BofA has started covering Taylor Morrison (TMHC, Financial) with a Buy recommendation, setting a price target of $70. According to the firm, Taylor Morrison stands favorably in the challenging housing sector due to its focus on wealthier clients and minimal involvement with first-time homebuyers. The company's strategy to grow organically after completing seven acquisitions since 2013 is viewed positively by the firm.

Wall Street Analysts Forecast

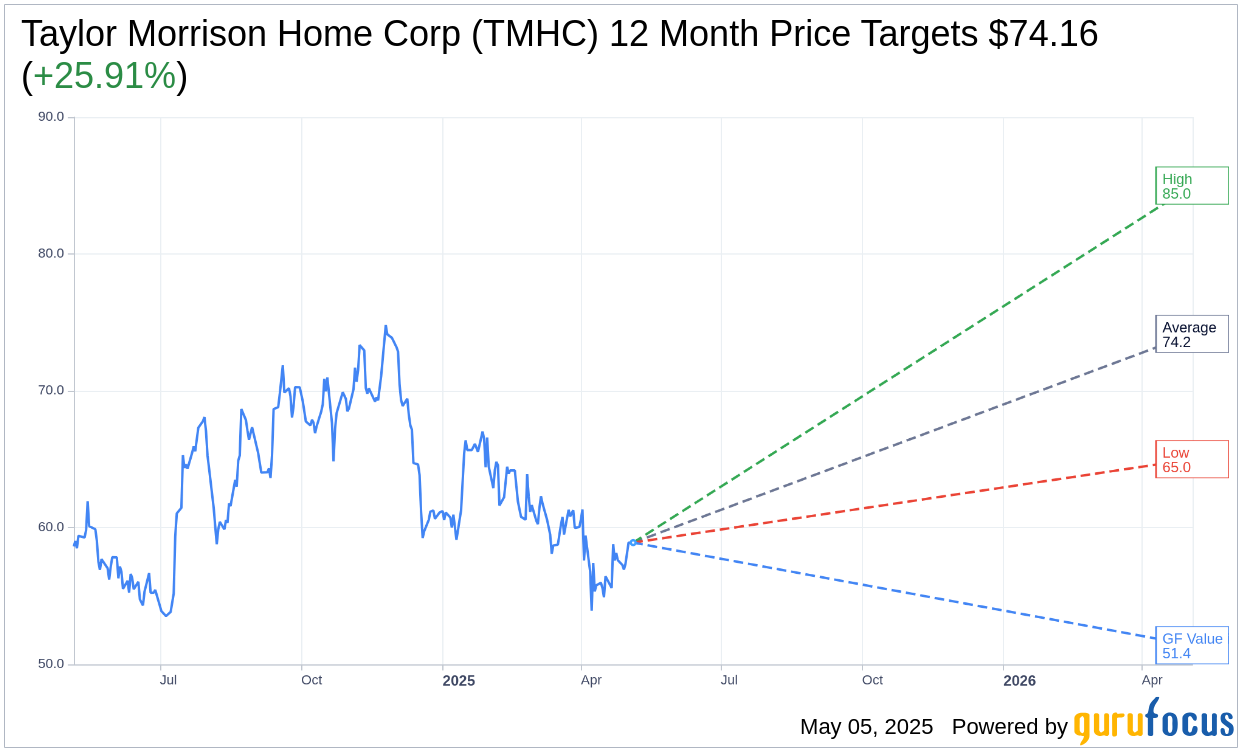

Based on the one-year price targets offered by 7 analysts, the average target price for Taylor Morrison Home Corp (TMHC, Financial) is $74.16 with a high estimate of $85.00 and a low estimate of $65.00. The average target implies an upside of 25.91% from the current price of $58.90. More detailed estimate data can be found on the Taylor Morrison Home Corp (TMHC) Forecast page.

Based on the consensus recommendation from 10 brokerage firms, Taylor Morrison Home Corp's (TMHC, Financial) average brokerage recommendation is currently 1.9, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Taylor Morrison Home Corp (TMHC, Financial) in one year is $51.40, suggesting a downside of 12.73% from the current price of $58.9. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Taylor Morrison Home Corp (TMHC) Summary page.

TMHC Key Business Developments

Release Date: April 23, 2025

- Home Closings Revenue: $1.8 billion, up 12% year over year.

- Adjusted Home Closings Gross Margin: 24.8%, up 80 basis points year over year.

- Adjusted Earnings Per Diluted Share: Increased 25%.

- Book Value Per Share: Grew 16% to approximately $58.

- Net Income: $213 million or $2.07 per diluted share; adjusted net income was $225 million or $2.18 per diluted share.

- Closings Volume: 3,048 homes, up 12% year over year.

- Average Closing Price: $600,000, roughly flat from a year ago.

- Monthly Absorption Pace: Increased to 3.3 per community from 2.6 in the fourth quarter.

- SG&A as a Percentage of Home Closings Revenue: 9.7%, down 70 basis points from a year ago.

- Financial Services Revenue: $51 million with a gross margin of 44.7%.

- Liquidity: Approximately $1.3 billion, including $378 million of unrestricted cash.

- Net Homebuilding Debt to Capitalization Ratio: 20.5% at quarter end.

- Share Repurchases: 2.2 million shares for $135 million; targeting $350 million for 2025.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Taylor Morrison Home Corp (TMHC, Financial) delivered 3,048 homes at an average price of $600,000, generating $1.8 billion in home closings revenue, up 12% year over year.

- The company's adjusted earnings per diluted share increased by 25%, and book value per share grew 16% to approximately $58.

- TMHC's diversified consumer and product strategy contributed to volume and margin resiliency, with a strong performance in the resort lifestyle segment.

- The company effectively used personalized finance incentives, with 42% of first-quarter closings utilizing a forward commitment, aiding first-time home buyers.

- TMHC maintained a strong balance sheet with over $1 billion in liquidity and a net homebuilding debt to capitalization ratio of 20.5%.

Negative Points

- The monthly absorption pace decreased to 3.3 per community from 3.7 a year ago, indicating a slowdown in sales velocity.

- Entry-level sales declined steeply by 21%, reflecting challenges in this consumer segment.

- Finished inventory at quarter-end was elevated, leading to a higher anticipated spec penetration in the second quarter.

- The company expects incentives to rise more meaningfully in the second quarter, impacting margins.

- TMHC revised its home closings gross margin forecast to around 23% for the year, down from previous expectations.