TD Cowen has adjusted its price target for OneMain (OMF, Financial) to $56, down from a previous target of $57, while maintaining a Buy rating. This revision follows the company's first-quarter results, which surpassed the firm's initial expectations.

Wall Street Analysts Forecast

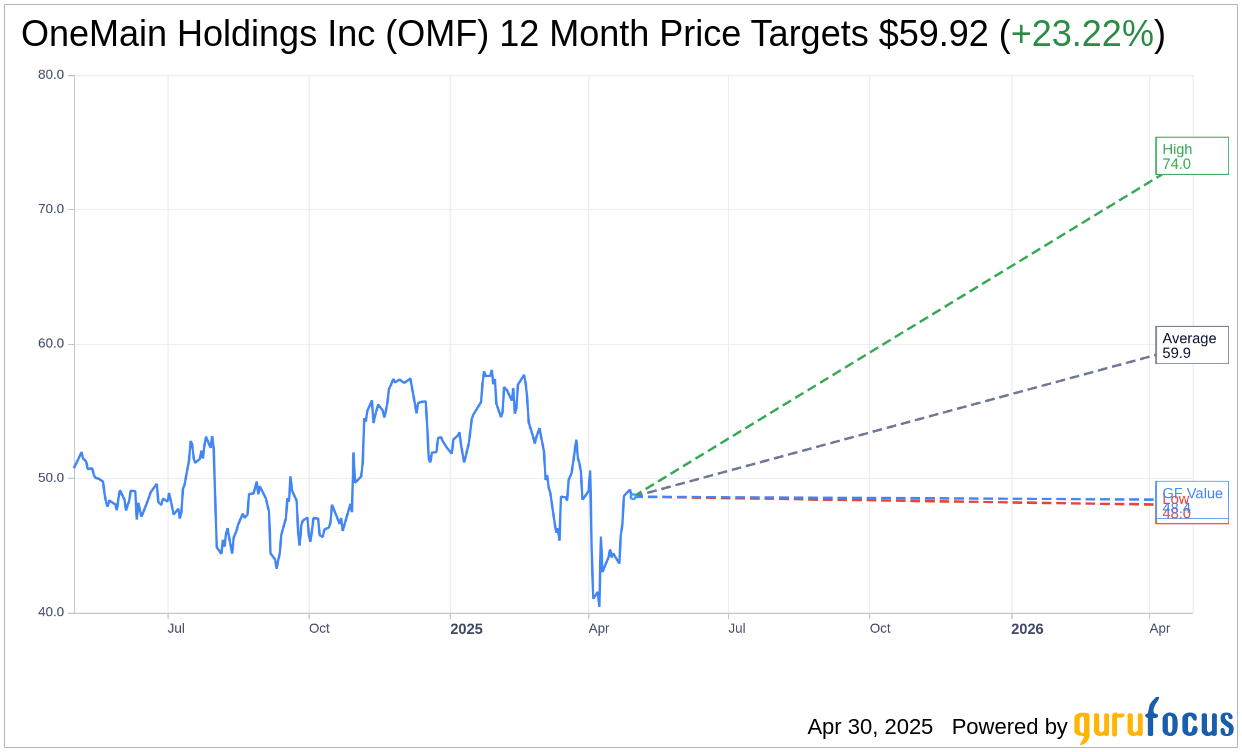

Based on the one-year price targets offered by 13 analysts, the average target price for OneMain Holdings Inc (OMF, Financial) is $59.92 with a high estimate of $74.00 and a low estimate of $48.00. The average target implies an upside of 23.22% from the current price of $48.63. More detailed estimate data can be found on the OneMain Holdings Inc (OMF) Forecast page.

Based on the consensus recommendation from 16 brokerage firms, OneMain Holdings Inc's (OMF, Financial) average brokerage recommendation is currently 2.0, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for OneMain Holdings Inc (OMF, Financial) in one year is $48.40, suggesting a downside of 0.47% from the current price of $48.63. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the OneMain Holdings Inc (OMF) Summary page.

OMF Key Business Developments

Release Date: April 29, 2025

- Capital Generation: $194 million, up 25% year over year.

- C&I Adjusted Earnings: $1.72 per share, up 19%.

- Receivables Growth: 12% year over year.

- Total Revenue: Grew 10% year over year.

- Originations Growth: 20% overall, 13% organic.

- 30+ Delinquency Rate: 5.08%, down 49 basis points year over year.

- C&I Net Charge Offs: 8.2%, down 49 basis points year over year.

- Consumer Loan Net Charge Offs: 7.8%, down 75 basis points year over year.

- GAAP Net Income: $213 million or $1.78 per diluted share, up 38% from the previous year.

- Managed Receivables: $24.6 billion, up 12% year over year.

- Interest Income: $1.3 billion, grew 11% year over year.

- Interest Expense: $311 million, up $35 million from the previous year.

- Operating Expenses: $401 million, up 11% year over year.

- Net Leverage: 5.5 times, slightly below last quarter.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Capital generation increased by 25% year over year, reaching $194 million.

- C&I adjusted earnings per share rose by 19% to $1.72.

- Receivables grew by 12% year over year, contributing to a 10% increase in total revenue.

- Originations increased by 20%, driven by high-quality customer acquisition and product innovation.

- Positive credit trends continued, with a decrease in delinquencies and net charge-offs, indicating improved credit performance.

Negative Points

- The macroeconomic environment remains uncertain, posing potential risks to future performance.

- Interest expense increased by $35 million compared to the previous year, due to higher average debt and cost of funds.

- The credit card net charge-off rate remains high at 19.8%, although it is expected to stabilize in the long term.

- The application for an industrial loan company (ILC) is pending, with no guarantee of approval, which could impact strategic plans.

- Operating expenses increased by 11% year over year, partly due to the inclusion of foresight expenses.