I don’t comment often on broader market trends, macroeconomics, interest rate changes, or much of anything else that is out of my control and ultimately has little to do my long-term plan of building wealth.

And that’s because much of this is noise. I’ve discussed many times how important it is to ignore this noise, so I try to make sure this blog is bit of a sanctuary away from all the needless media commotion. I don’t want to tell you to ignore the noise, then spout off a bunch of noise of my own. I’d be a hypocrite and I’d also be taking time away from what matters.

What matters?

Keeping your eye on the long term. Focusing on what you can control. Keeping track of companies’ fundamentals. And going about your life.

You know what doesn’t matter?

Interest rate changes. The day-to-day stock market fluctuations. The latest quote by a talking head.

However, I thought I’d take some time today to discuss the recent broader stock market pullback. And the reason why I’m choosing to do so is to perhaps put things in perspective here and show why it’s so important to focus on high-quality companies over the long haul.

Let’s get into it!

Stocks Fluctuate

So the S&P 500 index is down 4.34% from the start of the month.

Ouch, right?

Not really.

What have we lost? Have we actually lost anything at all?

Well, I haven’t lost anything. In fact, I’ve won. And I’ll show you how that works.

My portfolio value was $170,704.39 at the start the month. That was the value of the Freedom Fund on October 1.

If you factor out some of my recent stock purchases, my portfolio value would be $165,889.97 today. That’s a drop of 2.82% since the beginning of the month. Now, I’m not going to go on about the benefits of investing in low-beta blue chip dividend growth stocks that are defensive holdings whereby they tend to drop less than the broader stock market during pullbacks or corrections, but you can kind of see how that works here.

And I’m not really going to go on about that because it’s really not important.

What is important is that I haven’t actually lost anything at all. The market value of my securities fluctuate from day to day; I know this as an investor in stocks. Stocks fluctuate. Grass is green. The sky is blue.

