B. Riley has adjusted the price target for MSA Safety (MSA, Financial) from $200 to $195 while maintaining a Buy rating on the stock. This decision follows the release of MSA's first-quarter report, where the company posted sales and earnings exceeding expectations, though the gross margin fell short. The firm revised its estimates in response to these results.

Wall Street Analysts Forecast

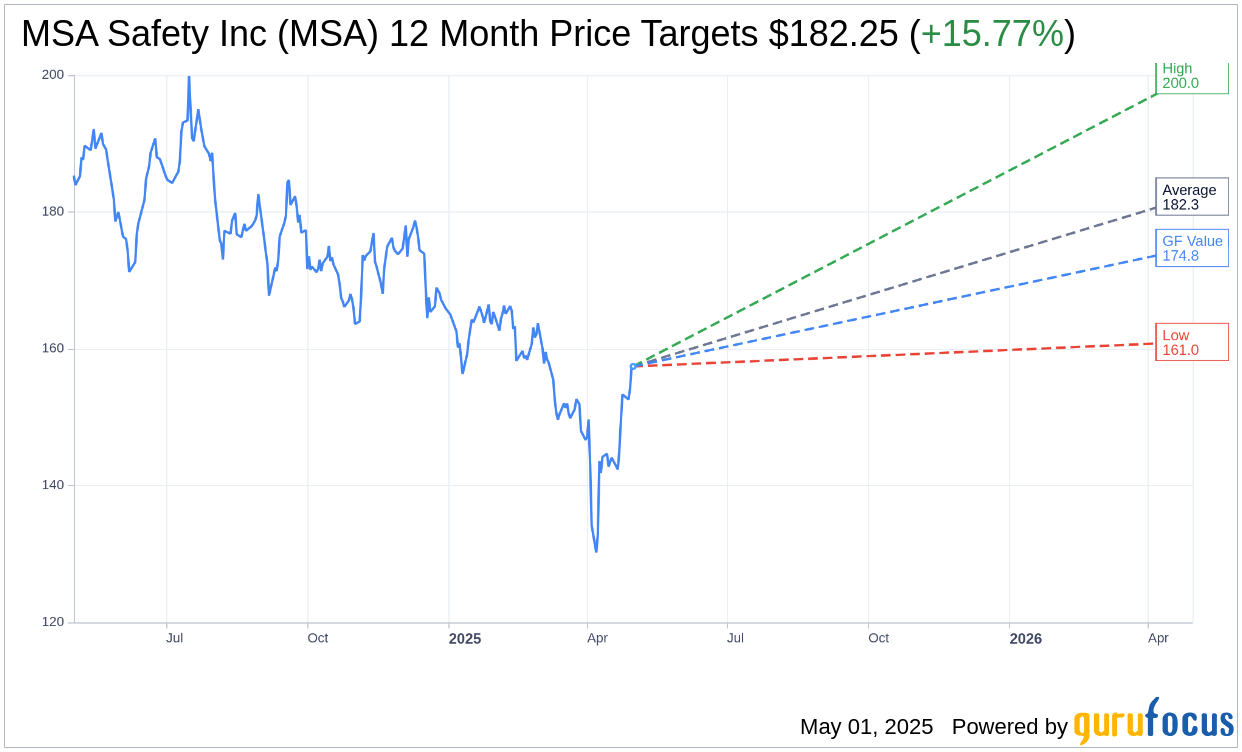

Based on the one-year price targets offered by 4 analysts, the average target price for MSA Safety Inc (MSA, Financial) is $182.25 with a high estimate of $200.00 and a low estimate of $161.00. The average target implies an upside of 15.77% from the current price of $157.42. More detailed estimate data can be found on the MSA Safety Inc (MSA) Forecast page.

Based on the consensus recommendation from 5 brokerage firms, MSA Safety Inc's (MSA, Financial) average brokerage recommendation is currently 2.2, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for MSA Safety Inc (MSA, Financial) in one year is $174.75, suggesting a upside of 11.01% from the current price of $157.42. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the MSA Safety Inc (MSA) Summary page.

MSA Key Business Developments

Release Date: April 30, 2025

- Revenue: $421 million, an increase of 2% reported and 4% organic over the prior year.

- Gross Margin: 45.9%, down 140 basis points from last year.

- Operating Margin: GAAP operating margin at 18.5%; adjusted operating margin at 20.8%, down 50 basis points year over year.

- Net Income: $60 million or $1.51 per share GAAP; adjusted diluted earnings per share at $1.68, up 4% from last year.

- Free Cash Flow: $51 million, with a conversion rate of 86%.

- Segment Performance - Americas: Sales decreased 1% reported, up 1% organic; adjusted operating margin at 26.8%, down 240 basis points.

- Segment Performance - International: Sales increased 9% reported, 11% organic; adjusted operating margin at 14.6%, up 310 basis points.

- Adjusted EBITDA: $470 million for the trailing 12 months, 25.9% of net sales.

- Net Debt: $331 million, including cash of $171 million.

- Order Trends: Healthy order pace with a quarterly book-to-bill ratio above 1.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- MSA Safety Inc (MSA, Financial) exceeded original expectations for the first quarter of 2025, delivering solid free cash flow generation.

- The company experienced strong demand across its Detection product category, contributing to higher sales.

- International growth was up double digits organically, particularly in the Asia Pacific region.

- MSA Safety Inc (MSA) secured a $10 million breathing apparatus contract from the Orange County Fire Authority, marking a key competitive conversion.

- The company successfully amended and increased its revolving credit facility to $1.3 billion, providing ample liquidity for growth initiatives.

Negative Points

- Operating margins declined year over year due to gross margin pressure from transactional foreign currency headwinds.

- Sales in the Fire Service category were down high single digits year over year, primarily due to challenging comparables in the Americas segment.

- Gross margin was impacted by inflation and foreign exchange headwinds, particularly from Latin American currencies.

- The company faces increased macroeconomic uncertainty and global tariff activity, which could present risks to growth outlook.

- Tariffs have become a significant concern, with about 15% of the cost of sales now subject to tariffs, impacting long-term strategic planning.