Wells Fargo has commenced coverage on Compass (COMP, Financial), assigning it an Equal Weight rating alongside a price target of $8. The financial institution's analysis, which includes agent checks and a review of the total addressable market, points to a multi-year potential for Compass to expand its agent roster. Additionally, the company has a promising mergers and acquisitions pipeline that could fuel further growth.

However, Wells Fargo remains cautious about Compass's ability to enhance commission splits effectively, as well as the prospects of its Private Exclusive strategy. Due to these factors, the firm's estimates align closely with broader market consensus, suggesting a balanced but cautious outlook for the stock.

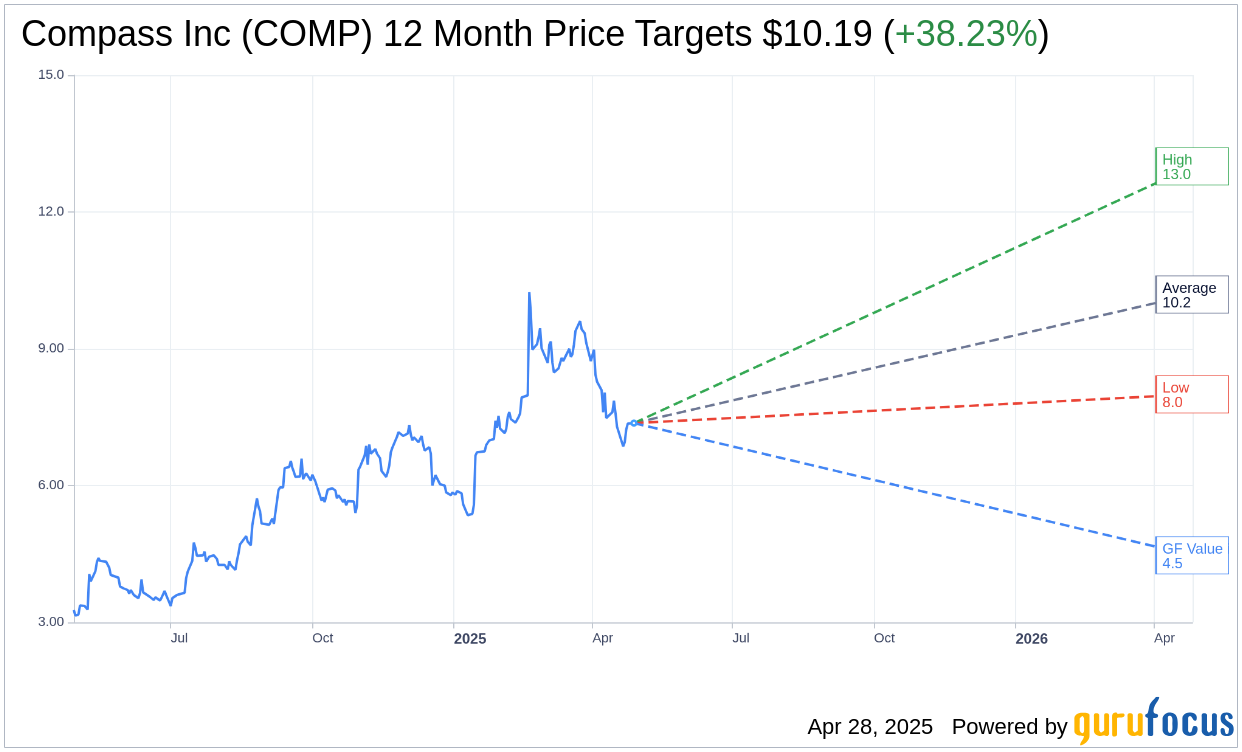

Wall Street Analysts Forecast

Based on the one-year price targets offered by 8 analysts, the average target price for Compass Inc (COMP, Financial) is $10.19 with a high estimate of $13.00 and a low estimate of $8.00. The average target implies an upside of 38.23% from the current price of $7.37. More detailed estimate data can be found on the Compass Inc (COMP) Forecast page.

Based on the consensus recommendation from 8 brokerage firms, Compass Inc's (COMP, Financial) average brokerage recommendation is currently 2.4, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Compass Inc (COMP, Financial) in one year is $4.47, suggesting a downside of 39.35% from the current price of $7.37. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Compass Inc (COMP) Summary page.

COMP Key Business Developments

Release Date: February 18, 2025

- Revenue: $1.38 billion in Q4, a 25.9% increase year-over-year.

- Adjusted EBITDA: $16.7 million in Q4, including $4.2 million in M&A transaction costs.

- Net Loss: $40.5 million in Q4, improved from a $83.7 million loss a year ago.

- Free Cash Flow: $26.7 million in Q4, compared to negative $41 million last year.

- Gross Transaction Value: $54 billion in Q4, a 29.2% increase year-over-year.

- Commissions and Related Expenses: 82.53% of revenue in Q4, up 82 basis points from last year.

- Principal Agent Count: Grew by 21% year-over-year, with 3,069 net new agents in 2024.

- Title and Escrow Attach Rate: Improved by over 800 basis points year-over-year.

- Market Share: Increased from 4.41% to 5.06% in Q4, a 65 basis point gain year-over-year.

- Q1 2025 Revenue Guidance: $1.35 billion to $1.475 billion.

- Q1 2025 Adjusted EBITDA Guidance: $11 million to $25 million.

- Full Year 2024 Revenue: $5.6 billion, a 15% increase year-over-year.

- Full Year 2024 Adjusted EBITDA: $126 million, a record for Compass.

- Cash and Cash Equivalents: $234 million at the end of Q4.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Compass Inc (COMP, Financial) reported a 25.9% year-over-year increase in revenue for Q4 2024, significantly outpacing the overall market growth.

- The company achieved a record level of adjusted EBITDA and free cash flow for the full year 2024, marking the first year of positive free cash flow.

- Compass Inc (COMP) successfully recruited 669 principal agents organically in Q4, maintaining a strong retention rate of 96.9%.

- The acquisition of Christie's International Real Estate is expected to contribute approximately $500 million in annual revenue, enhancing Compass Inc (COMP)'s high-margin affiliate business.

- The company's three-phase marketing strategy, including Compass Private Exclusives and Compass Coming Soon, has shown to improve closed prices by 2.9% on average, benefiting both agents and clients.

Negative Points

- Compass Inc (COMP) faces potential challenges from higher mortgage rates and a volatile market environment, which could impact future growth.

- The company's commissions and related expenses as a percentage of revenue increased by 82 basis points year-over-year, indicating potential margin pressure.

- Despite strong agent recruitment, the net increase in principal agent count was lower due to managing out non-producing agents.

- The integration of recent acquisitions, such as Christie's International Real Estate, may present operational challenges and require significant resources.

- Compass Inc (COMP) anticipates some split degradation among higher-producing agents, which could affect overall profitability.