The U.S. Commerce Department, led by Jeffrey Kessler, is considering revoking waivers that currently permit certain companies to utilize American technology in China without additional licensing. This move could significantly influence semiconductor firms, including AMD (AMD, Financial), since many in the industry benefit from these waivers to supply chip-making equipment to their Chinese manufacturing plants.

This initiative is part of an effort to restrict the flow of critical U.S. technology to foreign entities. The decision underscores a broader strategy to reassess and possibly tighten export controls under the current administration's technological policies.

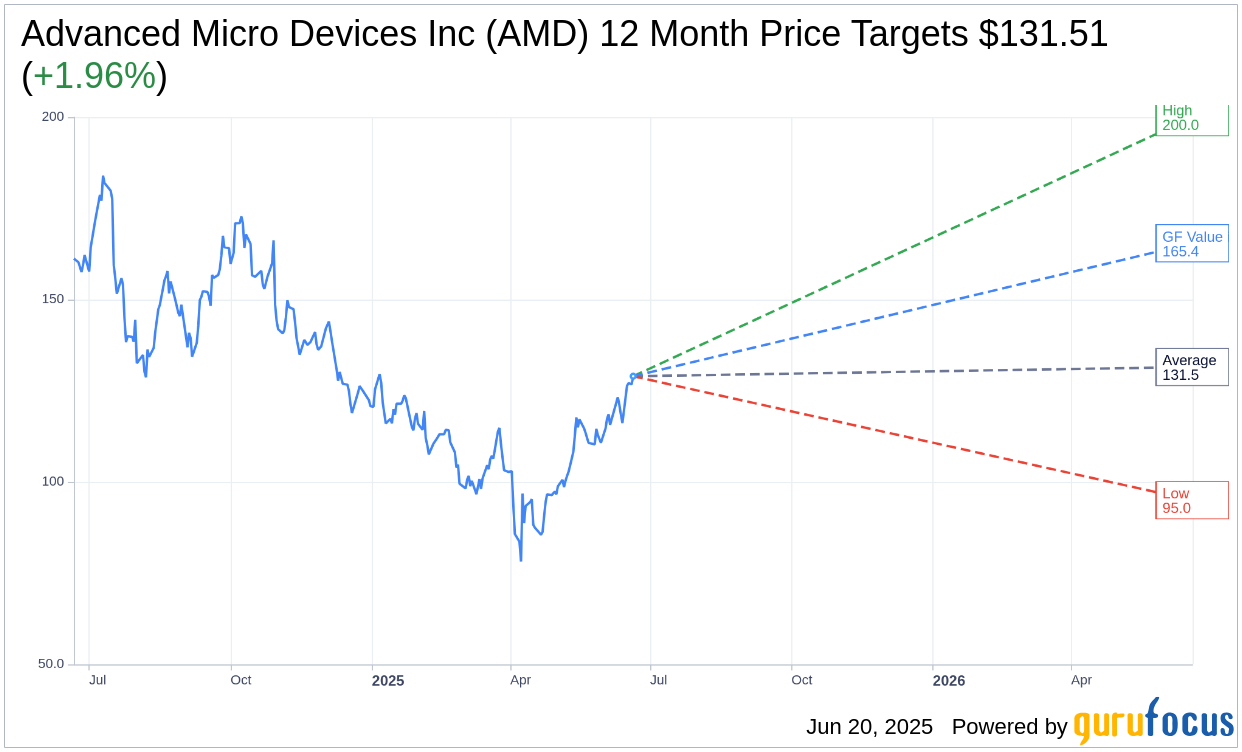

Wall Street Analysts Forecast

Based on the one-year price targets offered by 40 analysts, the average target price for Advanced Micro Devices Inc (AMD, Financial) is $131.51 with a high estimate of $200.00 and a low estimate of $95.00. The average target implies an upside of 1.96% from the current price of $128.98. More detailed estimate data can be found on the Advanced Micro Devices Inc (AMD) Forecast page.

Based on the consensus recommendation from 52 brokerage firms, Advanced Micro Devices Inc's (AMD, Financial) average brokerage recommendation is currently 2.1, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Advanced Micro Devices Inc (AMD, Financial) in one year is $165.43, suggesting a upside of 28.26% from the current price of $128.98. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Advanced Micro Devices Inc (AMD) Summary page.

AMD Key Business Developments

Release Date: May 06, 2025

- Revenue: $7.4 billion, up 36% year over year.

- Gross Margin: 54%, up 140 basis points from a year ago.

- Net Income: Increased by 55% year over year.

- Operating Income: $1.8 billion, representing a 24% operating margin.

- Diluted EPS: $0.96, an increase of 55% year over year.

- Data Center Revenue: $3.7 billion, up 57% year over year.

- Client and Gaming Revenue: $2.9 billion, up 28% year over year.

- Embedded Revenue: $823 million, down 3% year over year.

- Cash from Operations: $939 million.

- Free Cash Flow: $727 million.

- Share Repurchase: $749 million returned to shareholders.

- Cash and Equivalents: $7.3 billion at the end of the quarter.

- Second Quarter Revenue Outlook: Approximately $7.4 billion, plus or minus $300 million.

- Second Quarter Gross Margin Outlook: Estimated to be 43%, inclusive of charges.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Advanced Micro Devices Inc (AMD, Financial) reported a 36% year-over-year increase in first-quarter revenue, reaching $7.4 billion, driven by strong growth in data center and client segments.

- The company achieved a 55% increase in net income, supported by a higher percentage of data center product sales and a richer Ryzen processor mix.

- Data center segment revenue grew by 57% year over year, with significant contributions from EPYC CPU and Instinct AI accelerator sales.

- AMD's client revenue increased by 68% year over year, marking the fifth consecutive quarter of revenue share gains, driven by high-end Ryzen processors.

- The company expanded its gross margin for the fifth straight quarter, reaching 54%, up 140 basis points from the previous year.

Negative Points

- Gaming revenue decreased by 30% year over year, primarily due to lower semi-custom sales despite higher Radeon Graphics sales.

- Embedded segment revenue declined by 3% year over year, with a gradual recovery expected in the second half of 2025.

- The new export license requirement for MI308 shipments to China is expected to result in a $1.5 billion revenue reduction for the full year 2025.

- AMD's second-quarter guidance includes an estimated $700 million revenue reduction due to the new export license requirement, impacting data center segment revenue.

- Operating expenses increased by 28% year over year, as AMD continues to invest in go-to-market activities and R&D.