Honeywell (HON, Financial) has revealed plans to purchase the Catalyst Technologies division from Johnson Matthey for a total of GBP 1.8 billion. This acquisition will be executed through an all-cash transaction, which equates to roughly 11 times the projected EBITDA for 2025, including tax advantages and cost efficiencies at full capacity.

The deal is anticipated to be finalized by the first half of 2026, contingent upon standard closing conditions and necessary regulatory approvals. This strategic move aligns with Honeywell's growth objectives and positions it to enhance its offerings in the catalyst market.

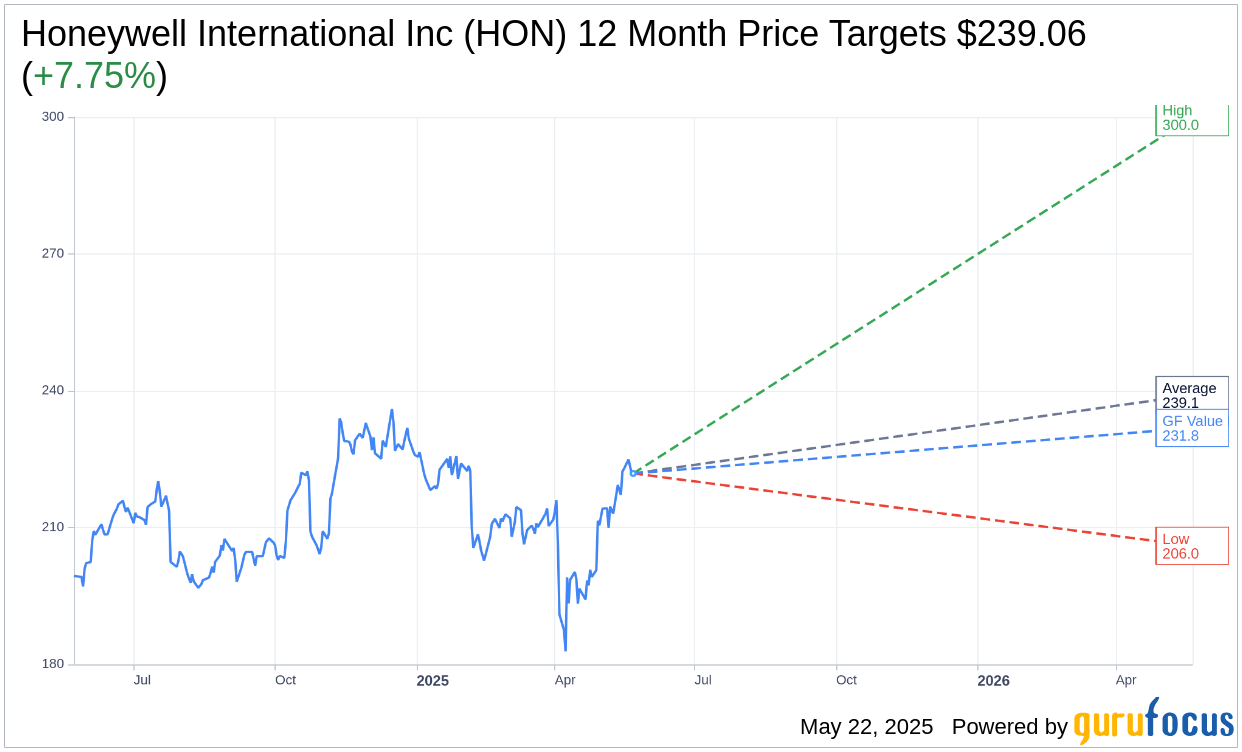

Wall Street Analysts Forecast

Based on the one-year price targets offered by 21 analysts, the average target price for Honeywell International Inc (HON, Financial) is $239.06 with a high estimate of $300.00 and a low estimate of $206.00. The average target implies an upside of 7.75% from the current price of $221.87. More detailed estimate data can be found on the Honeywell International Inc (HON) Forecast page.

Based on the consensus recommendation from 27 brokerage firms, Honeywell International Inc's (HON, Financial) average brokerage recommendation is currently 2.3, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Honeywell International Inc (HON, Financial) in one year is $231.85, suggesting a upside of 4.5% from the current price of $221.87. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Honeywell International Inc (HON) Summary page.

HON Key Business Developments

Release Date: April 29, 2025

- Organic Sales Growth: 4% in Q1, led by Aerospace Technologies.

- Segment Margin: Flat at 23% from the prior year.

- Adjusted Earnings Per Share (EPS): $2.51, up 7% year over year.

- Orders: $10.6 billion, up 3% year over year.

- Free Cash Flow: Over $300 million, $100 million above the prior year.

- Share Repurchase: Nearly $2 billion in Q1, with an additional $1 billion in April.

- Dividends Paid: Over $700 million in Q1.

- Aerospace Technologies Sales Growth: 9% organically year over year.

- Building Automation Sales Growth: 8% organically, with margin expansion of 150 basis points.

- Energy and Sustainability Solutions Margin Expansion: 230 basis points in Q1.

- Full-Year Organic Sales Growth Guidance: 2% to 5%.

- Full-Year EPS Guidance: $10.20 to $10.50, up 3% to 6%.

- Full-Year Free Cash Flow Guidance: $5.4 billion to $5.8 billion.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Honeywell International Inc (HON, Financial) exceeded the high end of its guidance on all metrics in the first quarter of 2025, demonstrating strong performance and substantial free cash flow growth.

- The company maintained its full-year organic growth guidance and raised its adjusted EPS guidance, showing confidence in its ability to navigate economic uncertainties.

- Honeywell International Inc (HON) is actively managing tariff impacts through a local-for-local strategy and pricing adjustments, aiming to offset $500 million in tariff exposure.

- The company is progressing well with its plan to separate into three standalone public companies, which is expected to unlock significant value for stakeholders.

- Honeywell International Inc (HON) has a strong acquisition strategy, with the recent acquisition of Sundyne expected to enhance its business profile and boost organic growth and segment margins.

Negative Points

- The economic climate has become increasingly uncertain, with shifting global trade patterns and higher price expectations posing challenges to customer planning.

- Industrial Automation sales declined 2% organically in the first quarter, with lower demand in personal protective equipment, particularly in China and Europe.

- Segment margin in Aerospace Technologies contracted by 190 basis points due to mix pressure and acquisition integration costs.

- The company anticipates potential end-market demand weakness triggered by geopolitical uncertainties, impacting organic sales and segment profit.

- Honeywell International Inc (HON) is facing challenges in its Industrial Automation segment, with exposure to China trade and potential demand destruction in short-cycle businesses.