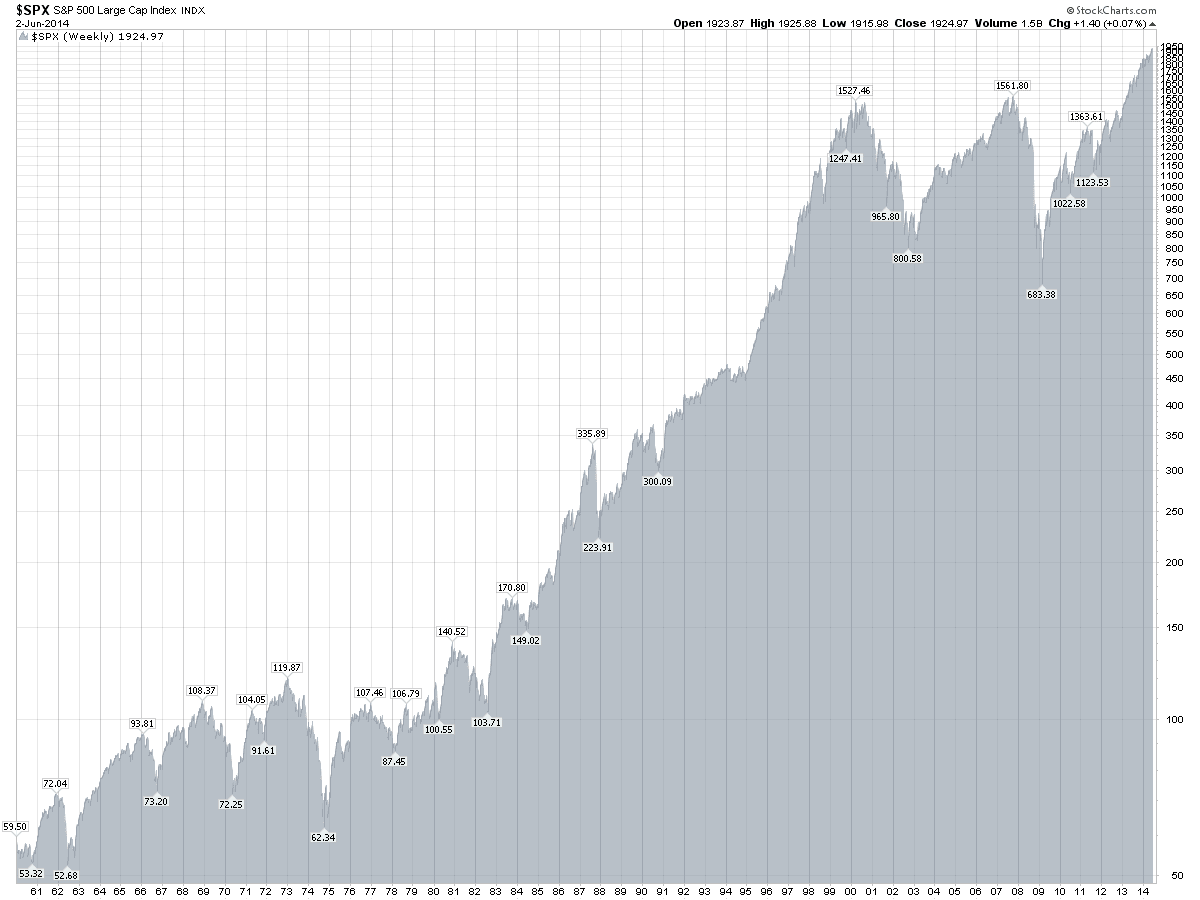

Stocks fluctuate up. They fluctuate down. However, over the long haul they tend to rise. A lot.

S&P 500 Index 1960 – Present (Weekly)

Source: StockCharts.com

I Still Own What I Own

But while the market value of my holdings have depreciated, I haven’t lost a dime. I’m not selling anything. I still own the same percentage of every company that I owned before this small pullback. I haven’t “lost” almost $5,000 since October started. I’ve actually “lost” $0.

I owned 100 shares of Johnson & Johnson (JNJ, Financial) before the market started to swoon. Guess what I still own? Those same 100 shares of JNJ.

That means my ownership stake in the company is still the same. A such, I still have the same claim to all future earnings and dividends.

So when JNJ pays out $0.70 per share in December, I’ll still collect the same $70.00 I was going to before Mr. Market became moody. My dividend income remains unchanged, and I consider my dividend income the true barometer of my success. If financial independence was a bar graph, my expenses would be the the entire bar and my dividend income would be the shaded area that shows how complete my journey to financial independence is. The value of my securities doesn’t factor into that at all.

And this exercise can be extrapolated out for all 51 stocks I own in my portfolio. None have cut their dividends. None have experienced any massive operational problems. They are basically the same as they were a month ago. Perhaps an argument could be made that some of the companies in the energy sector have experienced changing fundamentals over the last month or so as oil prices have dropped, but these aren’t the only stocks that have dropped in value lately.

Stocks are stocks. But businesses are businesses. Stocks may fluctuate up and down in price, but the ownership stakes these shares represent and the value of those stakes do not. Furthermore, large multinational companies worth hundreds of billions of dollars don’t fluctuate up and down like that on a daily basis in regards to their intrinsic value. The real value of businesses do in fact change over long periods of time, but not in the way the stock market would have you believe. And that’s because price and value are not one and the same.

Volatility Is A Synonym For Opportunity

I’d like to think that dividend growth investing is a win-win. So losing is actually winning. All this volatility is simply an opportunity.

I most recently purchased 30 shares of Unilever Plc (UL, Financial) after the stock tumbled more than 7% during the month prior to my purchase. Unilever is still pumping out butter, ice cream, soap, shampoo, and deodorant to billions of customers around the world. Nothing has changed. Yet an ownership stake in the company became more than 7% cheaper over the course of a month. And we’re talking about a company with a market cap north of $115 billion.

What happened with Unilever to where they were all of the sudden worth ~$8 billion less over the course of a month? Nothing. Which means an investor has an opportunity to buy into a world-class business for substantially less than just a month ago.

Of course, a stock’s yield rises as its share price falls. So a cheaper stock simply allows someone who’s aiming to live completely off of the dividend income their portfolio generates to get even closer to where they want/need to be. Cheaper stocks means my current capital can buy more shares, which means more dividend income to fund my dream. So while others might think a volatile stock market is a nightmare, it’s all a dream to me because I’m closer to my dream.

So this “loss” was actually a “win”. UL’s price goes down, yet I’m able to score shares at a cheaper price with a higher yield. How do you lose in that scenario?

For some reason, stocks seem to be the only thing in life that bothers people when they go down in value. If the grocery store has bread and milk on sale, nobody complains.

And stocks seem to have this unique characteristic where falling prices somehow triggers an emotional response which convinces people they must sell. You don’t sell your house immediately out of fear simply because your local real estate expert knocks on your door and tells you your house is worth 5% less today than it was last month. No, you’re going to slam the door in their face and promptly go back to whatever it was you were doing.

