Bank of America has increased its price target for Seagate (STX, Financial) from $112 to $120 while maintaining a Buy rating on the stock. This decision follows Seagate's impressive fiscal third-quarter results, which stood out despite prevailing supply shortages. Analysts believe that these results suggest the hard disk drive (HDD) market, alongside Seagate, has potential for continued positive performance across several upcoming quarters. Additionally, there is an indication that the HDD industry's growth cycle still has a considerable way to go before reaching its peak.

Wall Street Analysts Forecast

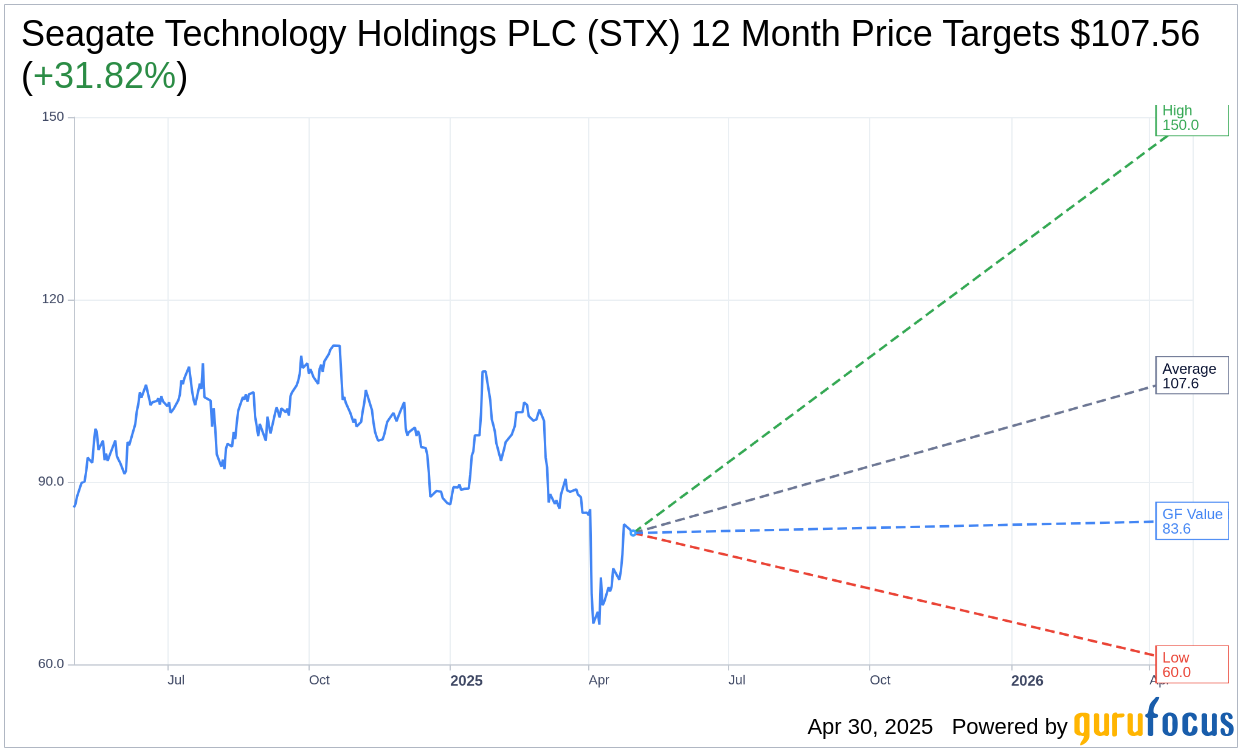

Based on the one-year price targets offered by 19 analysts, the average target price for Seagate Technology Holdings PLC (STX, Financial) is $107.56 with a high estimate of $150.00 and a low estimate of $60.00. The average target implies an upside of 31.82% from the current price of $81.60. More detailed estimate data can be found on the Seagate Technology Holdings PLC (STX) Forecast page.

Based on the consensus recommendation from 24 brokerage firms, Seagate Technology Holdings PLC's (STX, Financial) average brokerage recommendation is currently 2.2, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Seagate Technology Holdings PLC (STX, Financial) in one year is $83.61, suggesting a upside of 2.46% from the current price of $81.6. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Seagate Technology Holdings PLC (STX) Summary page.

STX Key Business Developments

Release Date: April 29, 2025

- Revenue: $2.16 billion, down 7% sequentially, but a 31% year-on-year increase.

- Non-GAAP Gross Margin: 36.2%, expanded by 70 basis points sequentially and over 1,000 basis points year-over-year.

- Non-GAAP Operating Margin: 23.5% of revenue, increased sequentially.

- Non-GAAP EPS: $1.90, at the top end of guidance range.

- Free Cash Flow: $216 million, up from $150 million in the prior period.

- Hard Drive Revenue: $2 billion, down 8% sequentially.

- Mass Capacity Revenue: $1.7 billion, a 48% year-on-year increase.

- Nearline Shipments: 120 exabytes, down 5% sequentially, up 55% year-on-year.

- Non-GAAP Gross Profit: $781 million, compared to $825 million in the prior quarter.

- Non-GAAP Operating Expenses: $274 million, down 5% quarter-over-quarter.

- Adjusted EBITDA: $563 million, doubling year-on-year.

- Non-GAAP Net Income: $407 million.

- Capital Expenditures: $43 million for the quarter.

- Debt Balance: $5.1 billion, with a net leverage ratio of 2.1 times.

- June Quarter Revenue Outlook: Expected to be $2.4 billion, plus or minus $150 million.

- June Quarter Non-GAAP EPS Outlook: Expected to be $2.40, plus or minus $0.20.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Seagate Technology Holdings PLC (STX, Financial) reported a 31% year-on-year increase in revenue and an 81% growth in non-GAAP gross profit dollars.

- The company expanded its gross margin for the eighth consecutive quarter, achieving the third highest operating margin in its history.

- Seagate's HAMR-based Mozaic drives, the industry's only 3 terabyte per disk products, are ramping up volume to qualified customers.

- The company has strong demand visibility into the first half of calendar 2026, with new build-to-order agreements being negotiated.

- Seagate is effectively managing its debt, having retired approximately $536 million during the quarter, and plans to continue reducing debt in the coming quarters.

Negative Points

- Revenue for the March quarter was down 7% sequentially, limited by temporary supply constraints.

- Mass capacity shipments were down 5% sequentially, despite a 50% year-on-year increase.

- There is potential risk from tariffs, which could impact customer buying decisions and financial performance in future quarters.

- Non-GAAP operating expenses are expected to increase in the September quarter due to an additional week in the period.

- The company faces challenges in maintaining supply-demand balance and managing operational issues that previously affected supply.