The price-to-cashflow ratio (PCF) is a popular metric among value investors. Many believe that using cashflow, rather than accounting earnings, delivers a truer picture of a company’s business performance, which in turn leads to better investment performance.

Set out below are the results of two Fama and French backtests of the cashflow yield (the inverse of the PCF ratio) data from 1951 to 2013. As at December 2013, there were 2,526 firms in the sample. The value decile contained the 269 stocks with the highest earnings yield, and the glamour decile contained the 311 stocks with the lowest earnings yield. The average size of the glamour stocks is $4.74 billion and the value stocks $4.80 billion. (Note that the average is heavily skewed up by the biggest companies. For context, the 2,526th company has a market capitalization today of $272 million, which is much smaller than the average, but still investable for most investors). Stocks with negative cashflow were excluded. Portfolios are formed on June 30 and rebalanced annually.

Annual and Compound Returns (Portfolio Constituents Weighted by Market Capitalization)

In this backtest, the two portfolios are weighted by market capitalization, which means that bigger firms contribute more to the performance of the portfolio, and smaller firms contribute less. Here we can see that the value decile has comprehensively outperformed the glamour decile, returning 16.7 percent compound (18.6 percent in the average year) over the full period versus 9.3 percent for the glamour decile (11.5 percent in the average year).

These returns are practically identical to the returns found for the price-to-earnings ratio in last week’s post (Investing Using the Price-to-Earnings Ratio and Earnings Yield (Backtests 1951 to 2013)).

Cashflow Yield (Market Capitalization Weight)

The reason for value’s outperformance is simply due to the fact that the value portfolios generated more cashflow per dollar invested; 27.2 percent versus 4.3 percent for the glamour portfolio. (I used a rolling average this week. The “average” I’ve quoted is for the full period. The rolling average has been higher, but it’s rarely been lower.):

Recent Performance (Market Capitalization Weight)

As we saw last week, value’s outperformance over glamour is not a historical artifact. If we examine just the period since 1999, we find that, though the return is lower than the long term average, value has continued to be the better bet.

Value has continued to outperform glamour since 1999, beating it by 8.7 percent compound, and 6.2 percent in the average year. The reason for lower returns recently may be due to the popularization of simple value strategies, but I think it’s more because the market is still working off the massive overvaluation of the late 1990s Dot Com boom.

As I noted last week, market capitalization-weighted returns are useful for demonstrating that the outperformance of value over glamour is not due to the value portfolios containing smaller stocks. Unless you’re running an index (or hugging an index), they’re not really meaningful. The easiest portfolio weighting scheme is to simply equally weight each position. (If we’re prepared to put up with a little extra volatility for a little extra return, we can also Kelly weight our best ideas). Here are the equal weight return statistics for the cashflow yield.

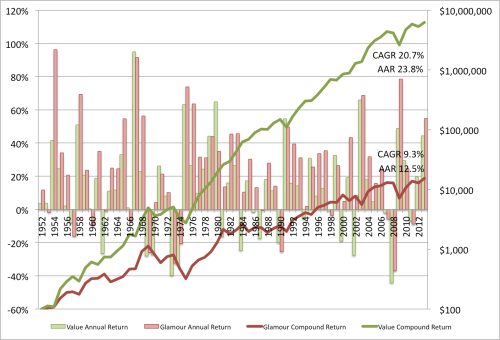

Annual and Compound Returns (Portfolio Constituents Equally Weighted)

In the equal weight backtest value generated 20.7 percent compound (23.8 percent on average), beating out glamour’s 9.3 percent compound return (12.5 percent on average). Folks who saw last week’s post might note the small advantage for the cashflow yield’s value decile over the earnings yield’s value decile, 20.7 percent versus 20.1 percent. We’ll examine the significance of this small win by cashflow in the coming weeks.

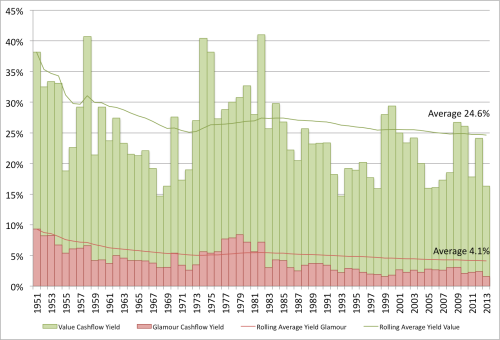

Cashflow Yield (Equal Weight)

Again, the value portfolios generate more cashflow than the glamour portfolios, generating 24.6 percent on average versus 4.1 percent in the glamour portfolios. As we saw last week, the average cashflow yield for the equally weighed value portfolio is slightly lower than the average cashflow yield for the market capitalization-weighted portfolios, which indicates that, over the full period, bigger stocks tended to be a cheaper method for buying cashflow than smaller stocks. That won’t always be the case, but it’s interesting nonetheless.

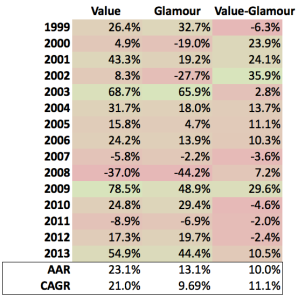

Recent Performance (Equal Weight)

In the equal weight portfolios, value has really outperformed glamour since 1999, beating it by 11.1 percent compound, and 10.0 percent in the average year.

As we saw last week, over the long run, cheap stocks tend to outperform more expensive stocks. Like the PE ratio, the PCF ratio is a very useful metric for sorting cheap stocks from expensive stocks.