A virtual meeting is scheduled for June 26, where B. Riley will host discussions involving HCC. This event promises to offer insights into the company's performance and strategic direction. Investors and stakeholders will have the opportunity to engage with key information that could influence investment decisions. The meeting aims to provide a comprehensive overview of HCC's recent activities and future outlook, highlighting aspects that may appeal to those seeking resilient investment opportunities.

Wall Street Analysts Forecast

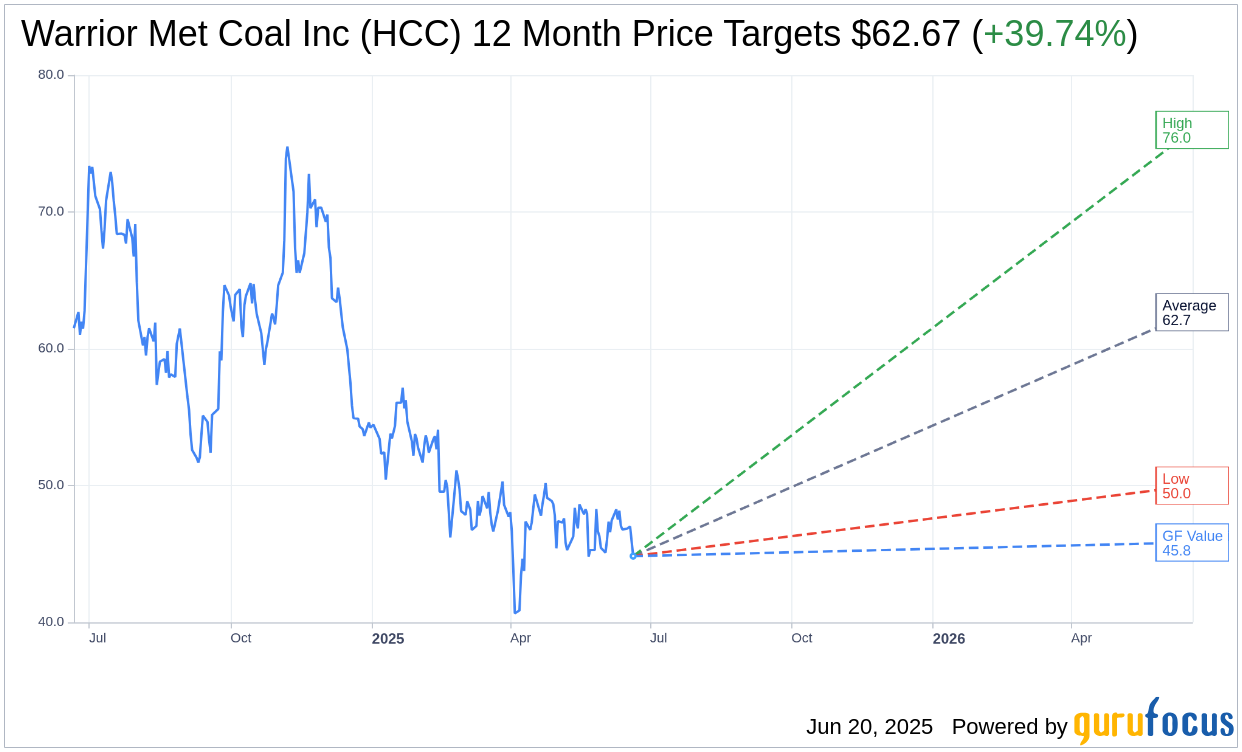

Based on the one-year price targets offered by 6 analysts, the average target price for Warrior Met Coal Inc (HCC, Financial) is $62.67 with a high estimate of $76.00 and a low estimate of $50.00. The average target implies an upside of 39.74% from the current price of $44.85. More detailed estimate data can be found on the Warrior Met Coal Inc (HCC) Forecast page.

Based on the consensus recommendation from 6 brokerage firms, Warrior Met Coal Inc's (HCC, Financial) average brokerage recommendation is currently 2.2, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Warrior Met Coal Inc (HCC, Financial) in one year is $45.84, suggesting a upside of 2.22% from the current price of $44.845. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Warrior Met Coal Inc (HCC) Summary page.

HCC Key Business Developments

Release Date: April 30, 2025

- Net Loss: $8 million or $0.16 per diluted share for Q1 2025.

- Revenue: $300 million in Q1 2025, down from $504 million in Q1 2024.

- Adjusted EBITDA: $40 million in Q1 2025, compared to $200 million in Q1 2024.

- Adjusted EBITDA Margin: 13% in Q1 2025, down from 40% in Q1 2024.

- Sales Volume: 2.2 million short tons in Q1 2025, a 2% increase from Q1 2024.

- Production Volume: 2.3 million short tons in Q1 2025, a 10% increase from Q1 2024.

- Average Net Selling Price: $136 per short ton in Q1 2025, down from $234 per short ton in Q1 2024.

- Cash Cost of Sales: $244 million or 83% of mining revenues in Q1 2025.

- Free Cash Flow: Negative $68 million in Q1 2025.

- Total Available Liquidity: $617 million at the end of Q1 2025.

- Capital Expenditures and Mine Development: $79 million in Q1 2025.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Warrior Met Coal Inc (HCC, Financial) achieved a 2% increase in sales volume, reaching 2.2 million short tons in the first quarter of 2025 compared to the same period last year.

- The company reported a 10% increase in production volume, driven by strong performance from existing mines and contributions from the Blue Creek mine.

- Warrior Met Coal Inc (HCC) maintained tight cost discipline, achieving a cash cost of sales per short ton FOB port of $112, down from $133 in the first quarter of 2024.

- The Blue Creek project remains on budget and on schedule, with significant progress in infrastructure development and early milestones achieved ahead of schedule.

- The company has sufficient liquidity, with $617 million in available liquidity, to complete the Blue Creek project without slowing down or suspending operations.

Negative Points

- Warrior Met Coal Inc (HCC) reported a net loss of $8 million for the first quarter of 2025, compared to a net income of $137 million in the same quarter of 2024.

- The company experienced a 42% decrease in realized average net selling prices, significantly impacting financial results.

- Adjusted EBITDA margin dropped to 13% in the first quarter of 2025 from 40% in the same period last year.

- Global steel market challenges, including China's overcapacity and trade policy uncertainties, continue to pressure steelmaking coal prices.

- The company faces potential impacts from retaliatory tariffs on US steelmaking coals, which have halted coal trade between the US and China.