Macquarie has revised its price target for Gambling.com (GAMB, Financial), bringing it down to $18 from the previous $19. Despite the adjustment, the firm has maintained an Outperform rating on the stock. This follows the company's release of first-quarter results, which showed a 39% increase in revenue and a 55% rise in EBITDA year-over-year, slightly surpassing market expectations.

In light of these results, Macquarie has also updated its EBITDA projections for the years 2025 to 2027 to align with current trends and guidance. The adjustments reflect the company's solid performance and outlook.

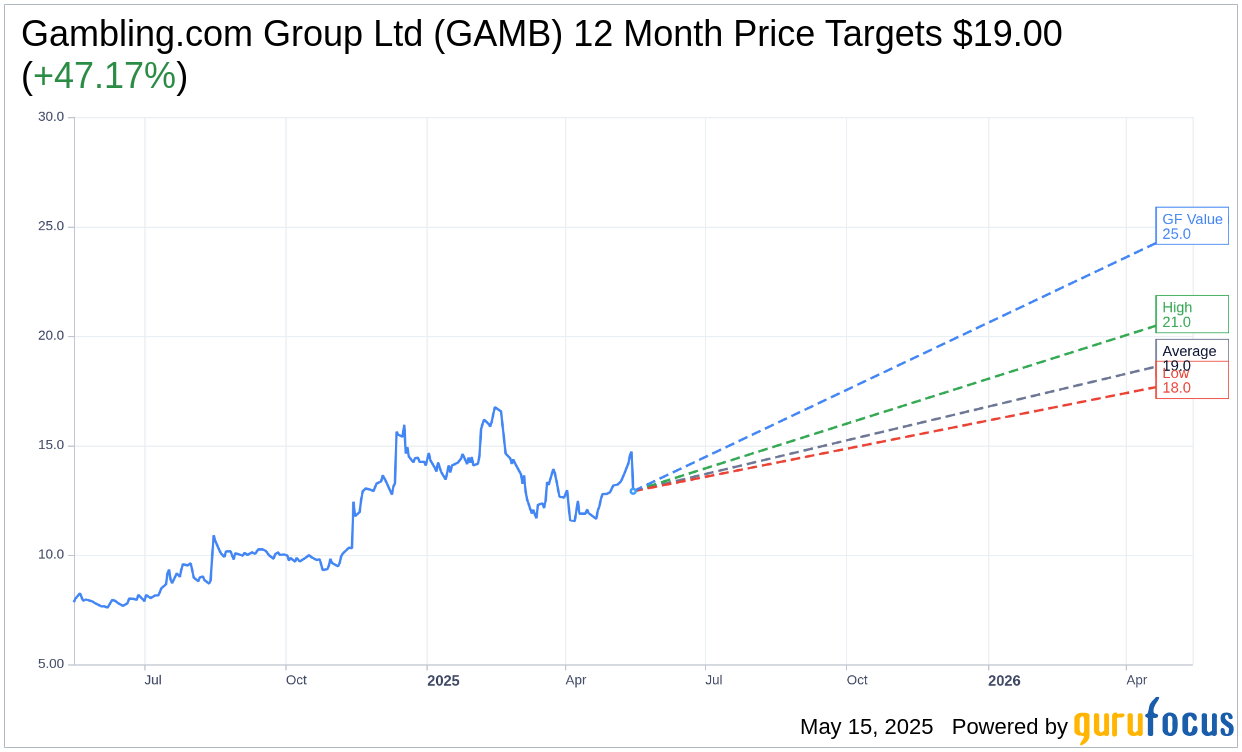

Wall Street Analysts Forecast

Based on the one-year price targets offered by 7 analysts, the average target price for Gambling.com Group Ltd (GAMB, Financial) is $19.00 with a high estimate of $21.00 and a low estimate of $18.00. The average target implies an upside of 47.17% from the current price of $12.91. More detailed estimate data can be found on the Gambling.com Group Ltd (GAMB) Forecast page.

Based on the consensus recommendation from 7 brokerage firms, Gambling.com Group Ltd's (GAMB, Financial) average brokerage recommendation is currently 1.6, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Gambling.com Group Ltd (GAMB, Financial) in one year is $25.04, suggesting a upside of 93.96% from the current price of $12.91. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Gambling.com Group Ltd (GAMB) Summary page.

GAMB Key Business Developments

Release Date: March 20, 2025

- Q4 Revenue: $35.3 million, a 9% year-over-year increase.

- Full-Year 2024 Revenue: $127.2 million, a 17% increase from 2023.

- Adjusted EBITDA (Q4): $14.7 million, a 39% increase year-over-year.

- Adjusted EBITDA Margin (Q4): 42%, up from 32% in the previous year.

- Full-Year 2024 Adjusted EBITDA: $48.7 million, a 33% increase from 2023.

- Free Cash Flow (Q4): $13.2 million, compared to $6.5 million in Q4 2023.

- Full-Year 2024 Free Cash Flow: $41.6 million, up from $23 million in 2023.

- Gross Margin (Q4): 94%, up from 84% in Q4 2023.

- Adjusted Net Income (Q4): $12.2 million, a 41% increase year-over-year.

- Adjusted Diluted Net Income Per Share (Q4): $0.35, up from $0.22 in Q4 2023.

- 2025 Revenue Guidance: $170 million to $174 million, representing 35% growth.

- 2025 Adjusted EBITDA Guidance: $67 million to $69 million, representing 40% growth.

- Total Cash (End of 2024): $13.7 million.

- Credit Facility Drawn: $87 million, with a facility expanded to $165 million.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Gambling.com Group Ltd (GAMB, Financial) reported record quarterly and full-year financial performance with Q4 2024 revenue of $35.3 million and adjusted EBITDA of $14.7 million.

- The company achieved a 17% increase in full-year 2024 revenue and a 33% rise in adjusted EBITDA, driven by global iGaming growth and the acquisition of Freebets.com.

- GAMB is positioned for significant growth in 2025, with expected full-year revenue growth of 35% and adjusted EBITDA growth of 40%.

- The acquisition of OddsJam and OpticOdds has expanded GAMB's product offerings and is expected to contribute to a 20% increase in recurring subscription revenue.

- The company has a strong focus on execution and diversified market exposure, with continued growth in iGaming revenue across all operating regions.

Negative Points

- The decline in North American sports revenue impacted overall growth, with a 9% year-over-year revenue increase in Q4 2024.

- The 9% decline in New Depositing Customers (NDCs) reflects the lack of new state launch activity compared to the previous year.

- Operating expenses increased by 21% due to higher headcounts and amortization expenses related to acquisitions.

- The company faces challenges in the Brazilian market due to regulatory changes and high taxes, impacting free cash flow generation.

- GAMB's guidance does not include contributions from new acquisitions or market launches, indicating potential uncertainties in achieving projected growth.