Rapid7 (RPD, Financial) has announced its forecast for second-quarter earnings per share (EPS), estimating a range between 43 cents and 46 cents. This outlook surpasses the market consensus, which stands at 42 cents. The company's projection indicates confidence in its financial trajectory, suggesting potential strength against prevailing market uncertainties.

Wall Street Analysts Forecast

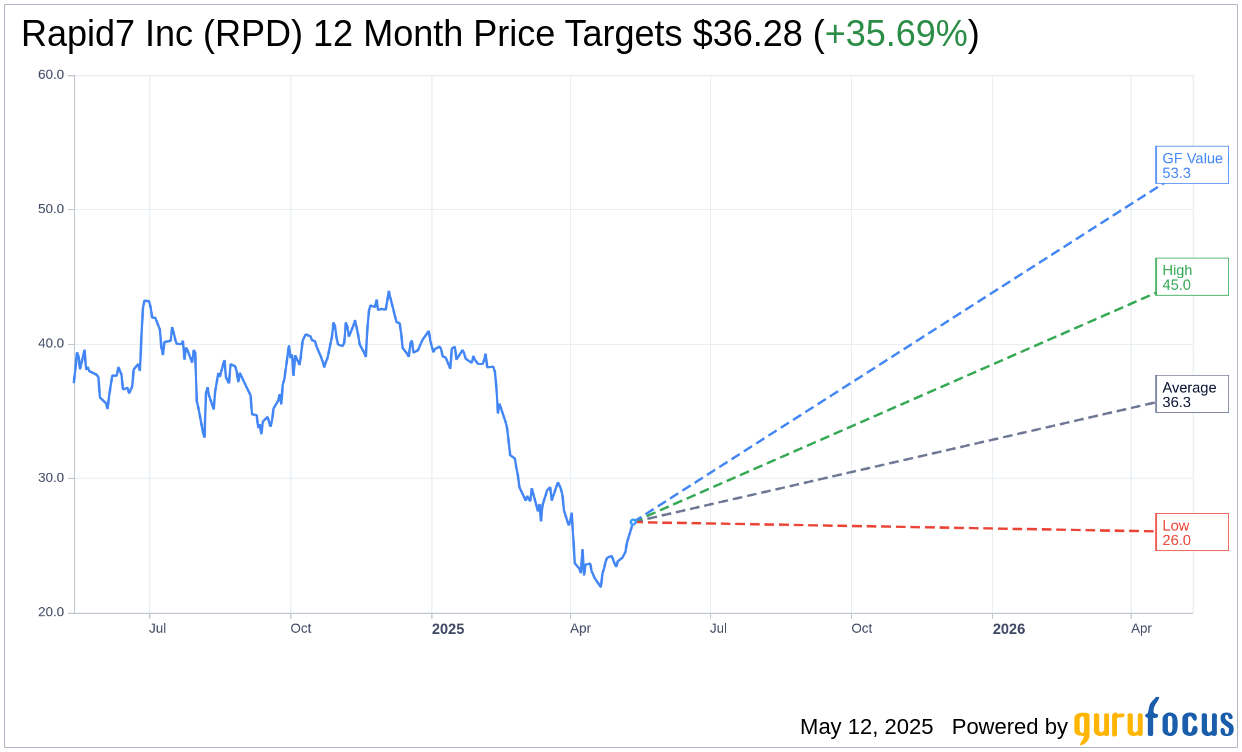

Based on the one-year price targets offered by 20 analysts, the average target price for Rapid7 Inc (RPD, Financial) is $36.28 with a high estimate of $45.00 and a low estimate of $26.00. The average target implies an upside of 35.69% from the current price of $26.74. More detailed estimate data can be found on the Rapid7 Inc (RPD) Forecast page.

Based on the consensus recommendation from 25 brokerage firms, Rapid7 Inc's (RPD, Financial) average brokerage recommendation is currently 2.5, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Rapid7 Inc (RPD, Financial) in one year is $53.33, suggesting a upside of 99.44% from the current price of $26.74. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Rapid7 Inc (RPD) Summary page.

RPD Key Business Developments

Release Date: February 12, 2025

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Rapid7 Inc (RPD, Financial) ended 2024 with $840 million in ARR, growing 4% over the prior year, in line with their outlook.

- Revenue and operating income exceeded guided ranges, with over $150 million in free cash flow generated for the year.

- The detection and response business delivered double-digit growth, ending the year with over $400 million in ARR.

- The company made substantial progress in scaling its partner ecosystem, booking 80-90% of new ARR through the channel.

- Rapid7 Inc (RPD) achieved significant milestones in cloud security adoption with the release of Exposure Command, driving over 20% year-over-year growth in risk and exposure management pipeline generation.

Negative Points

- Rapid7 Inc (RPD) acknowledged that recent growth has not kept pace with broader security demand.

- The vulnerability management landscape is facing intense competition and cloud migration, leading to secular pressure and increased churn.

- The company experienced challenges in managing the transition from traditional vulnerability management to integrated security operations.

- There is uncertainty and disruption with certain state, local, educational, and healthcare customers affecting ARR growth expectations.

- The managed service component of the business comes with lower gross margins due to its labor-intensive nature.