It is not good to over-promise and under-deliver on Wall Street. Terex (NYSE:TEX) is a prime example. It previously guided the Street to expect $5 EPS in 2016. But due to the latest $2.35 to $2.50 EPS guidance in 2014, it is almost impossible for Terex to achieve the $5 EPS goal in 2016. As a result, Terex was sold off and provided an unique investment opportunity for long-term investors. Further research shows Terex has already implemented a self-help restructuring program. With margin improvement towards 5% net margins, there is 30% upside potential to invest in Terex. Combined with positive outlook for the non-residential construction recovery, the investment in Terex becomes even more appealling. If we can look through the current disappointing guidance and invest for 2015 and beyond, Terex does provide a favorable risk/reward profile for prospective investors.

Company Overview

Terex is a lifting and material handling solution company with the focus on operation improvement. The company is geographically diverse: 41% North America, 32% Western Europe, 11% Asia, 6% Latin America, and 9% the rest of the world, or "ROW." It has five segments: 35% Aerial Work Platforms (AWP), 23% Cranes, 22% Material Handling & Port Solutions (MHPS), 12% Construction, and 9% Materials Processing (MP).

Terex published a good overview PDF file named "Introduction to Terex Corporation" on its website. There are many photos showing Terex's products. As the saying goes, a picture is worth a thousand words. I posted a few important products of TEX below:

(click to enlarge)

(click to enlarge)

Source: Company Presentation

Terex was founded in 1925 and is based in Westport, Connecticut. More detail about the history of the company can be found on the company website.

Why did TEX decline?

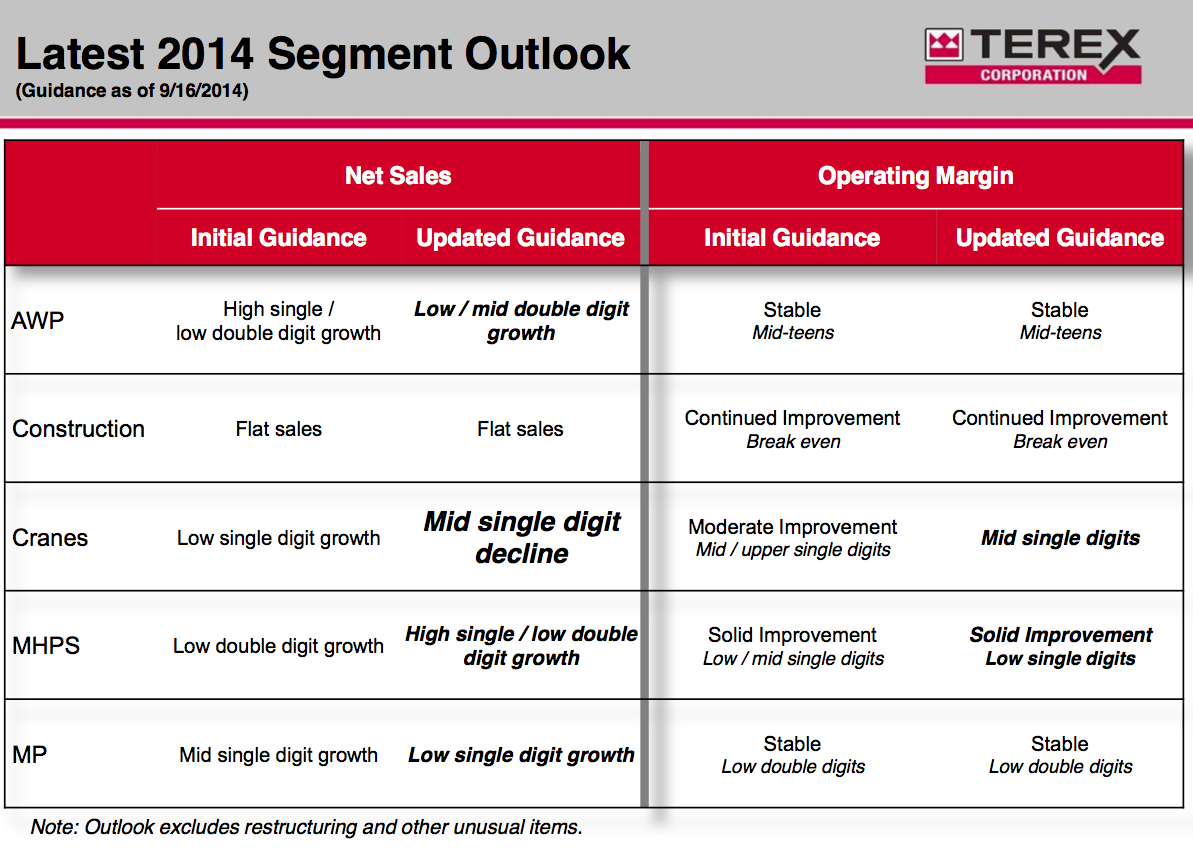

The main reason for the decline is the lowered full year outlook guidance for 2014 per-share earnings of $2.35 to $2.50 versus the previous forecast of $2.50 to $2.80. This is a significant decline in EPS, and it is no wonder that Terex's share price decreased accordingly.

In addition, the following bolds the text for any changes in the forecast. As we can see, the cranes business changed to mid single-digit decline for net sales from low single-digit growth, and to mid single-digits operating margin from moderate improvement mid-to-upper single digits.

