LE began trading on April 7, so we are now entering the beginning of the spin-off buy window.

They Couldn't Make It Easy

Before the spin-off was completed, Sears executives took advantage of the situation and stole a life line before cutting Lands' End loose. The company paid a $500 million dividend to Sears just before gaining its independence. Financed with a credit line, this will equate to roughly $22 million in annual interest payments by LE.

If chopped from last year's bottom line, this would give Lands' End earnings per share of roughly $1.75 instead of the reported $2.47. Tack on a few additional expenses for headquarters operation and various transitional costs, and earnings are cut in half or more.

Unfortunately, this isn't the first time Sears has acted in such a fashion. CEO Edward Lampert (Trades, Portfolio) spun off Orchard Supply Hardware from the firm in late 2011. Orchard was in bankruptcy court inside of 18 months. The culprit? Sears released Orchard into the world with $340 million in debt from the Sears balance sheet.

Hopefully, the newfound freedom will spark growth for the clothier. Profits have suffered under Sears' ownership, but a new management team with a fresh perspective could once again foster an atmosphere of expansion.

To Buy or Not to Buy?

For valuation's sake, I have to base my numbers off the present. And given the rough downward estimates I've made to 2014 net, I would need a deeper haircut before risking capital. Shares hit the market at $33.50 and closed today at $26.55. If shares experience an additional 25% to 50% decline the stock could get attractive.

Sears reported $79 million in net income for Lands' End over the prior twelve months. The $22 million interest payment, in relation, is quite significant as it will eat more than a quarter of bottom line profits.

If Sears were not facing a cash crisis, they might have formed the Lands' End issue with no debt. This would make today's price more than attractive and remove the additional risk imposed on the security. But because of the $500 million note, we must be disciplined in the price we pay to ensure an adequate yield.

The retail sector is a battlefield. Companies need every advantage they can get in order to survive. Unfortunately, Sears handicapped Lands' End right out of the gate with a selfish move that may very well cripple its chances of survival.

Summary

Spin-offs require a healthy amount of research. Unlike companies with long histories of reported financials, initial decisions must often be based on limited data. Be prepared to read through the parent company's 10-K to unravel the details of the deal. In Lands' End's case, the $500 million in long-term debt was not listed on the initial balance sheet since it had not yet been paid/borrowed.

The rewards, however, can be spectacular. You won't find a dozen opportunties a quarter, but one or two no-brainer deals can go a long way in your portfolio.

Not yet a GuruFocus Premium member? Take a Risk-Free 7-Day Trial and experience the best investment research tools available. If you decide it's not for you, cancel and owe nothing.