Agilent Technologies (A, Financial) experienced stock pressure prior to its earnings announcement, influenced primarily by challenges within the life science tools segment. According to analyst Vijay Kumar from Evercore ISI, the company's performance in the second quarter was stable, leading to the reaffirmation of its guidance.

Following the earnings report, the outlook for Agilent reveals varied signals. Despite this, certain strengths were highlighted. As part of a strategic decision, Agilent has been removed from Evercore ISI's "Tactical Outperform" list. The firm maintains an "In Line" rating on the stock, setting a price target of $125 for Agilent.

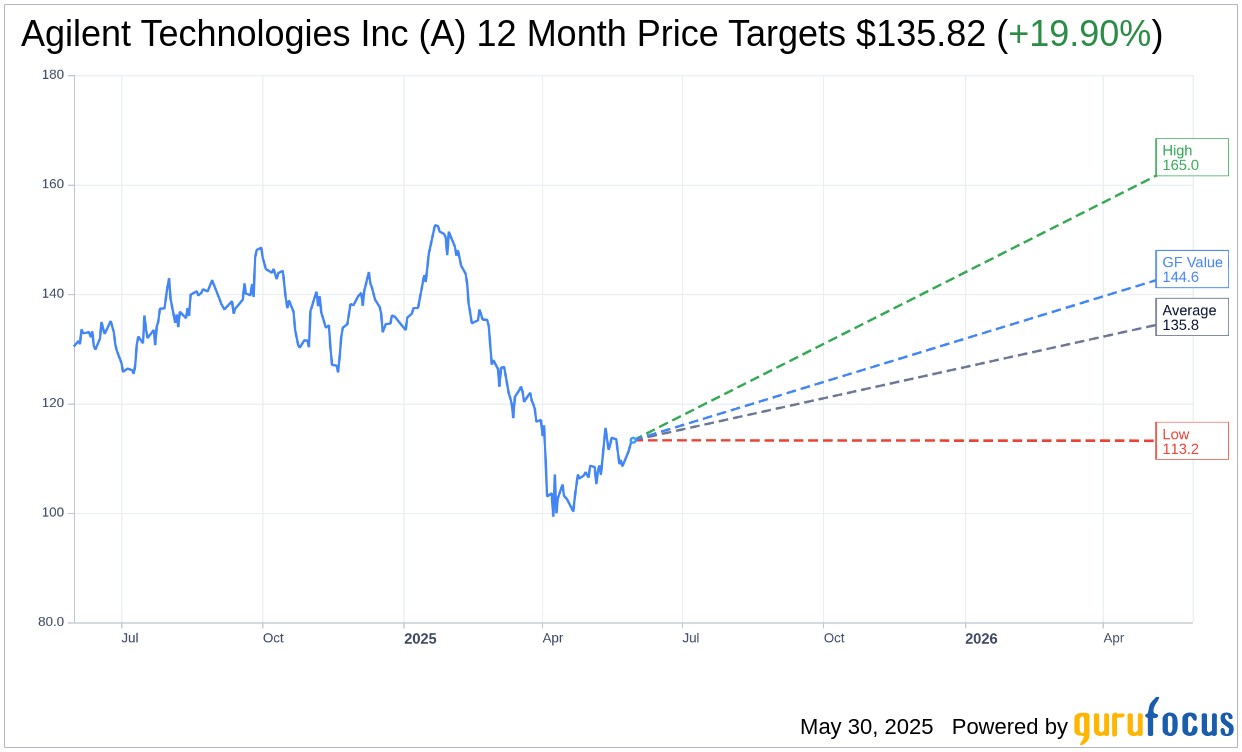

Wall Street Analysts Forecast

Based on the one-year price targets offered by 16 analysts, the average target price for Agilent Technologies Inc (A, Financial) is $135.83 with a high estimate of $165.00 and a low estimate of $113.20. The average target implies an upside of 19.90% from the current price of $113.28. More detailed estimate data can be found on the Agilent Technologies Inc (A) Forecast page.

Based on the consensus recommendation from 21 brokerage firms, Agilent Technologies Inc's (A, Financial) average brokerage recommendation is currently 2.3, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Agilent Technologies Inc (A, Financial) in one year is $144.57, suggesting a upside of 27.62% from the current price of $113.28. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Agilent Technologies Inc (A) Summary page.

A Key Business Developments

Release Date: May 28, 2025

- Revenue: $1.67 billion, representing 6% reported growth and 5.3% core growth year-over-year.

- Operating Margin: 25.1%, absorbing incremental tariff costs.

- Earnings Per Share (EPS): $1.31, a 7% increase compared to the second quarter of 2024.

- Gross Margin: 54.1%, impacted by tariffs, currency, and product mix.

- Agilent CrossLab Group Revenue: $713 million, 9% growth driven by consumables and automation.

- Life Sciences and Diagnostics Market Group Revenue: $654 million, 3% growth with strong performance in Pathology and NASD.

- Applied Markets Group Revenue: $301 million, flat on a core growth basis.

- Cash Flow from Operations: $221 million.

- Capital Expenditures: $114 million.

- Share Repurchases: $165 million.

- Dividends Paid: $70 million.

- Net Leverage Ratio: 1.

- Full Year Revenue Guidance: Increased to $6.73 billion to $6.81 billion, reflecting a 3.4% to 4.6% reported growth.

- Full Year EPS Guidance: $5.54 to $5.61, representing a 4.7% to 6% increase year-over-year.

- Tariff Impact: $50 million gross incremental exposure in the second half of fiscal year 2025, with mitigation strategies in place.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Agilent Technologies Inc (A, Financial) reported strong second-quarter results with revenue of $1.67 billion, representing a 6% increase year-over-year.

- The company achieved an operating margin of 25.1% despite absorbing incremental tariff costs.

- Agilent's EPS grew by 7% compared to the second quarter of 2024, marking the fourth consecutive quarter of accelerating growth.

- The company saw growth across all regions, with China leading at 10% growth, and strong performance in India with high teens growth.

- Agilent's PFAS testing business grew more than 70% year-over-year globally, contributing significantly to the company's growth.

Negative Points

- The academia and government end market declined modestly, with a 2% decrease in the quarter.

- Biopharma growth was slower, with low single-digit growth due to funding challenges in small and midsized biotech, primarily in the US.

- The company faced a mid-single-digit decline in its NGS business.

- Agilent had to absorb 55 basis points of incremental tariff costs, impacting gross margins.

- The company anticipates potential additional tariff impacts if US-EU tariffs increase, which could add $40 million in gross exposure in the second half of the year.