(click to enlarge)

Source: Company Presentation

All in all, the expectation was clearly reset, and the decline in share price reflected such negative revisions. As there are still self-help initiatives to control costs, which are still on target as the management team discussed, I believe that Terex provides compelling valuation given its expected growth in EPS beyond 2015. To put the potential of EPS into perspective, the Terex previously stated a $5 EPS goal for 2016. Although the EPS goal will certainly be postponed, Terex should still be capable of growing its current $2.35 - $2.50 EPS in 2014 towards its $5 EPS goal. As we can see, there is still plenty of growth ahead for the EPS to expand. Despite the recent setback in guidance, prospective investors should not rule out the EPS growth potential from its currently reduced EPS in 2014.

From an objective point of view, Stifel, a brokerage and investment firm, stated that the recent pullback provided a favorable risk/reward profile. The following excerpt is from Stifel:

Our feeling is that expectations have been sufficiently reset, which should allow for this later cycle name to outperform as end markets continue to firm into 2015 and beyond. While demand conditions remain mixed, we believe the market has already discounted end market uncertainty.

Valuation

I am interested in Terex because of the growth prospects in 2015 and beyond. Terex has already stated that it expected significant growth potential ahead as its sales currently are at around 65% of its peak level.

(click to enlarge)

Source: Company Presentation

As shown above, Terex's two main markets are both in good shape. For the North American market, the sales have been in an upward trend since 2009. For the Western European market, despite the sales being near the trough due to the weak business climate in Europe, it seems to form a bottom. Indeed, Terex is well positioned for any European recovery in 2015 and beyond. For the ROW, there is no clear pattern. Nevertheless, the management team explained that this was due to the focus on profitable growth. I admit that the ROW is worth monitoring. If there is further deterioration in the ROW business without any positive developments in both the North America and Europe to offset, I will re-evaluate my Buy thesis on Terex.

I forecast that Terex can grow its sales to $7.7 billion in 2015 from its current $7.3 billion. With the restructuring program, I expect the company can revert back to about 5% net profit margins. This results in $375 million net profit in 2015. As Terex used to trade in the range between 11x and 16x P/E multiples, I utilize 13x P/E to attain my target price of $42, which implies 30% upside potential.

From the free cash flow perspective, Terex confirmed it would generate $200-250 million free cash flow in 2014. By taking the mid-point of $225 million, Terex currently trades at 6% free cash flow yield, which should give support to the current depressed share price for a well-established lifting and material handling solution company.

For the cash flow analysis, I would like to point out that Terex built up its account receivables from $594 million in 2009 to $1.3 billion in 2014. This shows that Terex consumed a lot of free cash flow to fund the account receivables for the past five years. But on the positive side, Terex stated it would achieve $200-250 million free cash flow in 2014. In the future, I will pay attention to the free cash flow and see whether the account receivables decrease or not. Plus, would Terex need any additional free cash flow to fund any working capital needs in the foreseeable future? If so, I would again re-evaluate whether Terex is a good long-term investment.

Source: Gurufocus.com

Finally, I would like to provide the DCF analysis calculated by Gurufocus.com. It shows that TEX has 11% margin of safety.

Positive Outlook

Other than an attractive valuation and 30% upside potential, Terex can ride the non-residential recovery wave. According to the latest press release from Ashtead, an international equipment rental company with national networks in the U.S. and the U.K., it provided the following comment about the broad market:

The nature of the work in the early stage of what appears to be a strong non-residential recovery

If non-residential market recovers as Astead expected, there will be sales growth and margins expansion opportunities for Terex.

Financial Strength

TEX has $364 million cash on the balance sheet with about $600 million in untapped revolving credit lines. Currently, Terex has $1.9 billion in debt. After deducting the cash, the net debts are about $1.5 billion. Given Terex has $664 million EBITDA, the debt/EBIDTA ratio is approximately 2.3x, which should be manageable and close to the company's historical debt leverage ratio. In addition, since Terex has $600 million in untapped revolving credit lines, it should have enough liquidity for any business needs.

Management Team

(click to enlarge)

Source: Company Presentation

The above gives a good overview of the CEO and CFO of Terex. A point worth mentioning is that the CEO, Ronald DeFeo, has taken the role as Chief Operating Officer since 1993 and as Chief Executive Officer since 1995. He has over a decade of experience serving senior management roles within Terex.

Kevin Bradley joined Terex in 2005 and has almost a decade of experience with the company. Prior to Terex, Bradley worked for GE Commercial Finance (previously GE Capital).Â

According to the latest proxy statement, DeFeo holds 1.4% ownership as shown below:

(click to enlarge)

Source: Proxy Statement

The ownership shows the confidence DeFeo in Terex's future prospects.

Risks

First, Terex relies on the economic recovery to drive sales of lifting and material handling products. In particular, Europe is still struggling. As Europe is one of the important markets for Terex, if Europe does not recover as expected, the sales and profit margins for the firm will decline. Second, the restructuring program poses executive risk. The restructuring program might be delayed or may not achieve the anticipated margins and earnings benefit. Third, please refer to the risks section of the 10K to further understand the business risk investing in Terex.

The Bottom Line

I have been paying attention to the machinery industry, especially the crane and Ariel work platform segments. I also wrote an article about Oshkosh (NYSE:OSK) before. Because Terex recently traded close to its 52 weeks low, it triggered me to look further into the industry and Terex particularly. Despite the risk involved in cyclical names, such as Oshkosh and Terex, I found that the risk/reward is very attractive as the industry outlook is still bright for investors looking beyond 2015. I believe Terex is a well-run company and deserves to trade 30% higher than the current share price.

Disclosure: I am not a securities broker/dealer or an investment adviser. I am currently long TEX. You are responsible for your own investment decisions. All information contained should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.