Iterum Therapeutics (ITRM, Financial) has secured an extension from Pfizer regarding the $20 million regulatory milestone payment, now due by October 25, 2029. Originally stipulated in their licensing agreement, this payment was tied to the successful U.S. Food and Drug Administration approval of oral sulopenem, branded as ORLYNVAH, for commercial sale in the United States.

The company initially opted to delay this payment by two years following the FDA approval on October 25, 2024, formalized through a promissory note issued by Iterum Therapeutics International Limited (ITIL) to Pfizer. By May 2025, both entities agreed to amend the promissory note, prolonging the Deferral Period by an additional three years.

In exchange for the extension, ITIL consented to a higher annual interest rate on the deferred amount, increasing from eight percent to ten percent, starting October 26, 2026. Furthermore, ITIL committed not to incur any senior debt above this agreement, except with Pfizer's consent, and also agreed to pay a transaction fee and cover Pfizer's legal expenses.

Wall Street Analysts Forecast

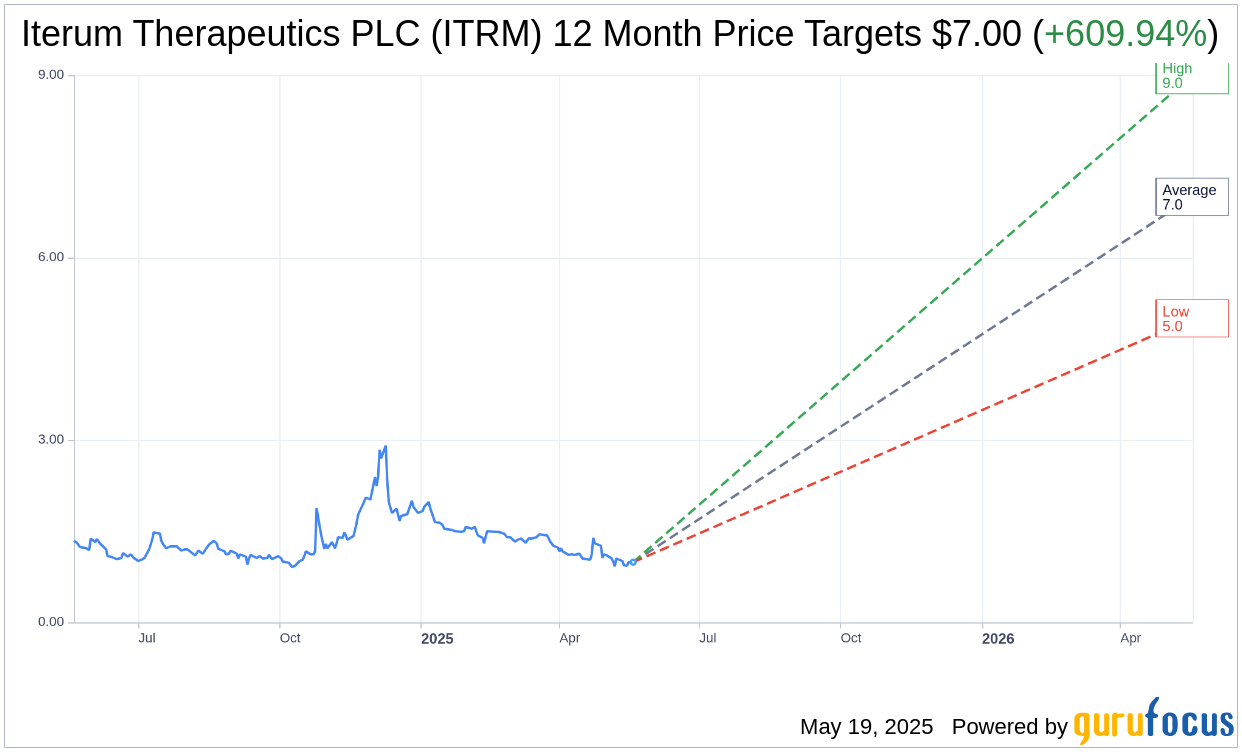

Based on the one-year price targets offered by 2 analysts, the average target price for Iterum Therapeutics PLC (ITRM, Financial) is $7.00 with a high estimate of $9.00 and a low estimate of $5.00. The average target implies an upside of 609.94% from the current price of $0.99. More detailed estimate data can be found on the Iterum Therapeutics PLC (ITRM) Forecast page.

Based on the consensus recommendation from 2 brokerage firms, Iterum Therapeutics PLC's (ITRM, Financial) average brokerage recommendation is currently 2.0, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

ITRM Key Business Developments

Release Date: May 13, 2025

- Total Operating Expenses: $3.7 million in Q1 2025, down from $6.2 million in Q1 2024.

- R&D Costs: $600,000 in Q1 2025, compared to $4 million in Q1 2024.

- G&A Costs: $2.8 million in Q1 2025, up from $2.2 million in Q1 2024.

- Net Loss (GAAP): $4.9 million in Q1 2025, compared to $7.1 million in Q1 2024.

- Net Loss (Non-GAAP): $3.3 million in Q1 2025, compared to $5.8 million in Q1 2024.

- Cash and Cash Equivalents: $12.7 million at the end of March 2025.

- Outstanding Shares: Approximately 40 million as of May 12, 2025.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Iterum Therapeutics PLC (ITRM, Financial) is preparing for the potential commercialization of ORLYNVAH, targeting a large U.S. market with approximately 40 million prescriptions annually for uncomplicated urinary tract infections.

- The company has extended its cash runway into 2026, providing financial stability for upcoming operations and potential product launch.

- Iterum Therapeutics PLC (ITRM) has significantly reduced its operating expenses, with a decrease from $6.2 million in Q1 2024 to $3.7 million in Q1 2025.

- The company has repaid the outstanding principal and interest on its exchangeable notes, eliminating a large amount of debt.

- Iterum Therapeutics PLC (ITRM) has partnered with Everson, an end-to-end commercialization firm, to prepare for the potential launch of ORLYNVAH, indicating a strategic approach to market entry.

Negative Points

- Iterum Therapeutics PLC (ITRM) has not yet secured a business development transaction that the Board finds acceptable, indicating challenges in finding suitable partners.

- The company faces competition from new products approved in the uncomplicated urinary tract infection space, increasing urgency for ORLYNVAH's market entry.

- Iterum Therapeutics PLC (ITRM) reported a net loss of $4.9 million for Q1 2025, although reduced from the previous year, it still indicates financial challenges.

- The increase in general and administrative expenses due to pre-commercialization activities suggests higher operational costs.

- The company's ability to expand its commercialization efforts is contingent on successfully raising additional capital, indicating potential financial constraints.