Enerflex (EFXT, Financial) has announced robust financial results for the first quarter, reporting an adjusted EBITDA of $113 million. This represents a significant rise from the $69 million recorded in the same quarter of the previous year, though slightly lower than the $121 million posted in the last quarter of 2024. The company's Energy Infrastructure and After-Market Services segments continue to show consistent performance, underscoring Enerflex’s capacity to yield sustainable returns globally.

The backlog for Enerflex’s product line at the end of Q1 2025 reached $1.2 billion, indicating a strong demand pipeline. While the company remains vigilant regarding fluctuating market conditions, it is confident in the underlying factors driving its growth, such as global energy security and the transition to low-emissions natural gas.

Additionally, Enerflex made progress in improving its financial health by repaying $74 million of debt in the first quarter, which decreased its leverage ratio to 1.3 times. This strategic move reflects effective operational execution and disciplined capital management. The company is focused on enhancing profitability, fortifying core operations, and delivering consistent, favorable returns to its shareholders.

Wall Street Analysts Forecast

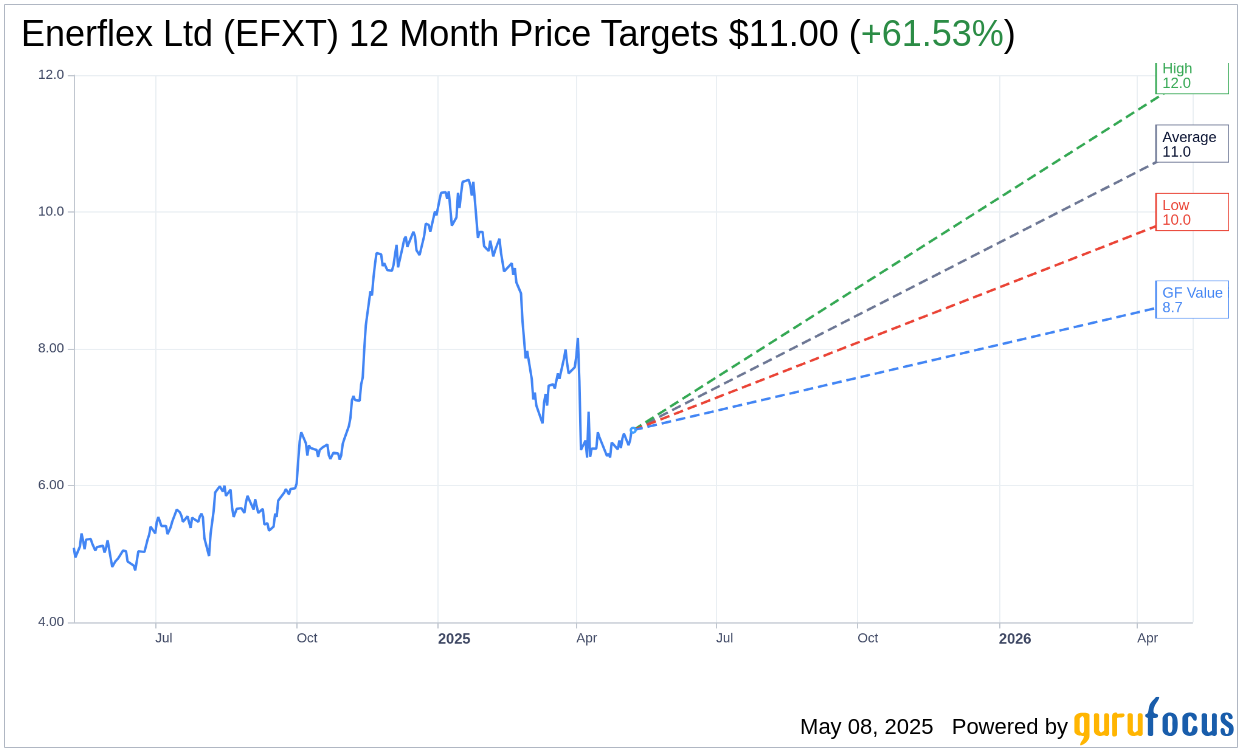

Based on the one-year price targets offered by 2 analysts, the average target price for Enerflex Ltd (EFXT, Financial) is $11.00 with a high estimate of $12.00 and a low estimate of $10.00. The average target implies an upside of 61.53% from the current price of $6.81. More detailed estimate data can be found on the Enerflex Ltd (EFXT) Forecast page.

Based on the consensus recommendation from 2 brokerage firms, Enerflex Ltd's (EFXT, Financial) average brokerage recommendation is currently 2.5, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Enerflex Ltd (EFXT, Financial) in one year is $8.72, suggesting a upside of 28.05% from the current price of $6.81. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Enerflex Ltd (EFXT) Summary page.

EFXT Key Business Developments

Release Date: February 27, 2025

- Consolidated Revenue: $561 million in Q4 2024, compared to $574 million in Q4 2023 and $601 million in Q3 2024.

- Gross Margin Before Depreciation and Amortization: $174 million or 31% of revenue in Q4 2024, compared to $158 million or 28% in Q4 2023.

- Adjusted EBITDA: $121 million in Q4 2024, compared to $91 million in Q4 2023.

- Net Debt: $616 million at the end of Q4 2024, with $92 million in cash and available liquidity of $614 million.

- Free Cash Flow: $76 million in Q4 2024, compared to $139 million in Q4 2023.

- SG&A Expenses: $92 million in Q4 2024, up $18 million year-over-year.

- Contract Backlog: $1.5 billion for Energy Infrastructure assets and $1.3 billion for Engineered Systems.

- Energy Infrastructure Gross Margin Before D&A: $86 million in Q4 2024, compared to $87 million in Q4 2023.

- After-market Services Gross Margin Before D&A: 22% in Q4 2024.

- Capital Expenditures: $47 million in Q4 2024, with $32 million for maintenance and $15 million for expansion.

- Dividend Payout: $2 million returned to shareholders in Q4 2024, with a 50% increase announced for Q1 2025.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Enerflex Ltd (EFXT, Financial) delivered strong operational performance across its geographies and product lines, with Energy Infrastructure and After-market Services generating 69% of gross margin before depreciation and amortization in 2024.

- The company achieved a rapid deleveraging of its balance sheet, reaching the low end of its target leverage range at 1.5 times by the end of 2024, down from 2.3 times at the end of Q4 2023.

- Enerflex Ltd (EFXT) has a robust contract backlog, with $1.5 billion for Energy Infrastructure assets and $1.3 billion for Engineered Systems, supporting future revenue streams.

- The US contract compression business showed strong operational performance with utilization in the mid-90% range and plans to grow the fleet from 428,000 horsepower to over 475,000 horsepower in 2025.

- Enerflex Ltd (EFXT) plans to increase direct shareholder returns, including a 50% increase in dividends starting Q1 2025, reflecting confidence in its financial position.

Negative Points

- Geopolitical tensions and potential tariffs pose risks, although Enerflex Ltd (EFXT) is working to mitigate these impacts through diversified operations and proactive risk management.

- Engineered Systems gross margin is expected to normalize to historical averages in 2025 due to weaker natural gas prices and a shift in project mix.

- SG&A expenses increased by $18 million year-over-year, partly due to increased share-based compensation and a bad debt recovery in the previous year.

- Free cash flow decreased to $76 million in Q4 2024 from $139 million in Q4 2023, reflecting changes in working capital recovery.

- The company anticipates a modest unwind in working capital in 2025, which could impact cash flow stability.