Canaccord has revised its price target for Middleby (MIDD, Financial), reducing it from $200 to $186 while maintaining a Buy rating on the stock. The adjustment follows the company's first-quarter performance, where its revenue fell approximately 4% short of market forecasts. However, Middleby exceeded the earnings per share expectations by about 5%. The firm's decision to lower the target reflects adjustments to their estimates and a decreased target multiple.

Wall Street Analysts Forecast

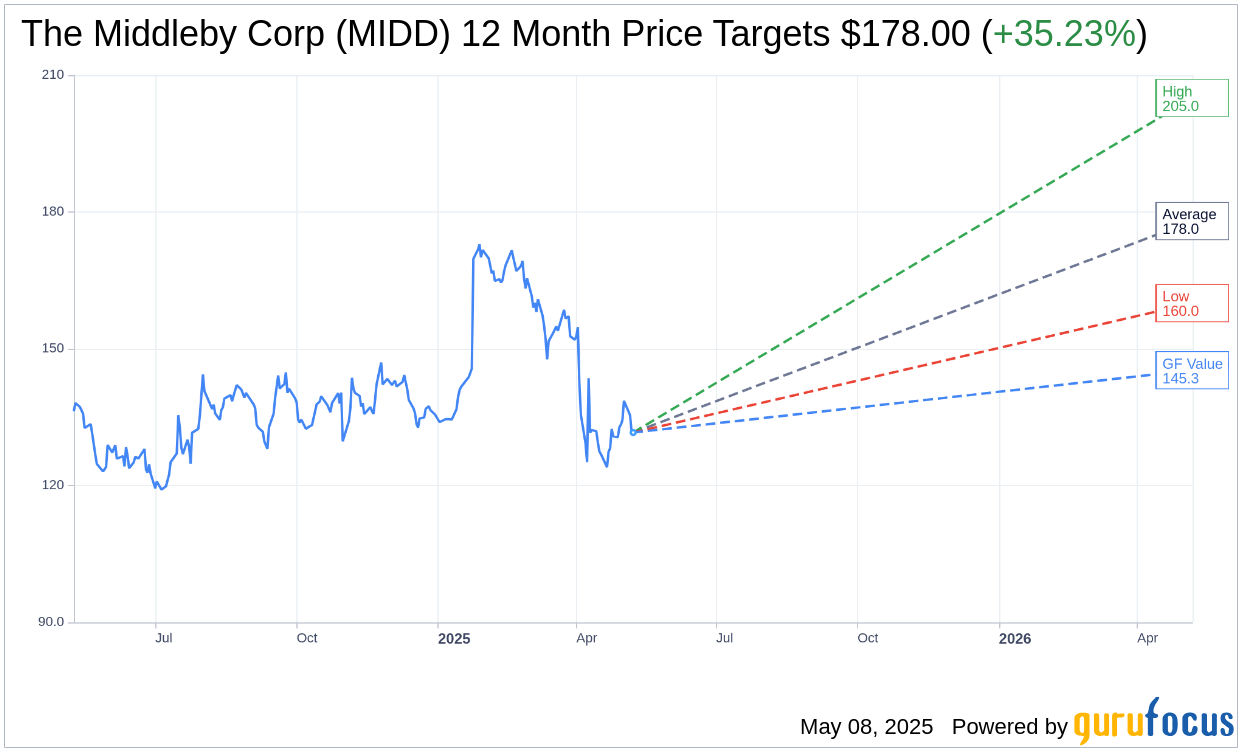

Based on the one-year price targets offered by 6 analysts, the average target price for The Middleby Corp (MIDD, Financial) is $178.00 with a high estimate of $205.00 and a low estimate of $160.00. The average target implies an upside of 35.23% from the current price of $131.63. More detailed estimate data can be found on the The Middleby Corp (MIDD) Forecast page.

Based on the consensus recommendation from 9 brokerage firms, The Middleby Corp's (MIDD, Financial) average brokerage recommendation is currently 2.4, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for The Middleby Corp (MIDD, Financial) in one year is $145.30, suggesting a upside of 10.39% from the current price of $131.63. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the The Middleby Corp (MIDD) Summary page.

MIDD Key Business Developments

Release Date: May 07, 2025

- Operating Cash Flows: Over $141 million, highest for a first quarter.

- Free Cash Flows: $107 million for the quarter, $620 million for the trailing 12 months.

- Leverage: Reduced from 3 times to 2 times over the past two years.

- Share Repurchase: Nearly $50 million in open market stock repurchases year-to-date.

- Tariff-Related Costs: Expected increase in annual expenses by approximately $150 million to $200 million.

- Revenue Adjustment: Segment composition change impacting around $10 million per quarter of revenue.

- Residential Segment Growth: Primarily attributable to outdoor products.

- Commercial Foodservice Business: Success in ice and beverage platform, offset by muted buying levels from largest chain customers.

- Food Processing Revenue: Drop in Q1 due to customer-driven delivery delays, expected sequential revenue increase in Q2.

- Residential Segment Outlook: Stability and potential growth in premium indoor brands, tariffs negatively impacting outdoor products revenue.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- The Middleby Corp (MIDD, Financial) has authorized an additional 7.5 million shares under its accelerated buyback program, reflecting confidence in the business.

- The company plans to separate its food processing business into a stand-alone public company by early 2026, aiming to unlock significant shareholder value.

- Middleby has demonstrated strong cash flow generation, with operating cash flows of over $141 million in Q1, the highest for a first quarter.

- The company is well-positioned in the market with its US-centric manufacturing footprint, providing a competitive advantage amid tariff challenges.

- Middleby continues to invest in innovation, with new products gaining traction and receiving industry awards, enhancing its market-leading position.

Negative Points

- Tariff-related costs are expected to increase annual expenses by approximately $150 million to $200 million, impacting profitability.

- Muted buying levels by large chain customers are offsetting wins in the commercial foodservice segment, affecting revenue growth.

- The food processing segment experienced a drop in revenues due to customer-driven delivery delays and lower volumes.

- Uncertainty around trade and consumer behavior is creating delays in converting opportunities into orders, challenging revenue growth.

- The residential segment faces potential negative impacts from tariffs on outdoor products, with revenue growth highly dependent on consumer sentiment.