Upon Mohnish Pabrai (Trades, Portfolio) interview, he concluded what he learned from Warren Buffett below:

he's a better investor because he's a businessman and he's a better businessman because he is an investor.

When investors buy shares of companies, they should treat themselves as owning part of the companies. Once we think in terms of running a business, we will start to pay attention to return of capital and other financial metrics necessary for running a business. In fact, CFI is a business still chaired by its founder and run by owner mindset. If we look into all the financial achievements of CFI, we will find that CFI has a lot of characters a long-term investor will admire for and would like to run the business as such. In this article, I will reveal what attracts me to CFI and why I believe that CFI deserves to be part of our portfolio.

Business overview

CFI manufactures, sources, markets and sells mattress fabrics and upholstery fabrics to the furniture and bedding industries in North America and internationally. CFI divides its businesses into two segments: Mattress Fabrics and Upholstery Fabrics. Its key customers include Serta, Simmons, Tempur Sealy, Select Comfort, Carpenter, Corsicana Bedding, Pacific Coast Feather, Southerland, etc.

As shown below, CFI has increased its share of U.S. bedding shipments from 87.2% in 2012 to 90.6% in 2013.

(click to enlarge)

Source: Company Presentation

For the macro business trend in the mattress industry, there is favorable demand. First, since mattresses are the most profitable products for home furnishing retailers, the industry has promoted benefits of sleep for overall health for a long period of time already. As a result, consumers changing mattresses has become more frequent, and there is growing consumer demand for better bedding. As more mattress are sold, the demand for the fabrics made by CFI will increase.

In addition, since fabrics business is just-in-time driven and without warning, there is limited competition from imports. Another reason for low overseas competition is that the freight and duty costs make imported fabric not as competitive as locally produced fabrics. This in fact helps to create competitive barriers in favor of CFI.

CFI is run by owner mindset. When we compare the business between 2000 and 2014, we can see that CFI has restructured itself from 3,500 U.S. employees in 2000 to 107 U.S. employees and 435 Chinese employees in 2014. It consolidated 14 U.S. upholstery fabrics plants in 2000 to only 1 U.S. plant and 4 China plants today. Furthermore, CFI reduced its fixed assets need from $92 million in 2000 to $0.8 million in U.S. fixed assets and $5 million in China fixed assets in 2014. All are great achievements, which CFI shareholders should appreciate.

NOL carryforwards

CFI has $45.7 million in U.S. federal and state loss carryforwards at the end of fiscal 2014. CFI does not pay cash taxes in the United States nor does it expect to for a number of years. As of Q4 2014, CFI paid estimated income cash tax rate of 17.6% for CFI's non-U.S. entities divided by consolidated income before income taxes. The NOL carryforwards can help to enhance the earnings, so does return for prospective CFI investors.

Acquisitions

CFI has made two successful mattress fabrics acquisitions since fiscal 2007. CFI is patient and disciplined with any capital commitment. In its company presentation, CFI clearly states that it will ensure any acquisitions will not jeopardize the financial health of CFI.

Valuations

CFI has already returned in excess of $160 million to its shareholders over the last 13 years. Relative to $188 million enterprise value, the return of capital back to shareholders is significant. This shows the culture emphasizing stewardship of capital utilization and strong capability of generating free cash flow. As shown below, CFI has around 25% return of capital for the past five years.

Source: Company Presentation

(click to enlarge)

Source: Company Presentation

Based on $188 million enterprise value and $13.8 million FCF in 2014, CFI also generates an attractive 7.3% FCF yield.

(click to enlarge)

Source: Gurufocus.com

According to Peter Lynch chart from Gurufocus.com, CFI can trade up to $21, implying 20% upside potential.

Despite the fact that the upside potential does not look extremely lucrative, the stability of CFI and its superior return of capital make CFI a good investment. For any investment, we always strive to assess the risk/reward profile. With the history already illustrated so much about the financial stewardship of CFI, I view the risk in CFI as low. The 20% upside reward relative to its low risk profile make CFI much more appealing to prospective investors.

Share repurchase program

In fiscal 2012 and 2013, CFI repurchased 1.1 million shares, representing 8.5% of outstanding shares. Following the end of fiscal 2014, CFI purchased additional 22,101 shares for approximately $380,000, which is within the $5 million repurchase plan authorized by Board of Directors as of February 25, 2014. All the share repurchase program shows that the management team and the board of CFI is eager to return capital back to its shareholders when it is appropriate.

