Business Overview

Resideo Technologies (NYSE: REZI) is a global manufacturer and distributor of home comfort, security, and automation products. It was spun off from Honeywell in 2018, inheriting Honeywell's Home and ADI Global Distribution businesses. Resideo's Products & Solutions segment supplies thermostats (under the Honeywell Home brand), smoke/carbon detectors (First Alert/BRK), security sensors, water leak detectors, and related services. Its ADI Global Distribution segment is a leading wholesale distributor of security and low‑voltage products to professional installers. In mid‑2024, Resideo acquired Snap One (Control4, Triad, etc.) for ~$1.4 billion, adding smart living solutions to its portfolio and expanding the ADI distribution offerings.

Resideo Technologies First Quarter FY2025 Earnings Analysis

Resideo reported strong Q1 2025 results, surpassing consensus estimates and management's guidance on both revenue and earnings. Total revenue came in at $1.77 billion, up approximately 19% year-over-year and above the expected $1.72 billion, driven by the Snap One acquisition and increased demand for new products such as HVAC thermostats and alarms. Adjusted EBITDA rose 23% YoY to $168 million, with gross margins improving to 41.4% in the Products segment and 21.6% in ADI, reflecting segment-wise margin expansions of 190 basis points and 360 basis points, respectively. Adjusted EPS stood at $0.63, more than double the consensus forecast of $0.28, representing a 125% earnings surprise. Despite cash usage of $65 million in the quarter, Resideo maintained a solid liquidity position, backed by record free cash flow generation of $444 million in FY2024.

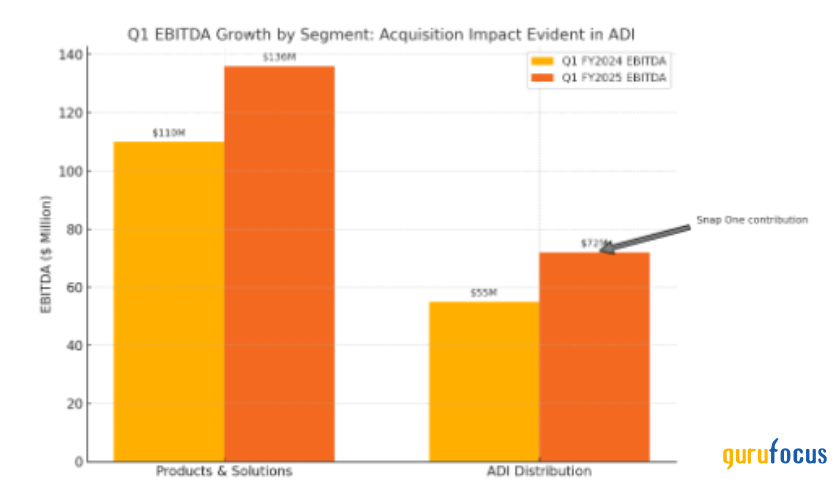

In Products & Solutions, Q1 revenue was $649M (+5% YoY, +6% organic) with a gross margin of 41.4% (↑1.9%). Volume grew on new Honeywell Home FocusPRO thermostats and BRK/First Alert alarms. Operating profit rose to $136M (21.0% of sales vs 18.1% year-ago). Notably, Resideo launched a connected First Alert smart smoke/CO alarm (compatible with Google Home) during Q1.In ADI Global Distribution, Q1 revenue was $1,121 mn (+29% YoY, +4% organic). The Snap One acquisition contributed $227 mn of this, while the core ADI business grew modestly on higher volume. ADI's gross margin was 21.6% (up 360 bp), and Adjusted EBITDA $72 mn (6.4% margin). Management reports Snap One integration is ahead of schedule, with synergies ramping. Overall, both segments saw double‑digit EBITDA growth and healthy margin improvement.

What Should We Expect In The Near Term?

The demand environment for REZI is expected to be steady in 2025. Management has also reaffirmed its guidance for 2025 with continued mid-single-digit organic growth and the Snap One's contribution. In the near term, the company plans further phased price increases to offset any tariffs or cost inflation. Over 98% of P&S product costs in Mexico are already tariff-exempt, and management expects to mitigate remaining tariff impacts through pricing actions. Furthermore, the Snap One unit continues to integrate into ADI, broadening the pro-audio/video portfolio. ADI's e-commerce channel and exclusive brand lines are expanding rapidly (Q1 e-commerce +15% organic). Combined organic ADI sales grew ~7% (daily) in Q1, indicating strength ahead.

Resideo is also rolling out new offerings to capture demand. Its Honeywell Home FocusPRO thermostat line (launched late 2024) has driven HVAC distributor orders. The new First Alert smart alarm (Q1 2025) addresses the expiring Nest Protect platform. A continued cadence of product launches is planned, especially energy-saving thermostats (e.g., a new S200 smart model with ENERGY STAR). Even though the current housing/consumer conditions are volatile, I believe the replacement demand for home safety/comfort products should support organic growth. The company is well-positioned if the consumer demand tightens with its inventory discipline and cost control measures.

