Long-established in the Consumer Packaged Goods industry, The Campbell's Co (CPB, Financial) has enjoyed a stellar reputation. However, it has recently witnessed a daily loss of 0.52%, juxtaposed with a three-month change of -2.44%. Fresh insights from the GF Score hint at potential headwinds. Notably, its diminished rankings in financial strength, growth, and valuation suggest that the company might not live up to its historical performance. Join us as we dive deep into these pivotal metrics to unravel the evolving narrative of The Campbell's Co.

Understanding the GF Score

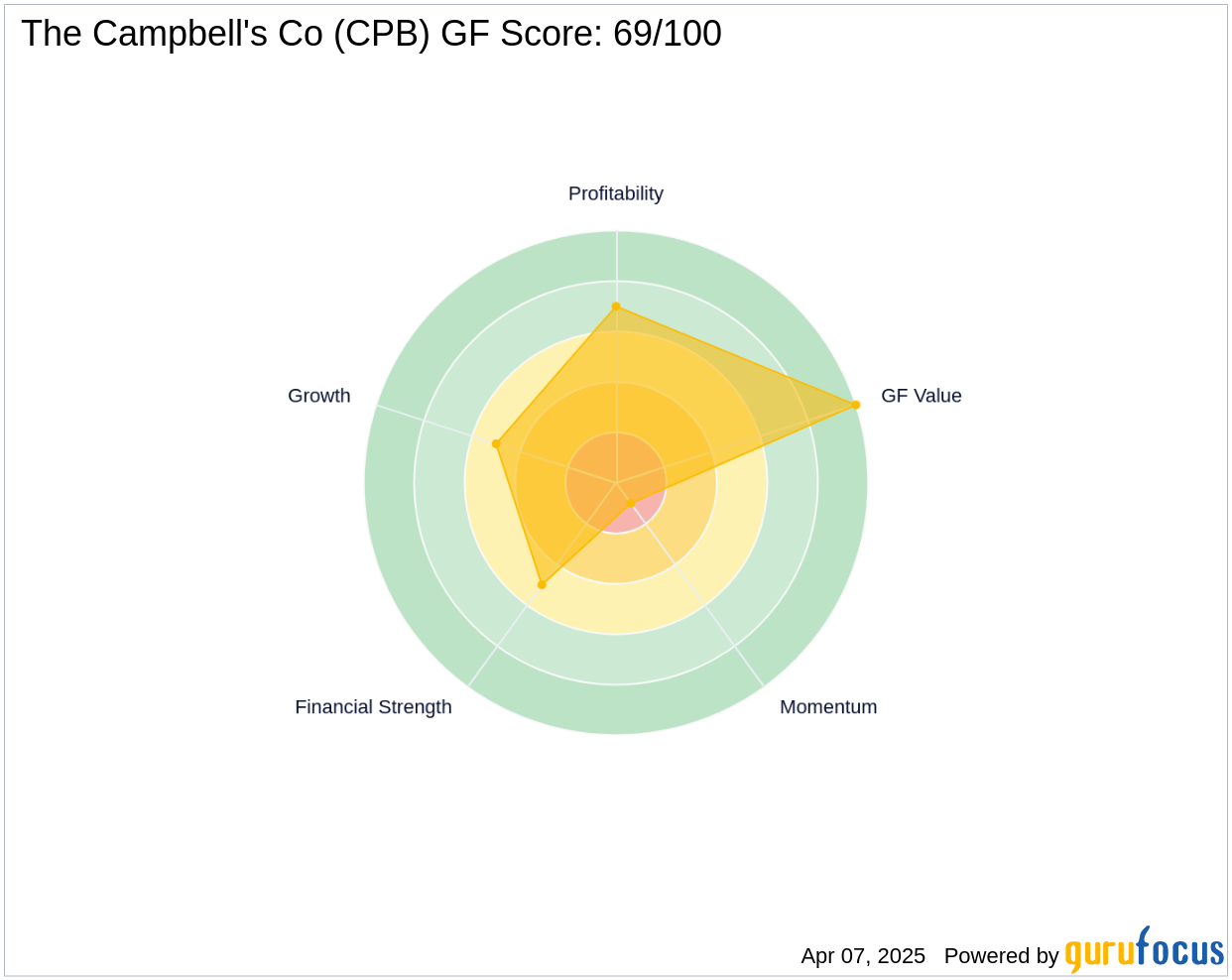

The GF Score is a stock performance ranking system developed by GuruFocus using five aspects of valuation, which has been found to be closely correlated to the long-term performances of stocks by backtesting from 2006 to 2021. The stocks with a higher GF Score generally generate higher returns than those with a lower GF Score. Therefore, when picking stocks, investors should invest in companies with high GF Scores. The GF Score ranges from 0 to 100, with 100 as the highest rank.

- Financial strength rank: 5/10

- Profitability rank: 7/10

- Growth rank: 5/10

- GF Value rank: 10/10

- Momentum rank: 1/10

Based on the above method, GuruFocus assigned The Campbell's Co the GF Score of 69 out of 100, which signals poor future outperformance potential.

Company Overview

Over the past 150-plus years, The Campbell's Co has evolved into a leading packaged food manufacturer in North America, with a portfolio that extends beyond its iconic red-and-white labeled canned soup. In fiscal 2024, snacks accounted for nearly half of its revenue, followed by soup (28%), other simple meals (17%), and beverages (7%). Outside its namesake, its brands include Pepperidge Farm, Goldfish, Snyder's of Hanover, Swanson, Pacific Foods, Prego, Pace, V8, and recently acquired Rao's (a deal that closed in March 2024). Around 90% of its revenue results from the US and the remainder from Canada and Latin America.

Financial Strength Breakdown