When stocks are cheaper, the opportunity is there for you to buy more. World-class businesses tend to sell more products and/or services, earn more money, and pay out more dividends over long periods of time. After all, you don’t build up track records of five decades or more of consecutive annual dividend raises (like Johnson & Johnson sports) if you’re not doing these things.

After all, one share of JNJ was priced at $56.59 10 years ago, and was paying out a $0.2850 dividend. The stock price has fluctuated in that 10-year time frame, and any fluctuations downward were simply opportunities to buy into one of the world’s largest healthcare companies that had already had decades upon decades of dividend raises under its belt.

But you know what isn’t volatile? Its dividend payout history:

Source: Johnson & Johnson Investor Relations

Taking Advantage Of The Opportunity

Of course, opportunity is wasted if it’s not taken advantage of. I talk all the time about deploying capital when stocks are cheap, and enjoying the opportunity to average down on stocks I already own.

And I’ve done just that since October began.

I started the month off by purchasing 110 shares in American Realty Capital Properties Inc. (ARCP, Financial). I then followed that up shortly thereafter by averaging down on my position in the world’s largest miner –BHP Billiton Plc (BBL, Financial). I waited for more than a year to add to my position in the miner, but when opportunity knocks I answer. I then completed the aforementioned acquisition of shares in Unilever.

Where does this leave me? Right about where I started.

The value of my portfolio has almost completely recovered via these recent purchases and a slightly less moody Mr. Market toward the end of last week.

However, what I tend to focus on is that chart. Over the course of one year it’s mainly up. Furthermore, when the chart drops, I’ve noticed the snap back is even more aggressive – you’ll notice that after the drop at the beginning of the year. And that’s because I own more equity in high-quality companies during the drop than I did before, right? I’m buying through these drops, which means my underlying equity ownership stakes are even larger. Moreover, these ownership stakes are bought on sale. Thus, when Mr. Market’s mood invariably improves, these stakes are perhaps revalued at a more appropriate rate, causing my portfolio’s value to correspondingly rise.

But the value of my portfolio isn’t really important. What is important is fundamentals and value of the equities I’m holding and purchasing, and the dividend income they produce.

ARCP dropped over 8% in the month preceding my purchase. Was the company worth 8% less? Had the fundamentals significantly deteriorated enough to warrant that valuation change? I believe no and no, which is why I purchased shares on sale. This one purchase alone added $110.00 to my annual dividend income. Bam!

BBL dropped almost 17% in the month preceding my purchase. This is a company with a market cap north of $150 billion. With a B. Shaving 17% off a company that large is no chump change. Was it intrinsically worth 17% less because iron ore had dropped on the back of supply/demand concerns? Is BBL somehow unlikely to be producing more iron, copper, oil, potash, and coal 10, 20, or 30 years from now? Are these natural resources, which are slowly depleting, going to be worth less three decades from now? I don’t have a crystal ball, but I like the odds this buy works out to my favor. Furthermore, this purchase added another$49.60 to my annual dividend income.

Then there’s the aforementioned UL purchase. A 7% drop on a company that produces innocuous products like soap and deodorant? Because people are all of the sudden going to stop washing their bodies and putting on deodorant? Nah, I don’t think so. This added yet another $45.50 to my annual dividend tally.

You see where I’m going here. Mr. Market gets moody and I add more than $200 to my annual dividend war chest. He might be in a bad mood, but I’m certainly not!

Conclusion

The stock market is an emotional roller coaster. Don’t let it get you sick.

Enjoy the view when it’s on the way up, and try to be more aggressive when it’s dropping.

But remember that dividend growth investors are winning either way. When stocks are up, our portfolios are humming along and all is good. When stocks are down, our capital goes further and buys more dividends with the same dollar. All along the way we’re increasing our ownership stakes by buying stocks with the capital we’re able to generate from our savings by living below our means, reinvesting our increasing dividend income back into high-quality businesses and further increasing that income, and slowly marching toward financial freedom.

If that’s not uplifting and inspiring I don’t know what is. Mr. Market can be bipolar, but I’m about as happy as a human being can be when I keep my perspective on the long term.

Keep your eye on the long term. Ignore the noise. Enjoy the ride, but take advantage of the drops when they occur. Remember that price and value are indeed different. Stick to quality.

Those chasing after financial independence are getting a helping hand when the market drops like this. Grab it.

Full Disclosure: Long JNJ, UL, ARCP, and BBL.

What do you think? Is dividend growth investing a “win-win”? Taking advantage of Mr. Market’s moodiness?

Thanks for reading.