Goldman Sachs has started coverage on Entegris (ENTG, Financial) with a Neutral rating, setting a price target of $85. The investment firm has taken a balanced approach when evaluating the U.S. semiconductor capital equipment, storage, and foundry sectors. Analysts observe that the semiconductor capital equipment industry is currently in a mid-cycle phase, where both challenges and opportunities contribute to steady revenue trends across the market.

While Goldman Sachs anticipates more potential losses than gains, they project a stable revenue environment through 2026. The firm notes that China offers more opportunities rather than threats for industry companies. Additionally, there is an expectation of upside within the hard-disk-drive market cycle, alongside a predicted recovery in NAND leading up to 2026.

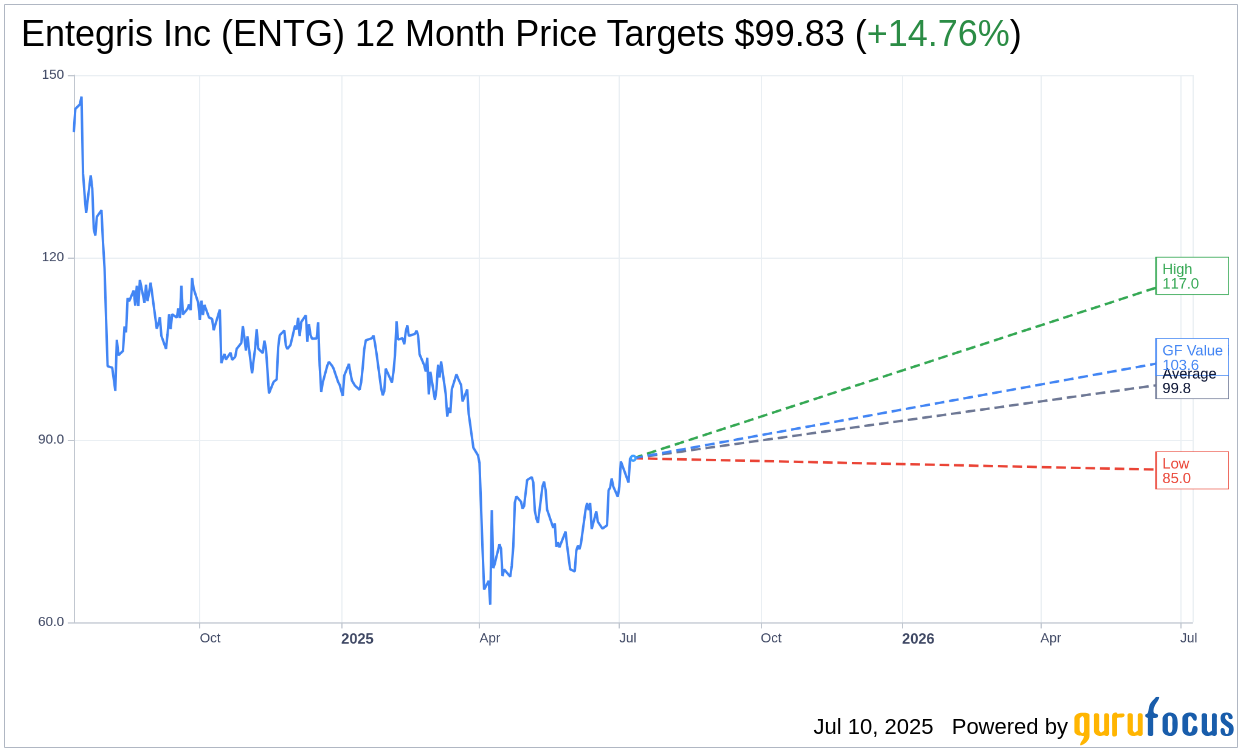

Wall Street Analysts Forecast

Based on the one-year price targets offered by 10 analysts, the average target price for Entegris Inc (ENTG, Financial) is $99.83 with a high estimate of $117.00 and a low estimate of $85.00. The average target implies an upside of 14.76% from the current price of $86.99. More detailed estimate data can be found on the Entegris Inc (ENTG) Forecast page.

Based on the consensus recommendation from 11 brokerage firms, Entegris Inc's (ENTG, Financial) average brokerage recommendation is currently 2.1, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Entegris Inc (ENTG, Financial) in one year is $103.64, suggesting a upside of 19.14% from the current price of $86.99. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Entegris Inc (ENTG) Summary page.

ENTG Key Business Developments

Release Date: May 07, 2025

- Revenue: $773 million, up 5% year over year, excluding divestitures; flat year over year on an as-reported basis, down 9% sequentially.

- Gross Margin: 46.1% on both GAAP and non-GAAP basis, at the midpoint of guidance.

- Operating Expenses: $234 million on a GAAP basis; $186 million on a non-GAAP basis, better than guidance.

- Adjusted EBITDA Margin: 28.5%, at the midpoint of guidance.

- GAAP Tax Rate: 11.5%; Non-GAAP Tax Rate: 15%.

- GAAP EPS: $0.41 per share; Non-GAAP EPS: $0.67 per share, at the midpoint of guidance.

- Material Solutions Sales: $341 million, up 8% year on year, excluding divestitures; down 5% sequentially.

- Advanced Purity Solutions Sales: $434 million, up 3% year on year; down 11% sequentially.

- Free Cash Flow: $32 million.

- Capital Expenditures: Expected to be approximately $300 million in 2025, down from $325 million.

- Gross Debt: Approximately $4 billion; Net Debt: $3.7 billion.

- Gross Leverage: 4.4 times; Net Leverage: 4 times.

- Q2 Revenue Guidance: $735 million to $775 million.

- Q2 Gross Margin Guidance: Approximately 45% on both GAAP and non-GAAP basis.

- Q2 GAAP EPS Guidance: $0.34 to $0.41 per share; Non-GAAP EPS Guidance: $0.60 to $0.67 per share.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Entegris Inc (ENTG, Financial) reported a 5% year-over-year revenue growth in Q1 2025, excluding divestitures.

- Materials Solutions sales increased by 8% year-over-year, driven by strong growth in CMP slurries and pads.

- The company is making progress with its new Colorado manufacturing site and expects to initiate customer qualifications in the second half of the year.

- Entegris Inc (ENTG) has developed well-integrated supply chain clusters around its largest manufacturing centers, enhancing its strategic advantage.

- The company is well-positioned to capture incremental content per wafer and outperform the market, with strong engagements in moly deposition materials and IPA purifiers.

Negative Points

- Q1 2025 revenue was slightly below guidance due to softer demand for fluid handling and FOUP products.

- The company faces significant uncertainty due to new tariff regimes, impacting its ability to provide precise revenue guidance.

- Entegris Inc (ENTG) expects a temporary impact on its top line related to sales to China due to new tariffs.

- Gross margin is expected to decline slightly in Q2 2025 due to volume deleveraging and tariff impacts.

- The company has paused M&A activities and is focusing on reducing its debt level amidst the uncertain environment.