The Campbell's Co's financial strength indicators present some concerning insights about the company's balance sheet health. The Campbell's Co has an interest coverage ratio of 3.89, which positions it worse than 68.4% of 1,459 companies in the Consumer Packaged Goods industry. This ratio highlights potential challenges the company might face when handling its interest expenses on outstanding debt. It's worth noting that the esteemed investor Benjamin Graham typically favored companies with an interest coverage ratio of at least five.

The company's Altman Z-Score is just 1.83, which is below the safe threshold of 2.99. Although this does not imply immediate danger of financial distress, the stock may face some financial struggles if the Altman Z-score drops below 1.81.

Additionally, the company's low cash-to-debt ratio at 0.11 indicates a struggle in handling existing debt levels. Furthermore, the company's debt-to-Ebitda ratio is 5.21, which is above Joel Tillinghast's warning level of 4 and is worse than 79.45% of 1,494 companies in the Consumer Packaged Goods industry. Tillinghast said in his book “Big Money Think's Small: Biases, Blind Spots, and Smarter Investing” that a high debt-to-Ebitda ratio can be a red flag unless tangible assets cover the debt.

Conclusion

The Campbell's Co's financial strength, profitability, and growth metrics, as highlighted by the GF Score, suggest potential underperformance in the future. While the company has a rich history and a diverse product portfolio, its current financial indicators raise concerns about its ability to maintain its past success. Investors should carefully consider these factors when evaluating the company's future prospects. For those interested in exploring companies with stronger GF Scores, GuruFocus Premium members can use the following screener link: GF Score Screen.

This article, generated by GuruFocus, is designed to provide general insights and is not tailored financial advice. Our commentary is rooted in historical data and analyst projections, utilizing an impartial methodology, and is not intended to serve as specific investment guidance. It does not formulate a recommendation to purchase or divest any stock and does not consider individual investment objectives or financial circumstances. Our objective is to deliver long-term, fundamental data-driven analysis. Be aware that our analysis might not incorporate the most recent, price-sensitive company announcements or qualitative information. GuruFocus holds no position in the stocks mentioned herein.