In its recent financial update, (S, Financial) has reported an impressive second-quarter adjusted gross margin of 79%. This figure highlights the company's robust performance and operational efficiency during the period. Such a high margin suggests effective cost management and strong revenue generation, positioning (S) advantageously in the market. This financial health may attract investors looking for stable and resilient stock options.

Wall Street Analysts Forecast

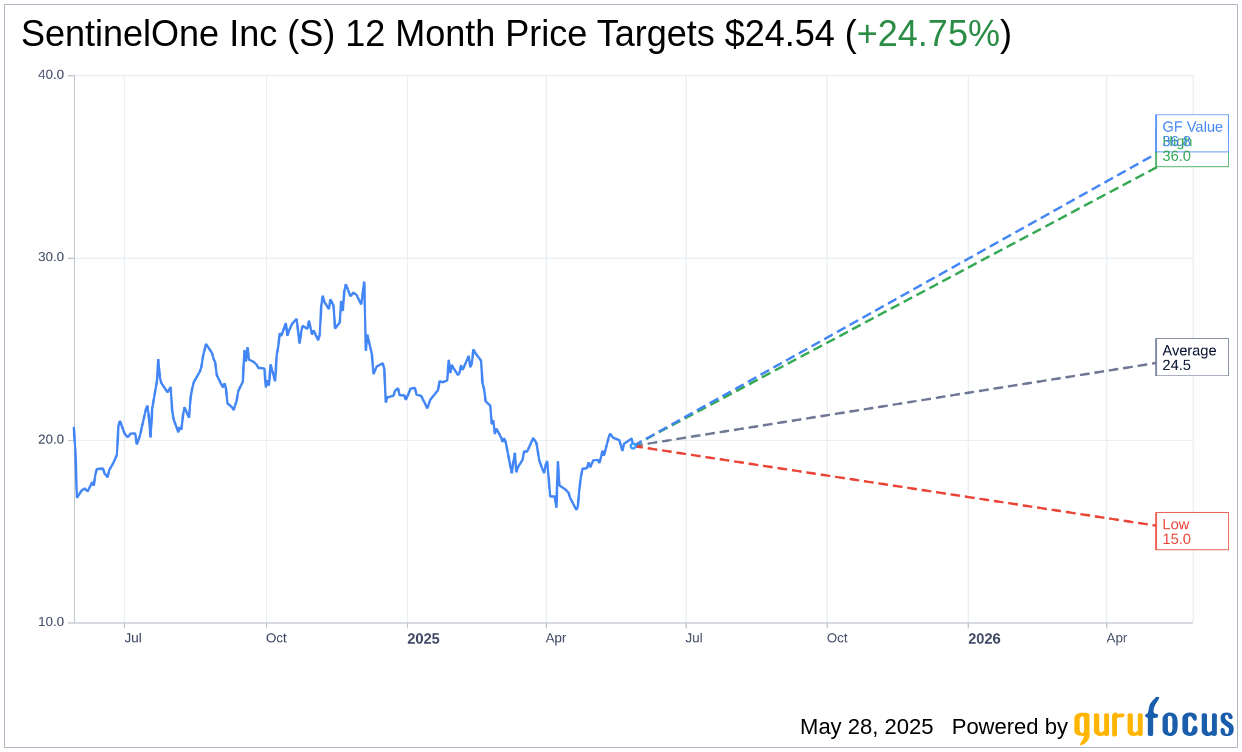

Based on the one-year price targets offered by 34 analysts, the average target price for SentinelOne Inc (S, Financial) is $24.54 with a high estimate of $36.00 and a low estimate of $15.00. The average target implies an upside of 24.75% from the current price of $19.67. More detailed estimate data can be found on the SentinelOne Inc (S) Forecast page.

Based on the consensus recommendation from 38 brokerage firms, SentinelOne Inc's (S, Financial) average brokerage recommendation is currently 1.9, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for SentinelOne Inc (S, Financial) in one year is $36.81, suggesting a upside of 87.14% from the current price of $19.67. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the SentinelOne Inc (S) Summary page.

S Key Business Developments

Release Date: March 12, 2025

- Revenue: $821 million for fiscal year '25, a growth of 32% year over year.

- Q4 Revenue: $226 million, a 29% increase year over year.

- Gross Margin: Reached a new full year high, with Q1 expected to be about 79%.

- Operating Margin: Improved by 16 percentage points year over year; first quarter of positive operating margin in Q4.

- Net Income Margin: Positive 2% for the full year.

- Free Cash Flow Margin: Positive 1% for the full year.

- Total ARR: Grew 27% to $920 million.

- Net New ARR: $60 million in Q4.

- RPO Growth: Re-accelerated to 30%, reaching a record of $1.2 billion.

- Customer Growth: Over 14,000 direct customers; customers with ARR of $100,000 or more grew 25% year over year.

- Dollar-Based Net Retention Rate: 110% for the full year.

- Fiscal Year '26 Revenue Guidance: Expected to surpass $1 billion, representing 23% growth.

- Fiscal Year '26 Net New ARR Guidance: Approximately $200 million, growing about 2% year over year.

- Cash and Cash Equivalents: Over $1.1 billion.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- SentinelOne Inc (S, Financial) achieved over 30% top line growth while expanding operating margins by over 15 percentage points.

- The company reported its first quarter of positive operating income in Q4, alongside its first full year of positive net income and free cash flow.

- SentinelOne Inc (S) surpassed expectations in Q4, with revenue growing 29% year over year to $226 million.

- The company set a new customer growth record, with over 14,000 direct customers and significant expansion in platform solutions.

- SentinelOne Inc (S) is the first company to embed foundational generative AI capabilities into every platform solution by default, enhancing its competitive edge in AI-powered cybersecurity.

Negative Points

- The company faces macroeconomic challenges, including economic and political uncertainty impacting budgets and business decisions.

- SentinelOne Inc (S) is retiring its legacy Deception solution, which is expected to result in up to $10 million of churn, impacting ARR growth.

- The guidance for fiscal year '26 includes a deceleration in revenue growth to 23%, compared to previous years.

- There is uncertainty regarding federal spending, which could affect the company's growth in the government sector.

- Despite strong performance, the company's guidance for Q1 and fiscal year '26 was slightly below analyst expectations, raising concerns about future growth momentum.