In today's brutal retail environment, most retailers would suffer due to lower sales and margins. However, for those strong retailers with great brands, I believe that they deserve to be given more thorough analysis and see whether their depressed earnings and sales are temporary or permanent. For Guess (NYSE:GES), I am strongly impressed by its consistent global product licensing earnings and its history of capital return back to its shareholders. Plus, a quarter of GES's market capitalization consists of cash, which shows the solid financial strength of GES. Although nobody can predict what the future fashion trend will be, GES has the financial flexibility to wait and catch the next great fashion. With 41% margin of safety calculated by gurufocus.com, I encourage my fellow readers to look further into GES to appreciate its values, and I will provide my FCF valuation for GES with 37% upside potential.

Business Overview

For the history of GES, it was established by the Marciano brothers, Paul Marciano and Maurice Marciano. One of their initial designs was a stonewashed, slim-fitting jean, the 3-zip Marilyn. Bloomingdale's was GES's first department store customer, and the jeans got sold off in just hours. This led to the beginning of the success story of GES.

Guess is a lifestyle brand selling eyewear, handbag, fragrance, jewelry, watches, footwear, and clothings. It targets the millennial, which is the highest growth segment in the apparel industry.

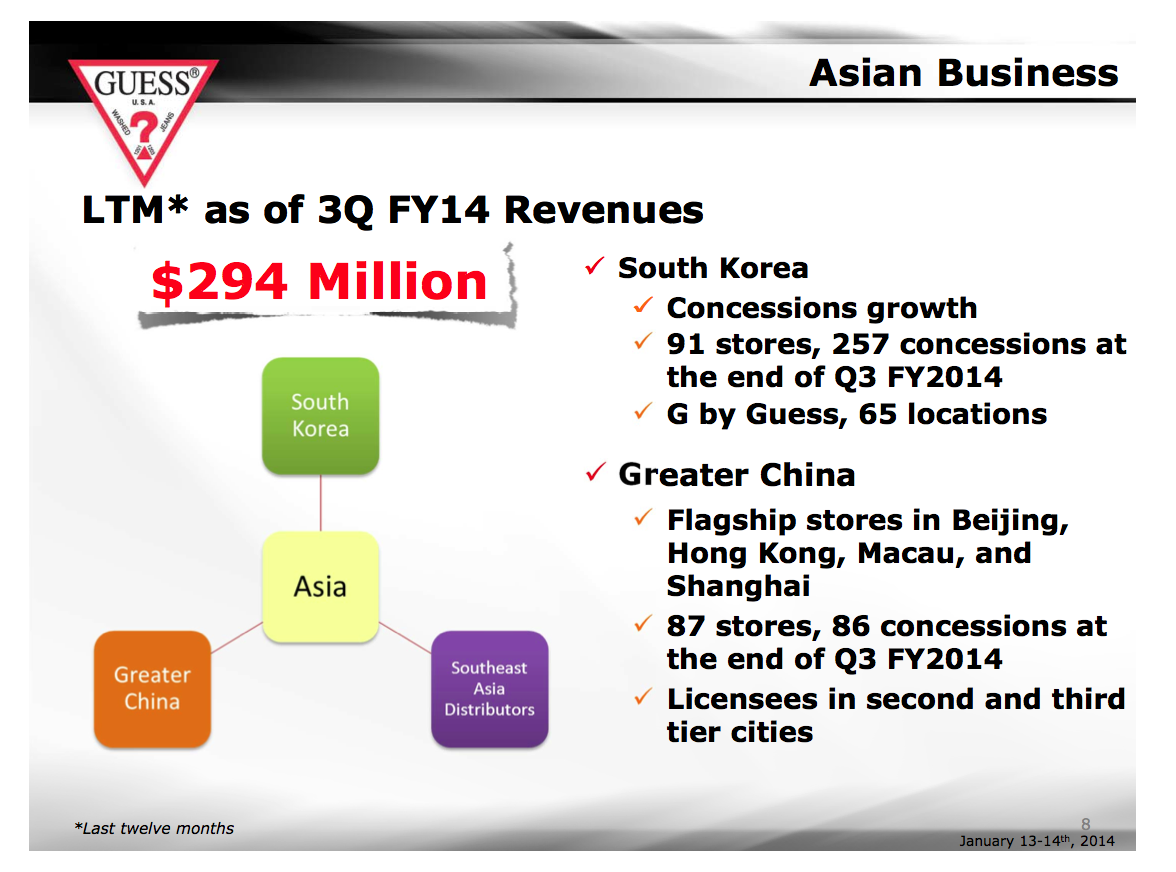

While generating 42% sales from North America and 35% from Europe, GES has the ambition to expand oversea as shown below:

(click to enlarge)

Source: Company Presentation

With sales growth in Asia, GES definitely has the future growth engine while the brand in Asia is well-known. From store counts perspective, GES has 480 stores in Asia, 635 stores in Europe and Middle East, and 588 stores in Americas according to the company presentation data in January 2014.

