Citi has adjusted its price target for Bausch + Lomb (BLCO, Financial) from $14 down to $13 while maintaining a Neutral rating on the company's shares. This decision follows the release of BLCO's Q1 report. Citi highlights a $20 million EBITDA tariff impact, which, although not mentioned in the company's guidance, has been factored into their financial model.

Wall Street Analysts Forecast

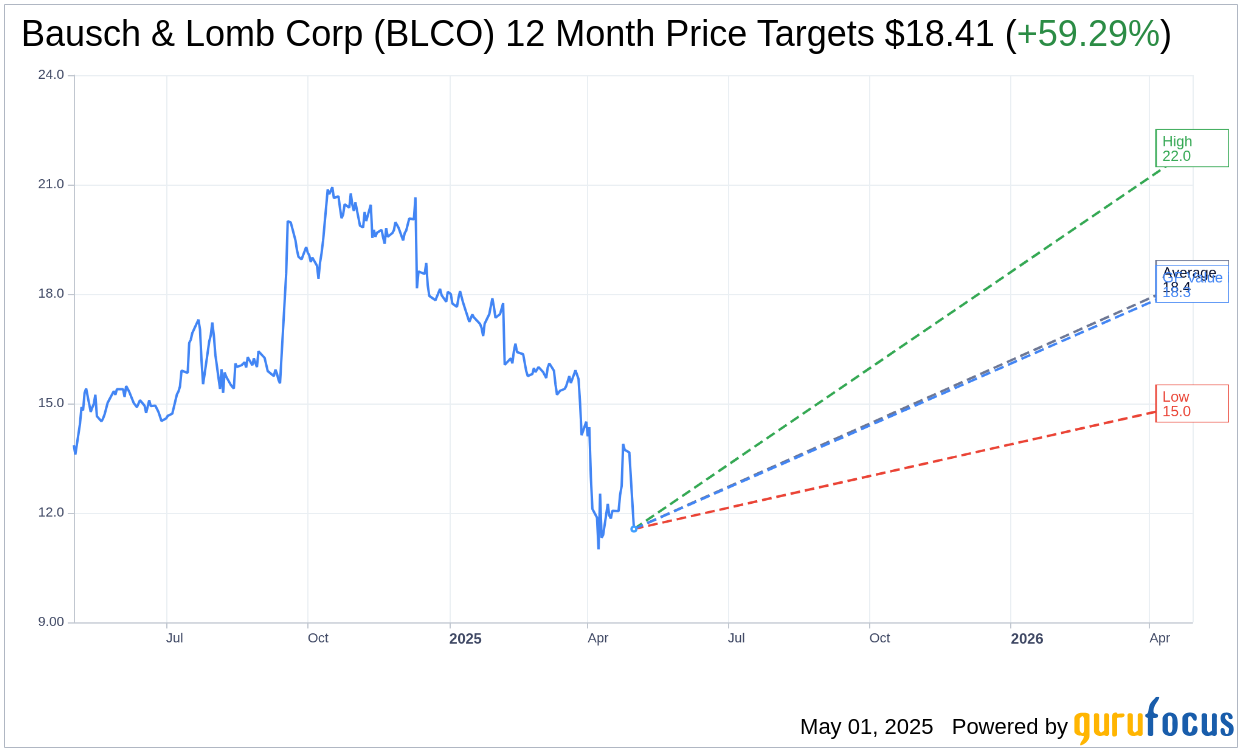

Based on the one-year price targets offered by 12 analysts, the average target price for Bausch & Lomb Corp (BLCO, Financial) is $18.41 with a high estimate of $22.00 and a low estimate of $15.00. The average target implies an upside of 59.29% from the current price of $11.56. More detailed estimate data can be found on the Bausch & Lomb Corp (BLCO) Forecast page.

Based on the consensus recommendation from 13 brokerage firms, Bausch & Lomb Corp's (BLCO, Financial) average brokerage recommendation is currently 2.6, indicating "Hold" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Bausch & Lomb Corp (BLCO, Financial) in one year is $18.28, suggesting a upside of 58.13% from the current price of $11.56. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Bausch & Lomb Corp (BLCO) Summary page.

BLCO Key Business Developments

Release Date: April 30, 2025

- Total Revenue: $1.137 billion, reflecting 5% growth.

- Vision Care Revenue: $656 million, increased by 5%.

- Surgical Segment Revenue: $214 million, an increase of 11%.

- Pharma Segment Revenue: $267 million, growth of 1%.

- Adjusted Gross Margin: 59.5%, including a one-time headwind of 140 basis points due to the enVista recall.

- Adjusted EBITDA: $126 million, including a one-time impact of $16 million related to inventory write-off from the enVista recall.

- Net Interest Expense: $91 million.

- Adjusted EPS: Loss of $0.07 per share, excluding IPR&D.

- 2025 Revenue Guidance: Raised to $5 billion to $5.1 billion.

- 2025 Adjusted EBITDA Guidance: Updated to $850 million to $900 million.

- Currency Impact: $19 million headwind to revenue and $7 million to adjusted EBITDA in Q1.

- R&D Investment: $86 million in adjusted R&D for Q1.

- Tariff Impact: Estimated potential headwind of 120 basis points to adjusted EBITDA margin in 2025.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Bausch & Lomb Corp (BLCO, Financial) reported mid-single-digit constant currency revenue growth in the first quarter, aligning with industry growth expectations.

- The Vision Care segment saw a 5% revenue increase, driven by strong performance in both consumer and contact lenses, with Daily SiHy contact lenses growing by 42%.

- The Surgical segment experienced an 11% revenue increase, with premium IOLs contributing significantly to this growth.

- Miebo, a key product in the Pharmaceuticals segment, delivered $57 million in revenue, showing sequential growth of 8% and year-over-year growth of over 100%.

- The company successfully managed a voluntary recall of enVista IOLs, demonstrating strong operational resilience and a commitment to patient safety, with a quick return to market.

Negative Points

- The Pharmaceuticals segment faced challenges, with the US Generics business declining by 23% due to increased competition and lower inventory levels.

- Xiidra, despite strong prescription growth, faced headwinds from higher gross to net deductions, impacting its financial performance.

- The enVista IOL recall is expected to have a one-time negative impact of approximately $55 million on revenue and $65 million on adjusted EBITDA for 2025.

- Tariffs pose a potential headwind of approximately 120 basis points to adjusted EBITDA margin in 2025, with ongoing uncertainty around their impact.

- Currency fluctuations were a headwind, reducing revenue by approximately $19 million and adjusted EBITDA by $7 million in the first quarter.