HSBC has revised its stance on Carnival (CCL, Financial), lifting its rating from Reduce to Hold and increasing the price target from $14 to $24. This adjustment comes as Carnival demonstrates robust booking trends, maintaining a strong reservation position even amid broader economic uncertainties. According to analysts, the company has shown noteworthy progress in profit recovery and debt reduction, supported by recent refinancing efforts.

HSBC's analysis indicates that Carnival has successfully addressed previous concerns, notably through effective cost-cutting measures and efforts to pursue higher return opportunities. These strategic initiatives have contributed to Carnival's improved financial outlook, prompting the upgraded assessment.

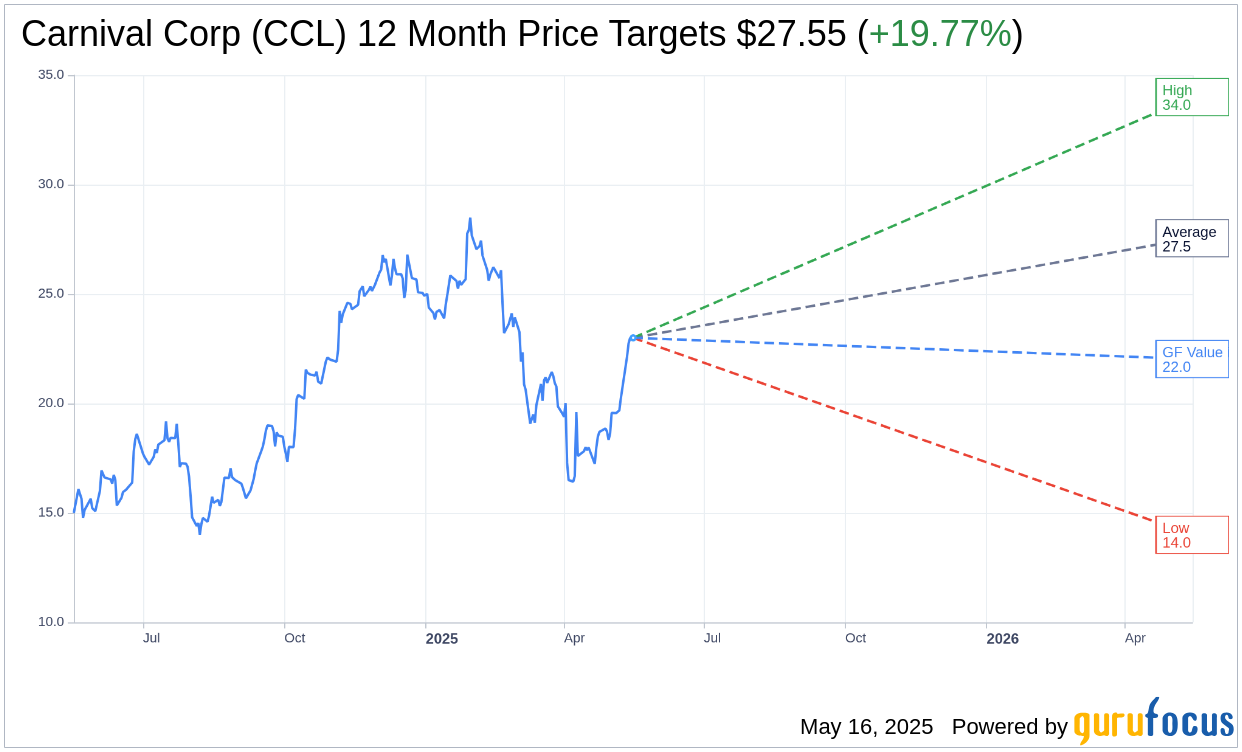

Wall Street Analysts Forecast

Based on the one-year price targets offered by 23 analysts, the average target price for Carnival Corp (CCL, Financial) is $27.55 with a high estimate of $34.00 and a low estimate of $14.00. The average target implies an upside of 19.77% from the current price of $23.00. More detailed estimate data can be found on the Carnival Corp (CCL) Forecast page.

Based on the consensus recommendation from 29 brokerage firms, Carnival Corp's (CCL, Financial) average brokerage recommendation is currently 2.0, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Carnival Corp (CCL, Financial) in one year is $22.03, suggesting a downside of 4.22% from the current price of $23. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Carnival Corp (CCL) Summary page.

CCL Key Business Developments

Release Date: March 21, 2025

- Revenue: First-quarter revenue reached a high-water mark, driven by strong demand.

- Net Income: Exceeded guidance by more than $170 million.

- EBITDA: Reached $1.2 billion, a nearly 40% year-over-year increase.

- Yield Increase: Achieved a 7.3% increase, surpassing guidance.

- Operating Income: Nearly doubled for the quarter.

- Operating and EBITDA Margins: Improved over 400 basis points year over year.

- Customer Deposits: Increased by over $300 million compared to the prior year.

- Interest Expense: Reduced by $13 million due to refinancing efforts.

- Debt Refinancing: $5.5 billion refinanced, reducing interest expense by $145 million annually.

- Total Debt: Reduced by $0.5 billion, ending the quarter at $27 billion.

- Cash Interest Rate: Average rate reduced to 4.6%.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Carnival Corp (CCL, Financial) achieved a robust 7.3% yield increase, surpassing yield guidance and building on last year's 17% improvement.

- The company reported a near doubling of operating income for the quarter, with EBITDA reaching $1.2 billion, marking a 40% year-over-year increase.

- Carnival Corp (CCL) has successfully increased its earnings guidance for the year by $185 million, driven by strong first-quarter results.

- The company is on track to meet its 2026 financial targets one year early, with ROIC expected to hit 12% and EBITDA per ALBD more than 50% higher than two years ago.

- Carnival Corp (CCL) has made significant progress in refinancing efforts, reducing interest expenses by $100 million for the year and lowering its average cash interest rate to 4.6%.

Negative Points

- Despite strong performance, Carnival Corp (CCL) acknowledges heightened macroeconomic and geopolitical volatility, which could impact future results.

- The company faces increased dry-dock costs due to unplanned dry docks, which have affected cruise costs without fuel per ALBD.

- Carnival Corp (CCL) has a significant amount of debt, ending the quarter with $27 billion in total debt, although efforts are being made to reduce this.

- The company has limited capacity growth, with only three ships on order over the next four years, which may constrain future revenue growth opportunities.

- Carnival Corp (CCL) is not immune to potential consumer demand fluctuations, as indicated by the cautious approach to maintaining yield guidance for the remainder of the year.