Why did GES decline to today's depressed level?

The following is the latest 2015 guidance:

Outlook

The Company's expectations for the third quarter of fiscal 2015 ending November 1, 2014, are as follows:

- Consolidated net revenues are expected to range from $590 million to $600 million.

- Operating margin is expected to be between 3.5% and 4.5%.

- Diluted earnings per share are expected to be in the range of $0.15 to $0.20.

The Company updated its outlook for the fiscal year ending January 31, 2015, which is now as follows:

- Consolidated net revenues are expected to range from $2.44 billion to $2.48 billion.

- Operating margin is expected to be between 5.5% and 6.0%.

- Diluted earnings per share are expected to be in the range of $1.05 to $1.20.

As the expected EPS of Guess in the range of $1.05 to $1.2 compared against street consensus expectation of $1.5 EPS, it is not difficult to see why GES declined significantly to its 52 weeks low. With the disappointed financial performance, the management team of GES realized the urgency to initiate the new $20 million cost saving program to streamline its North American retail division. In addition, GES has already identified 50 stores to close before the end of fiscal 2016. On top of these 50 stores, 50 percent of its North American stores will be up for lease renewal in the next three and a half years. The optionality of closing down unprofitable stores with lease expiration should be cost efficient and eventually help to restore the profit margins of GES. This seems to drive the stock price to rebound from its trough in the near future.

Shares Repurchase and Dividend Payments

Since 2009, GES has returned $950 million in the forms of shares buyback and dividends. Relative to today's market cap of $2 billion and $1.5 billion enterprise value, the return of capital is significant. This shows that the management team of GES has a shareholder friendly policy for returning back capital to shareholders instead of spending the money recklessly on acquisitions.

In terms of financial strength, GES has $466 million in cash relative to its $2 billion market cap. The cash position should give financial flexibility to GES.

Valuation

Source: GuruFocus.com

Based on the DCF valuation from Gurufocus.com, GES has 41% margin of safety and should be valued at $39.42.

(click to enlarge)

Source: Company Presentation

It is no wonder that Gurufocus.com gives 41% margin of safety to GES. Based on the 8.9% FCF relative to net revenue, GES can generate amply of free cash flow. That's why GES is capable of returning back almost $1 billion to its shareholders since 2009. One important point I would like to stress about GES is the global product licensing division. The division has $120 million sales for the last twelve months as of Q3 2014. With 89.6% operating margins, the operating earning is $107 million for the last twelve months as of Q3 2014. Let's step back and think about the global product licensing division. It is a great free cash flow generator as GES does not need to come up with any working capitals or investments to generate the $107 million licensing earnings. As a result, GES historically generated significant amount of free cash flow and return the capital back to shareholders.

| Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Stabilized Yr. |

| Year | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 |

| Sales | 2,594 | 2,646 | 2,726 | 2,807 | 2,920 | 3,036 | 3,127 | 3,221 | 3,318 | 3,417 | 3,520 |

| EBITDA | 311 | 318 | 327 | 337 | 350 | 364 | 375 | 387 | 398 | 410 | 422 |

| EBIT | 226 | 230 | 237 | 244 | 254 | 264 | 272 | 280 | 289 | 297 | 306 |

| Net Income | 153 | 156 | 161 | 166 | 172 | 179 | 184 | 190 | 196 | 201 | 208 |

| Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â |

| EBIT x (1 - Tax Rate) | 151 | 154 | 159 | 164 | 170 | 177 | 182 | 188 | 193 | 199 | 205 |

| - Capital Expenditure | 78 | 79 | 82 | 84 | 88 | 91 | 94 | 97 | 100 | 103 | 106 |

| + Depreciation & Amortization | 86 | 87 | 90 | 93 | 96 | 100 | 103 | 106 | 109 | 113 | 116 |

| - Change in Non-cash Working Capital | 18 | 11 | 16 | 17 | 23 | 24 | 19 | 19 | 20 | 20 | 21 |

| Adjusted Free Cash Flow | 141 | 152 | 151 | 155 | 156 | 162 | 173 | 178 | 184 | 189 | 195 |

| FREE CASH FLOW (FCFF) VALUATION MODEL | Â |

| Present Value of Free Cash Flow (NYSE:FCF) | 1,038 |

| Present Value of Terminal Value | 1,427 |

| Value of Operating Assets | 2,464 |

| Value of Cash, Marketable Securities & Non-operating assets | 478 |

| Value of the Firm | 2,942 |

| Value of Debt | 162 |

| Value of Common Equity | 2,780 |

| Value of Common Equity Per Share | 33 |

Other than utilizing others' financial models, I inputted Google's financial data into my DCF model, and I come up with my target price of $33, implying 37% upside potential for GES. Although my DCF model showed 37% upside potential rather than the 41% margin of safety derived from Gurufocus.com, I believe that the lower valuation is mainly due to my pessimistic assumptions to reflect the current sub-par financial performance of GES. If GES can start to show positive momentum in its sales and margins in the near future, I might revise my assumptions to reflect such positive outlooks.

