In its first-quarter financial report, Illinois Tool Works (ITW, Financial) announced revenues of $3.8 billion, which fell slightly short of the market consensus of $3.84 billion. Despite this, the company's leadership expressed confidence in its ability to exceed expectations due to effective strategic execution. ITW has decided to uphold its 2025 financial guidance, anticipating that its current pricing strategies will counterbalance any tariff-related cost challenges.

The company’s President and CEO, Christopher A. O’Herlihy, highlighted ITW's resilience in the face of external market uncertainties. He attributed this strength to the firm’s strategy of manufacturing largely in the regions where its products are sold, coupled with a decentralized operational model that enhances the ability to quickly adapt to changing market conditions. Additionally, ITW prides itself on a diverse and high-quality business portfolio that provides stability.

O’Herlihy stressed the importance of ITW's strong financial position, which supports ongoing strategic investments and facilitates continuous progress towards long-term goals. A core component of ITW's strategy is leveraging Customer-back Innovation to drive organic growth that surpasses market averages, reinforcing the company's commitment to outperforming in the current economic climate.

Wall Street Analysts Forecast

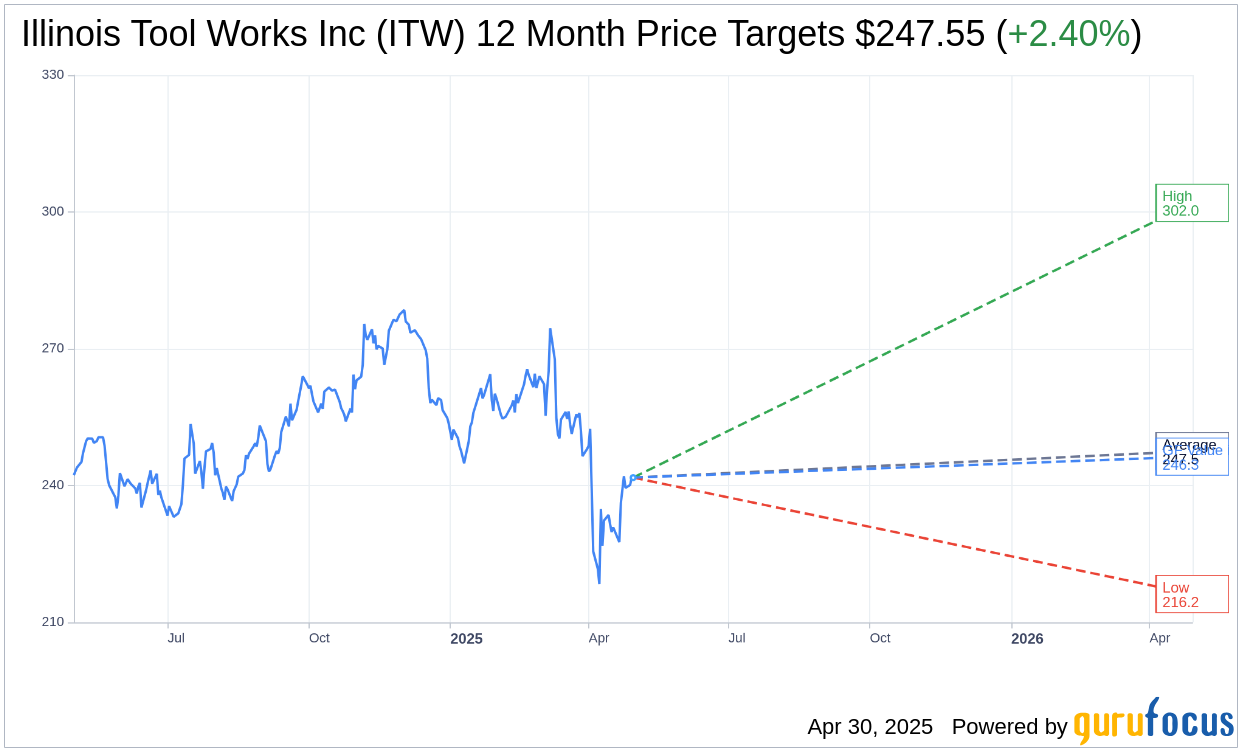

Based on the one-year price targets offered by 15 analysts, the average target price for Illinois Tool Works Inc (ITW, Financial) is $247.55 with a high estimate of $302.00 and a low estimate of $216.22. The average target implies an upside of 2.40% from the current price of $241.75. More detailed estimate data can be found on the Illinois Tool Works Inc (ITW) Forecast page.

Based on the consensus recommendation from 20 brokerage firms, Illinois Tool Works Inc's (ITW, Financial) average brokerage recommendation is currently 3.1, indicating "Hold" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Illinois Tool Works Inc (ITW, Financial) in one year is $246.34, suggesting a upside of 1.9% from the current price of $241.75. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Illinois Tool Works Inc (ITW) Summary page.

ITW Key Business Developments

Release Date: February 05, 2025

- GAAP EPS: Improved 7% to $2.54.

- Organic Revenue: Declined 0.5%; positive 0.4% excluding product line simplification.

- Operating Income: $1.03 billion, an increase of 4%.

- Operating Margin: Record 26.2%, up 140 basis points.

- Free Cash Flow: Increased 10% with a conversion to net income of 133%.

- Automotive OEM Margins: Improved by 230 basis points to 19.6% for the full year.

- Food Equipment Organic Growth: Almost 3.5%.

- Test & Measurement and Electronics Organic Revenue: Up 2%.

- Welding Operating Margin: 31.2%, a 160 basis point improvement.

- Polymers & Fluids Organic Revenue: Grew 1%.

- Construction Products Organic Growth: Down 4%.

- Specialty Products Operating Margin: Record 28.4% for the quarter.

- Dividend Increase: Raised by 7%, marking the 61st consecutive year.

- Shareholder Returns: Over $3.2 billion returned in dividends and share repurchases.

- 2025 EPS Guidance: Projected range of $10.15 to $10.55.

- 2025 Organic Growth Projection: 0% to 2%, or 1% to 3% excluding strategic PLS.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Illinois Tool Works Inc (ITW, Financial) achieved record financial results in 2024, including EPS, margins, and returns, outperforming underlying end markets.

- The company reported a record operating margin of 26.2%, an increase of 140 basis points, driven by enterprise initiatives.

- Free cash flow increased by 10% with a conversion to net income of 133%, supported by strong working capital management.

- The Automotive OEM segment improved margins by 230 basis points to 19.6%, with expectations of further outperformance in 2025.

- Customer-back innovation (CBI) initiatives showed progress, with patent filings increasing by 18% in 2024, positioning ITW for future growth.

Negative Points

- Organic revenue declined by 0.5% in Q4 2024, with a 0.9% reduction due to strategic product line simplification.

- Foreign currency translation negatively impacted revenue by 1%, contributing to a total revenue decline of 1.3%.

- The Construction Products segment experienced a 4% decline in organic growth due to a challenging market environment.

- The company faces nonoperational headwinds in 2025, including a $0.30 impact from foreign currency translation.

- ITW's guidance for 2025 includes a modest organic growth projection of 1% to 3%, reflecting current demand levels and seasonality.