Morgan Stanley has adjusted its price target for Abercrombie & Fitch (ANF, Financial), raising it from $78 to $82 while maintaining an Equal Weight rating on the stock. The decision followed a first-quarter earnings report where sales exceeded expectations, although the fiscal year guidance was lowered less than anticipated. Despite this positive outlook, the report revealed some ongoing challenges, including a slowdown in the A&F banner and a miss on the gross margin.

According to the firm, while the first-quarter results may heighten concerns about potential declines in sales and profitability, leading to possible downward revisions in earnings per share, these risks seem to be mostly factored into the current stock price.

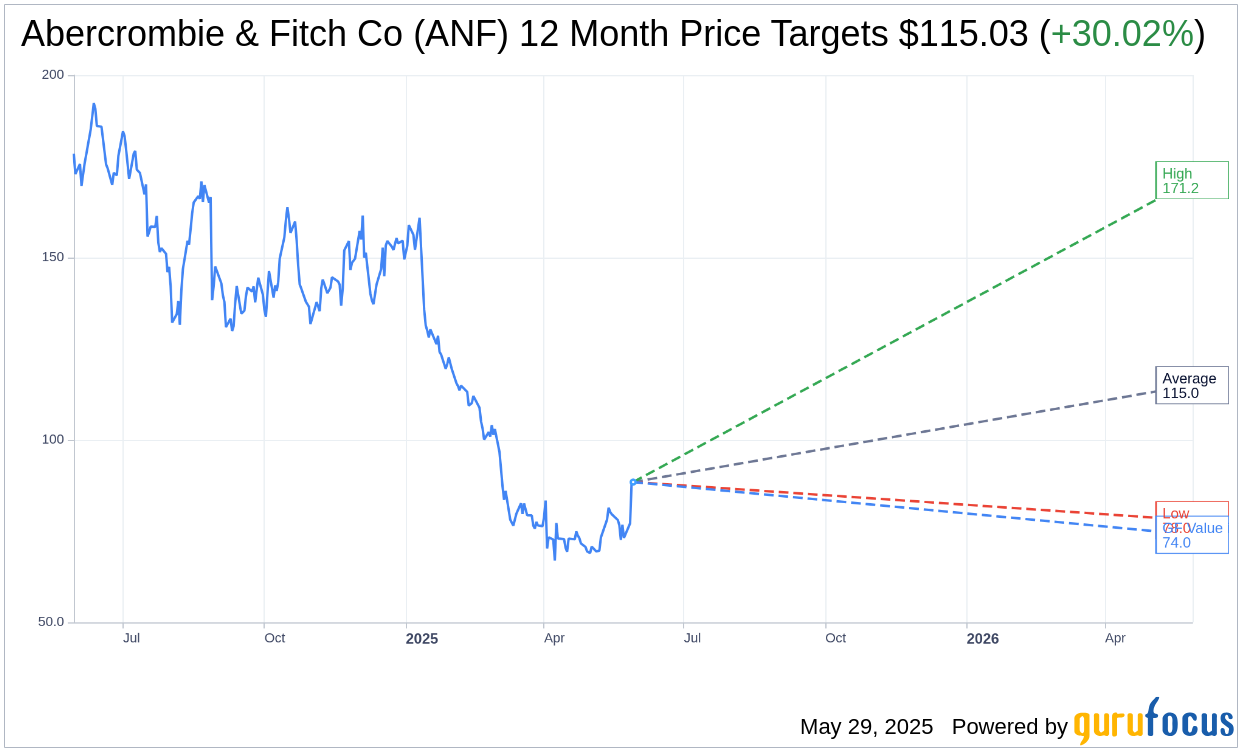

Wall Street Analysts Forecast

Based on the one-year price targets offered by 8 analysts, the average target price for Abercrombie & Fitch Co (ANF, Financial) is $115.03 with a high estimate of $171.20 and a low estimate of $78.00. The average target implies an upside of 30.02% from the current price of $88.47. More detailed estimate data can be found on the Abercrombie & Fitch Co (ANF) Forecast page.

Based on the consensus recommendation from 12 brokerage firms, Abercrombie & Fitch Co's (ANF, Financial) average brokerage recommendation is currently 2.1, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Abercrombie & Fitch Co (ANF, Financial) in one year is $74.03, suggesting a downside of 16.32% from the current price of $88.47. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Abercrombie & Fitch Co (ANF) Summary page.

ANF Key Business Developments

Release Date: May 28, 2025

- Net Sales: $1.1 billion, up 8% year-over-year.

- Operating Margin: 9.3%.

- Earnings Per Share (EPS): $1.59.

- Share Repurchases: $200 million, totaling 5% of shares outstanding.

- Americas Sales Growth: 7%.

- EMEA Sales Growth: 12%.

- APAC Sales Growth: 5%.

- Hollister Net Sales Growth: 22%.

- Abercrombie Brands Net Sales Decline: 4%.

- Inventory Increase: 21% at cost.

- Cash and Cash Equivalents: $511 million.

- Marketable Securities: $97 million.

- Full Year Net Sales Growth Outlook: 3% to 6%.

- Full Year Operating Margin Outlook: 12.5% to 13.5%.

- Full Year EPS Outlook: $9.50 to $10.50.

- Capital Expenditures: Approximately $200 million.

- New Store Openings: Around 100 new experiences, including 60 new stores.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Abercrombie & Fitch Co (ANF, Financial) reported record net sales of $1.1 billion for the first quarter, an 8% increase from the previous year, surpassing their expected growth range of 4% to 6%.

- The company achieved an operating margin of 9.3% and earnings per share of $1.59, both above the ranges provided in March.

- Hollister brand delivered record first-quarter results with 22% net sales growth, marking its 8th consecutive quarter of growth.

- Net sales growth was observed across all regions, with the Americas growing by 7%, EMEA by 12%, and APAC by 5%.

- Abercrombie & Fitch Co (ANF) returned $200 million to shareholders through share repurchases, totaling 5% of shares outstanding at the beginning of the year.

Negative Points

- Abercrombie brands experienced a 4% net sales decline, with comparable sales down 10%, primarily due to lower AUR as they cleared seasonal carryover inventory.

- The company faced a reduction in full-year operating margin outlook due to an estimated 100 basis point impact from tariffs.

- Gross margin was negatively impacted by freight and carryover pressures, contributing to a 440 basis point decline in Q1.

- Abercrombie & Fitch Co (ANF) anticipates a $50 million cost impact from tariffs for 2025, affecting their full-year operating margin outlook.

- The company is experiencing pressure on AUR, particularly in the Abercrombie brand, due to carryover inventory and competitive market conditions.