PayPal (PYPL, Financial) Holdings has entered into long-term collaborations with the Big Ten and Big 12 Conferences to implement a new payment distribution framework for university athletic departments. This initiative allows for a smooth transfer of institutional payments to student-athletes, leveraging PayPal's secure and transparent platform. As a result, funds are easily accessible, enabling students to utilize PayPal’s extensive commerce network for transactions such as purchasing event tickets or books from campus stores.

This development follows a recent legal ruling permitting academic institutions to directly share revenue with student-athletes, marking a transformative shift in collegiate athletics. The partnership between PayPal and these conferences aims to actualize this change by ensuring funds reach athletes promptly and securely.

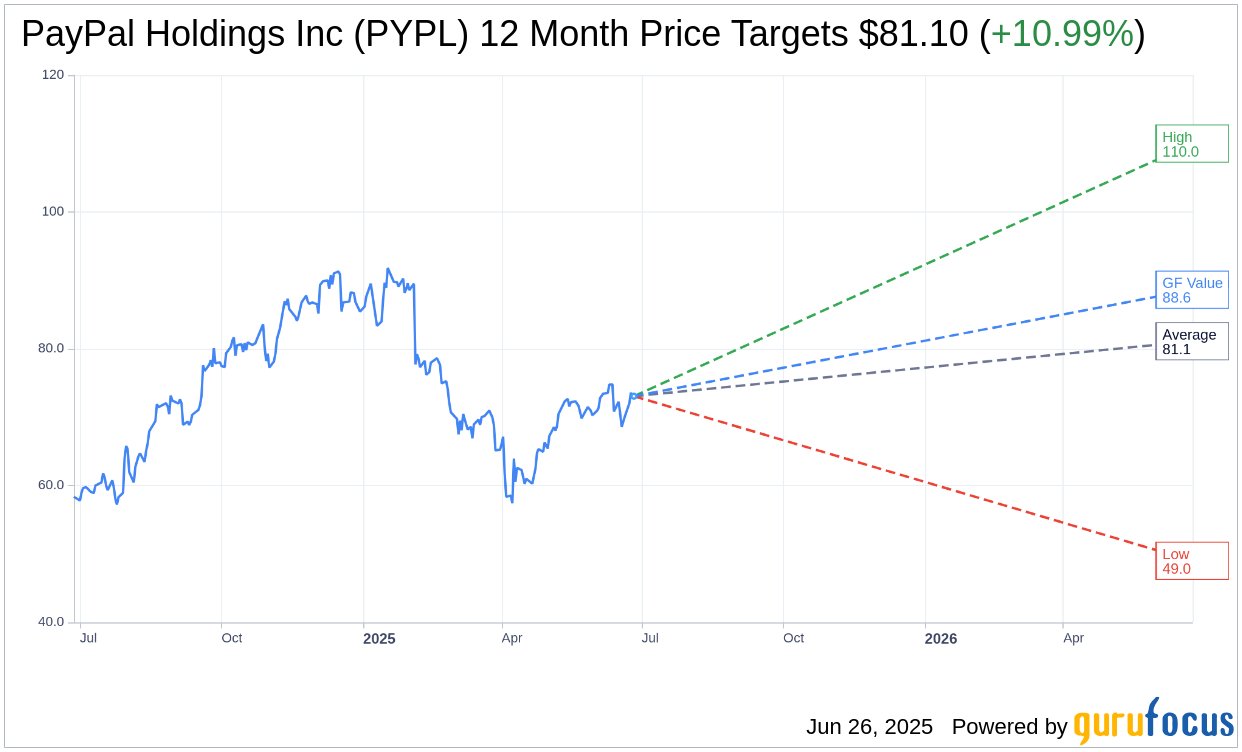

Wall Street Analysts Forecast

Based on the one-year price targets offered by 37 analysts, the average target price for PayPal Holdings Inc (PYPL, Financial) is $81.10 with a high estimate of $110.00 and a low estimate of $49.00. The average target implies an upside of 10.99% from the current price of $73.07. More detailed estimate data can be found on the PayPal Holdings Inc (PYPL) Forecast page.

Based on the consensus recommendation from 46 brokerage firms, PayPal Holdings Inc's (PYPL, Financial) average brokerage recommendation is currently 2.4, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for PayPal Holdings Inc (PYPL, Financial) in one year is $88.63, suggesting a upside of 21.29% from the current price of $73.07. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the PayPal Holdings Inc (PYPL) Summary page.

PYPL Key Business Developments

Release Date: April 29, 2025

- Transaction Margin Growth: 8% growth excluding last year's leap day.

- Non-GAAP Earnings Per Share: Increased 23% year-over-year.

- Total Active Accounts: Grew by 2% in the quarter.

- Branded Experiences TPV: Grew 8% excluding last year's leap day.

- Venmo Revenue Growth: 20% increase driven by online and in-store payments.

- Free Cash Flow: $1 billion generated in the first quarter.

- Non-GAAP Operating Margin: Increased to 20.7%, up 260 basis points.

- Share Repurchases: $1.5 billion completed in the quarter.

- Cash and Investments: Ended the quarter with $15.8 billion.

- Debt: $12.6 billion in debt at the end of the quarter.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- PayPal Holdings Inc (PYPL, Financial) delivered its fifth consecutive quarter of profitable growth, with transaction margin dollars growing by 8%, excluding the impact from last year's leap day.

- Non-GAAP earnings per share increased 23% year-over-year, reflecting strong profitability.

- Branded experiences TPV grew 8% in Q1, highlighting the success of omnichannel initiatives and increased consumer engagement.

- Venmo achieved 20% revenue growth, driven by increased merchant availability and consumer adoption.

- PayPal Holdings Inc (PYPL) is expanding its offerings with innovations like a dynamic smart wallet and agentic commerce, positioning itself as a strategic commerce partner for merchants.

Negative Points

- Despite a strong start to the year, PayPal Holdings Inc (PYPL) is maintaining its full-year guidance due to macroeconomic uncertainties.

- Transaction take rate declined by 6 basis points to 1.68%, influenced by product and merchant mix.

- The PSP volume growth slowed to 2% compared to 6% in the previous quarter, as the company prioritizes profitable growth over volume.

- There is potential impact from geopolitical factors, such as tariffs, which could affect global economic activity and consumer spending.

- The competitive landscape in key markets like the UK remains challenging, requiring continued investment in product improvements and marketing.