Stable and Attractive Dividend Yield

(click to enlarge)

GES has an attractive dividend yield. After the recent share price decline, the dividend yield reached an all-time high of 3.8%. For investors looking for dividend yield, GES can be a good candidate in your portfolio.

Management Team

(click to enlarge)

Source: Proxy Statement

Both the founders, Maurice Marciano (13.8%) and Paul Marciano (14.1%), held significant stakes in GES. Paul Marciano has been the CEO of GES since January 8, 2007. He served several important roles in GES, including Creative Director and Chief Operating Officer. He even survived the worst recession in 2009. With his 14.1% ownership in GES, GES is run by owner mindset. This owner mindset should be one of the main reaons behind why GES has returned around $1 billion back to its shareholders since 2009.

As there is need for changes, GES recently appointed Sandeep Reddy as CFO in July 2013. He has led the GES Europe Finance Team as CFO since September 2010, demonstrating his leadership, financial and business acumen. Previously, he held senior financial roles in Mattel for 13 years in Europe and the United States. With his experience in both the major markets GES serves, Sandeep Reddy is expected to bring positive changes so as to help GES navigate the current brutal retail environment without demaging the financial health of GES.

Risks

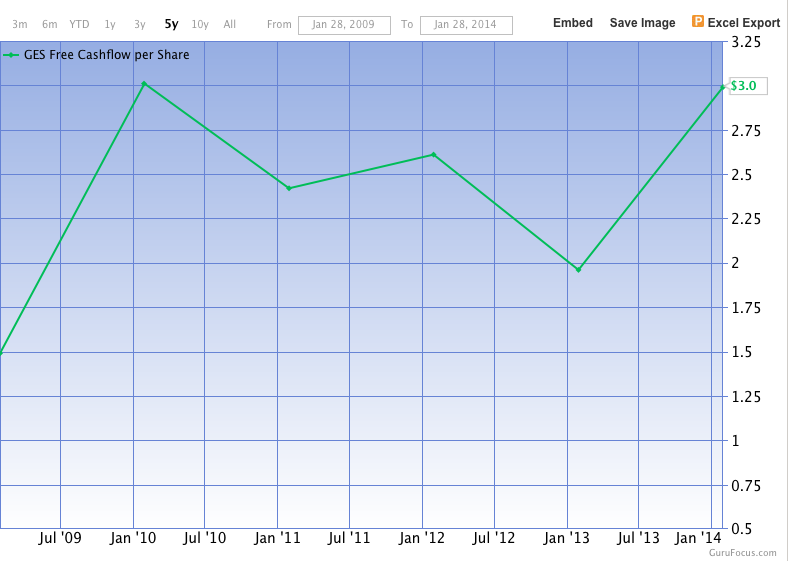

First, GES has experienced negative same store sales since 2011. the negative comp can decelerate further, and the sluggish North America retail and whole division can come in worse than anticipated due to a slowdown in the consumer recovery. However, GES is capable of generating healthy free cash flow around $2.5 per share as shown below.

(click to enlarge)

Source: Gurufocus.com

With GES trading at $23.44, the implied P/FCF is about 10x, which is very attractive for value-oriented investors. Together with around 25% of market cap being in cash, GES has the financial flexibility to implement turnaround plan if needed and restore the health of the company. Second, the retail industry is very volatile. The fashion trend can dramatically affect probabilities of any retailers, including GES. By investing in GES, prospective investors take on the retail business risk. In addition, I would like to reveal that retailers, including GES, rely significantly on brand equity. As we witnessed in Coach (NYSE:COH), sometimes even the best brand can slowly lose attractiveness to its customers; then investors would susquently incur capital loss in their stocks. Prospective investors should independently assess whether GES has enduring power and decide whether they would like to take on the risk investing in GES.

The Bottom Line

In my opinion, GES is still a relevant global brand with significant brand equity. This can be reflected by the healthy free cash flow generated by the global product licensing division. Despite all the sale and margin headwinds GES face today, I believe that GES has more than sufficient financial flexibility to turnaround the business. For a company with 41% margin of safety, long-term investors should have enough cushion to weather any adverse retail environment and realize a sizable return for their loyalty in GES.

Disclosure: I am not a securities broker/dealer or an investment adviser. You are responsible for your own investment decisions. All information contained should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.