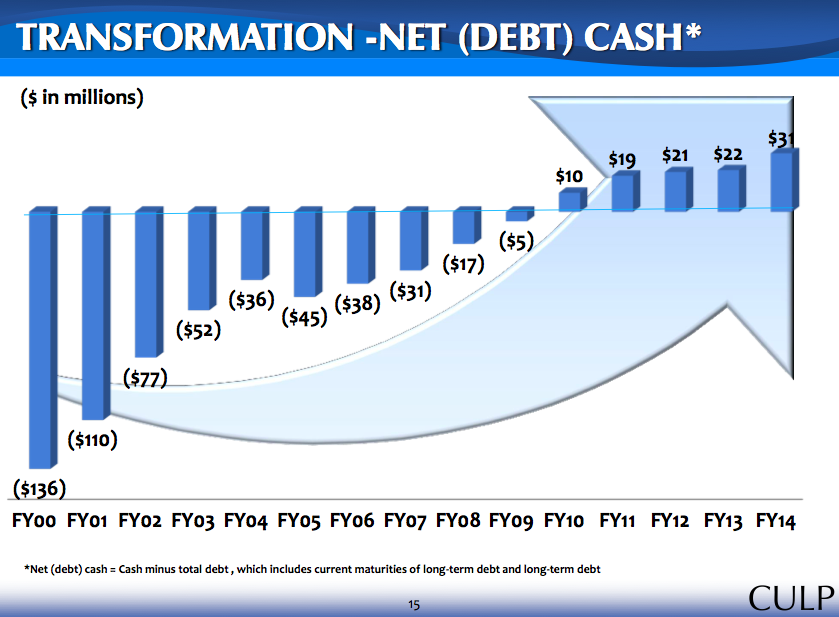

The continuous decline in debts

(click to enlarge)

Source: Company Presentation

Not only did CFI repurchase its own shares, but also reduced its debts from $136 million in 2000 to today's net cash of $31 million. This is attributed to the stewardship of focusing on return of capital and not to overspend on any acquisitions. For the enterprise value of $188 million, the transformation on debts is outstanding for CFI and further shows the financial strengths of CFI.

Management team

(click to enlarge) (click to enlarge)

(click to enlarge)

Source: Proxy Statement

For the latest proxy statement indicating the number of outstanding shares as of April 27, 2014 as shown above, the Culp family, including Robert Culp, Judith Walker and Harry Culp, together owns 12.9% of CFI's outstanding shares. The substantial holdings illustrate the confidence of the Culp family in CFI. In addition, CFI is chaired by the founder, Robert G. Culp. With debt reductions and capital returns to shareholders through shares buyback and dividends, we can see that CFI is truely run by owner mindset with interest aligned with minority shareholders.

Franklin N. Saxon has been the CEO of CFI since May 1, 2007. In fact, Mr. Saxon has been with CFI since 1983. He served as CFO and COO in CFI. His long tenure and experiences in various important roles make him understand the Fabrics business well. Plus, his previous role as CFO helps him to incorporate important financial metrics, such as return of capital, into his corporation vision and the expansion of the business.

Risks

First, most U.S. consumers are still under tight financial budgets. If there is any further economical slowdown, the demand for bedding and upholstered furniture sales will decline accordingly. However, the housing market seems to see sign of recovery. This should help to give some support for the sales of CFI. Second, since CFI is based on Just-In-Time business model, any delay in shipment can cause customer dissatisfaction and lead to less sales in the future. Third, there is risk that management will do dilutive acquisitions. However, based on past track record, management team of CFI is very cognizant of the acquisition risks. Their interests are well aligned with minority shareholders since the Culp family owns substantial shares of CFI.

The bottom line

Above 20% return on Capital for the past five years helps to demonstrate that CFI has superior capital allocation capability. In addition, CFI has been able to pay off all its debts while building up net cash position of $35 million and repurchasing its own shares. I believe that the owner mindset assists CFI in making those outstanding achievements, and the current management team has been in place for a long time, which I envision will continue to deliever great shareholders return in the foreseeable future. For long-term investors, CFI is a good candidate to include in your portfolio.

Disclosure: I am not a securities broker/dealer or an investment adviser. You are responsible for your own investment decisions. All information contained should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.

Also check out: