Wedbush analyst Jay McCanless has elevated TRI Pointe (TPH, Financial) from a Neutral to an Outperform rating, simultaneously increasing the price target from $38 to $43. This upgrade stems from the firm's confidence in TRI Pointe’s strategic initiatives and market positioning.

Key factors influencing this decision include TRI Pointe's ongoing share repurchase efforts, which are seen as a positive for investors. Additionally, Wedbush considers the company's financial projections for fiscal year 2025 to be within reach. The analyst also notes robust demand from move-up and active adult segments as a driving force behind the upgrade.

Wedbush has been zeroing in on companies with exposure to move-up and active adult buyers since late 2024, a category where TRI Pointe is prominently positioned. The firm predicts that issues related to community development that affected fiscal year 2024 will not spill over into the next seven quarters, potentially smoothing the path for continued growth. This positive outlook underlines the reasons for the revised recommendation and increased price target for TRI Pointe (TPH, Financial).

Wall Street Analysts Forecast

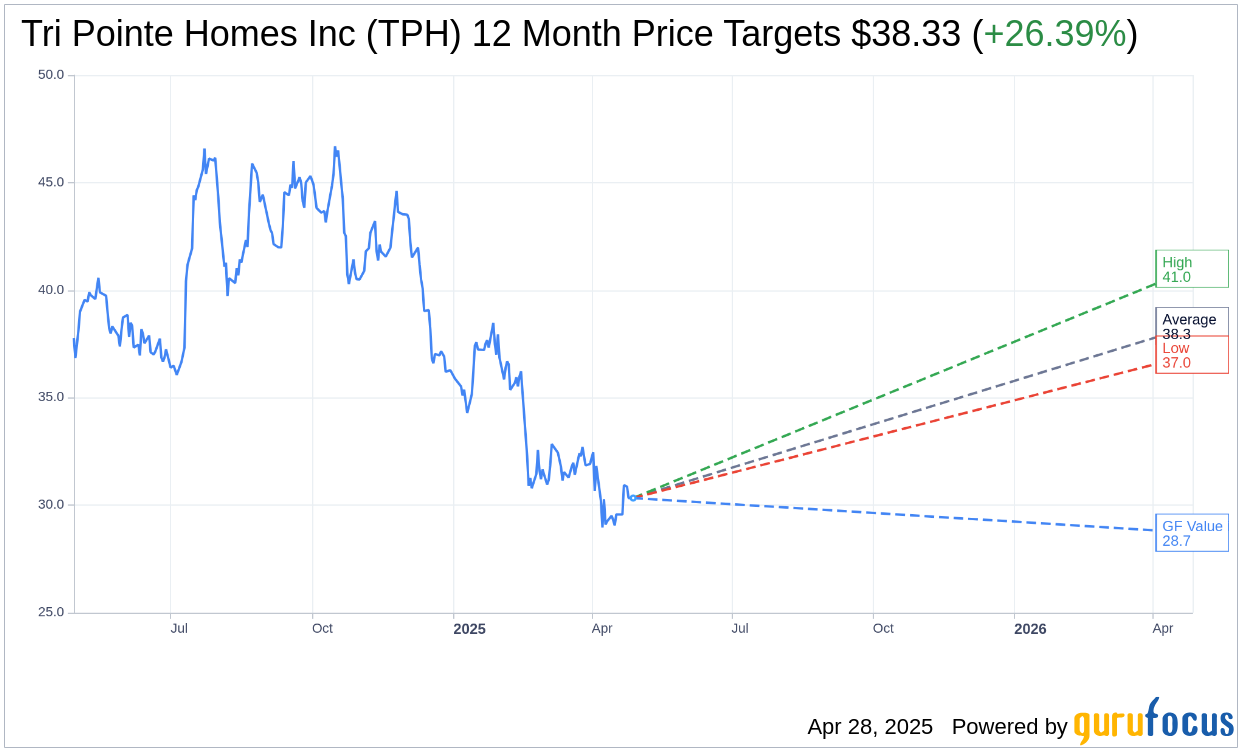

Based on the one-year price targets offered by 6 analysts, the average target price for Tri Pointe Homes Inc (TPH, Financial) is $38.33 with a high estimate of $41.00 and a low estimate of $37.00. The average target implies an upside of 26.39% from the current price of $30.33. More detailed estimate data can be found on the Tri Pointe Homes Inc (TPH) Forecast page.

Based on the consensus recommendation from 7 brokerage firms, Tri Pointe Homes Inc's (TPH, Financial) average brokerage recommendation is currently 2.1, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Tri Pointe Homes Inc (TPH, Financial) in one year is $28.72, suggesting a downside of 5.31% from the current price of $30.33. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Tri Pointe Homes Inc (TPH) Summary page.

TPH Key Business Developments

Release Date: February 18, 2025

- Home Sales Revenue: $1.2 billion in the fourth quarter of 2024.

- Homebuilding Gross Margin: Improved by 40 basis points year over year to 23.3% in Q4 2024.

- SG&A as a Percentage of Home Sales Revenue: 10.3% in Q4 2024.

- Pretax Margin: 14% in Q4 2024.

- Net Income: $129 million or $1.37 per diluted share in Q4 2024.

- Full-Year Net Income: $458 million or $4.83 per diluted share, a 40% increase year over year.

- Operating Cash Flows: Record high in 2024.

- Senior Notes Redemption: $450 million redeemed in 2024.

- Return on Average Equity: 14.5% for 2024, a 270-basis point improvement over the previous year.

- Book Value Per Share Growth: Increased by 14.5% year over year.

- Share Repurchase: 4 million shares repurchased in 2024; new $250 million authorization announced in December 2024.

- Liquidity: Approximately $1.7 billion at the end of Q4 2024.

- Homebuilding Debt-to-Capital Ratio: 21.6% at the end of Q4 2024.

- Homebuilding Net Debt to Net Capital Ratio: Negative 1.6% at the end of Q4 2024.

- Active Selling Communities: 145 at the end of 2024; expected to end 2025 with 150 to 160.

- Lots Owned or Controlled: Over 36,000, a 14% increase compared to the previous year.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Tri Pointe Homes Inc (TPH, Financial) delivered a strong fourth quarter with 1,748 new homes and $1.2 billion in home sales revenue.

- The company achieved a record high of 6,460 new homes delivered in 2024, with a 40% year-over-year increase in net income.

- Tri Pointe Homes Inc (TPH) has made significant geographic diversification gains, particularly in Texas and the Carolinas.

- The company has a strong balance sheet with $1.7 billion in liquidity and a negative 1.6% homebuilding net debt to net capital ratio.

- Tri Pointe Homes Inc (TPH) has a robust land position, owning or controlling over 36,000 lots, a 14% increase from the previous year.

Negative Points

- The company experienced softer seasonal sales trends in the third and fourth quarters, leading to a lower backlog for 2025.

- Elevated mortgage rates and economic uncertainties have caused some consumers to stay on the sidelines.

- Incentives increased to 7% in the fourth quarter to move completed inventory, indicating pressure on pricing.

- The company anticipates a lower homebuilding gross margin for 2025, ranging from 20.5% to 22%, compared to 23.3% in 2024.

- Tri Pointe Homes Inc (TPH) faces potential political uncertainties and operating headwinds that could impact consumer confidence and demand.