Peabody Energy anticipates a second-quarter coal volume of 4.0 million tons, with exports comprising 2.5 million tons. Within this export total, 0.8 million tons are currently priced at about $77 per ton. Additionally, 1.0 million tons of Newcastle-based products and 0.7 million tons of high ash products have yet to be priced. The expected cost per ton ranges between $45 and $50.

The company's President and CEO, Jim Grech, notes that the second quarter typically reflects reduced thermal coal demand due to seasonal factors. However, the outlook remains robust, with all planned production for 2025 in the Powder River Basin already sold. Furthermore, metallurgical coal prices have experienced a recovery from their March lows.

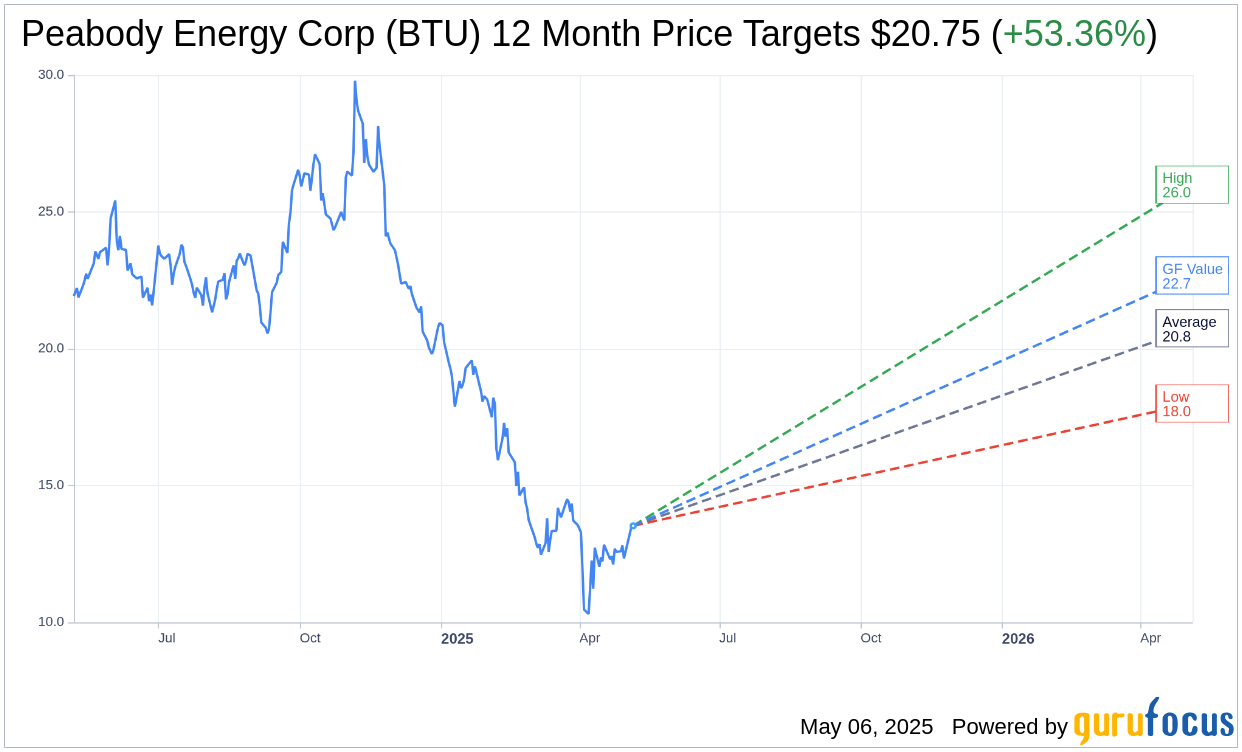

Wall Street Analysts Forecast

Based on the one-year price targets offered by 4 analysts, the average target price for Peabody Energy Corp (BTU, Financial) is $20.75 with a high estimate of $26.00 and a low estimate of $18.00. The average target implies an upside of 53.36% from the current price of $13.53. More detailed estimate data can be found on the Peabody Energy Corp (BTU) Forecast page.

Based on the consensus recommendation from 4 brokerage firms, Peabody Energy Corp's (BTU, Financial) average brokerage recommendation is currently 1.8, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Peabody Energy Corp (BTU, Financial) in one year is $22.68, suggesting a upside of 67.63% from the current price of $13.53. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Peabody Energy Corp (BTU) Summary page.

BTU Key Business Developments

Release Date: February 06, 2025

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Peabody Energy Corp (BTU, Financial) reported a strong finish to 2024 with solid fourth-quarter results despite facing geologic and pricing challenges.

- The company successfully shipped its first coal from the Centurion mine and agreed to acquire multiple premium hard coking coal mines from Anglo American.

- Peabody Energy Corp (BTU) returned $221 million to shareholders in 2024 while continuing to reinvest in the business.

- The company set a new record for the lowest accident rates in its 140-plus-year history and reclaimed 70% more land than it disturbed.

- Peabody Energy Corp (BTU) achieved the top rating for governance by ratings firm ISS, highlighting its strong governance practices.

Negative Points

- Seaborne met coal prices have increased by 45% in the past year, but U.S. coal demand has not yet caught up with the expected uplift from growing domestic power demand.

- The company faced geologic challenges at its 20 Mile mine, impacting production, although increased production is now taking hold.

- Peabody Energy Corp (BTU) anticipates lower Seaborne thermal volumes in 2025 due to reduced production at Wilpinjong and the closing of the Wambo underground mine.

- The company recorded a $41 million non-cash charge for the remeasurement of its Australian balance sheet due to a lower Australian dollar exchange rate.

- Peabody Energy Corp (BTU) faces challenges with the new 15% tariff on U.S. coal imports to China, potentially impacting its business and Seaborne markets.