Resideo Technologies' Long-Term Outlook

Over the long term, Resideo should deliver sustained, profitable growth in the smart-home and building controls markets by leveraging its diversified business model, strong brand portfolio, and expanding product lineup. The company is well-positioned to benefit from structural tailwinds in connected home technologies, including increased adoption of IoT thermostats, security systems, smoke detectors, and water monitoring devices. With nearly half of U.S. households now embracing smart home devices, Resideo's offerings in energy management, safety, air quality, and security provide a solid platform for growth. While primarily a hardware-centric business, recurring revenue streams are supported by its extensive professional installer network (ADI) and trusted Honeywell Home brand, further enhanced by Snap One's subscription-based services such as smart video and home automation systems.

The company should achieve its long-term margin expansion target through operational scale, improved product mix, and cost efficiencies. In Q4 2024, the Products & Solutions segment gross margin reached 41.0%, up 240 basis points year-over-year, with expectations of continued improvement as ADI benefits from Snap One's higher-margin offerings and growing e-commerce penetration. The company also maintains a robust innovation pipeline, demonstrated by the successful launch of its next-generation Honeywell Home thermostats in 2024, and plans to expand into advanced HVAC controls, safety devices, and water-sensing technologies. While macroeconomic headwinds and competition from DIY players like Google Nest, Amazon Ring, and Apple HomeKit pose risks, Resideo's emphasis on professional channels and its dual structure of manufacturing and distribution provide resilience. Management remains confident that the Snap One acquisition, coupled with a disciplined innovation and margin strategy, will support long-term value creation and profitable growth.

Resideo's Total Addressable Market (TAM)

According to industry estimates, the global smart home market is expected to exceed $170 billion by 2028, growing at a CAGR of over 10%. The smart security segment is projected to grow at a high single-digit pace, driven by increasing demand for connected thermostats, smoke detectors, and video surveillance systems. Resideo, through its Honeywell Home and First Alert brands, already enjoys strong installer trust and widespread distribution, with Honeywell thermostats having near-universal penetration in the U.S. HVAC installer channel. This positions the company favorably to capitalize on the expanding TAM, especially when integrating bolt-on acquisitions like Snap One, which can achieve outsized market access via Resideo's established dealer network.

Key Investor Movements

Institutional investor activity in the first quarter of 2025 signals growing confidence in Resideo Technologies' long-term prospects. Notably, renowned investor Ken Fisher (Trades, Portfolio) increased his stake in the company by 15%, reflecting his conviction in Resideo's growth trajectory and operational execution. Barrow, Hanley, Mewhinney & Strauss made a particularly strong statement of confidence with a substantial 149% increase in their holdings, indicating a bullish view on the company's valuation and strategic positioning following its Snap One acquisition. Additionally, respected value investor John Rogers (Trades, Portfolio) raised his stake by 5%, reinforcing optimism around Resideo's margin expansion potential and smart home market exposure.

Valuation & Comparison With Peers

Resideo's valuation is moderate by many measures. On a forward P/E basis (earnings in 2025), REZI trades around 10–12x. This exceeds its 5‑year historical average of 8x, reflecting the recent sharp rise in stock price. On an EV/EBITDA basis, Resideo's current multiple is only ~6x, well below its 5‑year average (~9.8x), thanks to rapid EBITDA growth.

Comparatively, Resideo's peers span a wide range: leading security/smart-home players often trade at higher multiples. For example, ADT Inc. (security systems) has a forward P/E around 9.9x (similar to Resideo), whereas Alarm.com (smart home SaaS) trades near 25x. Larger building controls firms like Johnson Controls or Carrier Global are in the mid‑20s P/E. Resideo's EV/EBITDA (~6×) is similar to ADT's (~6×) but far below Alarm.com's (~13×) and many industrial peers (~15–20×). In short, REZI appears reasonably priced for its growth: cheaper than high‑growth tech peers but richer than very defensive names. The discrepancy between P/E and EV/EBITDA reflects one-time items: Resideo's GAAP earnings were depressed by non-cash tariff reimbursements, inflating P/E. Using non-GAAP EBITDA or cash flow, Resideo looks inexpensive.

Investor Takeaways

Resideo's recent results demonstrate solid execution. The company delivered double‑digit revenue growth and margin expansion in Q1 2025, handily beating analyst estimates. Management's confidence (reiterated guidance, strong cash flow targets) suggests the business is on track. With Snap One integration ahead of schedule and new products coming to market, Resideo appears poised to sustain growth in both segments. From a financial perspective, Resideo trades at modest multiples relative to peers, especially on an EV/EBITDA basis. If Resideo fulfills its outlook, this could imply further upside for the stock. However, risks remain in a cyclical housing market and from one-time accounting items (which have distorted current earnings). Overall, Resideo is executing a clear strategy of margin improvement and innovation, and its balanced valuations make it a name of interest in the home security and controls sector.