Baird has increased its price target for Aptiv (APTV, Financial) shares to $82 from $80, maintaining a positive outlook on the stock. Analyst Luke Junk expressed greater optimism about the vehicle technology and mobility sector as the company approaches its second-quarter reports. According to Baird, auto suppliers like Aptiv are expected to exceed expectations in the second quarter, with projections for the third quarter appearing promising. This positive sentiment has led to adjustments in estimates and price targets, which now reflect stronger fundamentals within the industry.

Wall Street Analysts Forecast

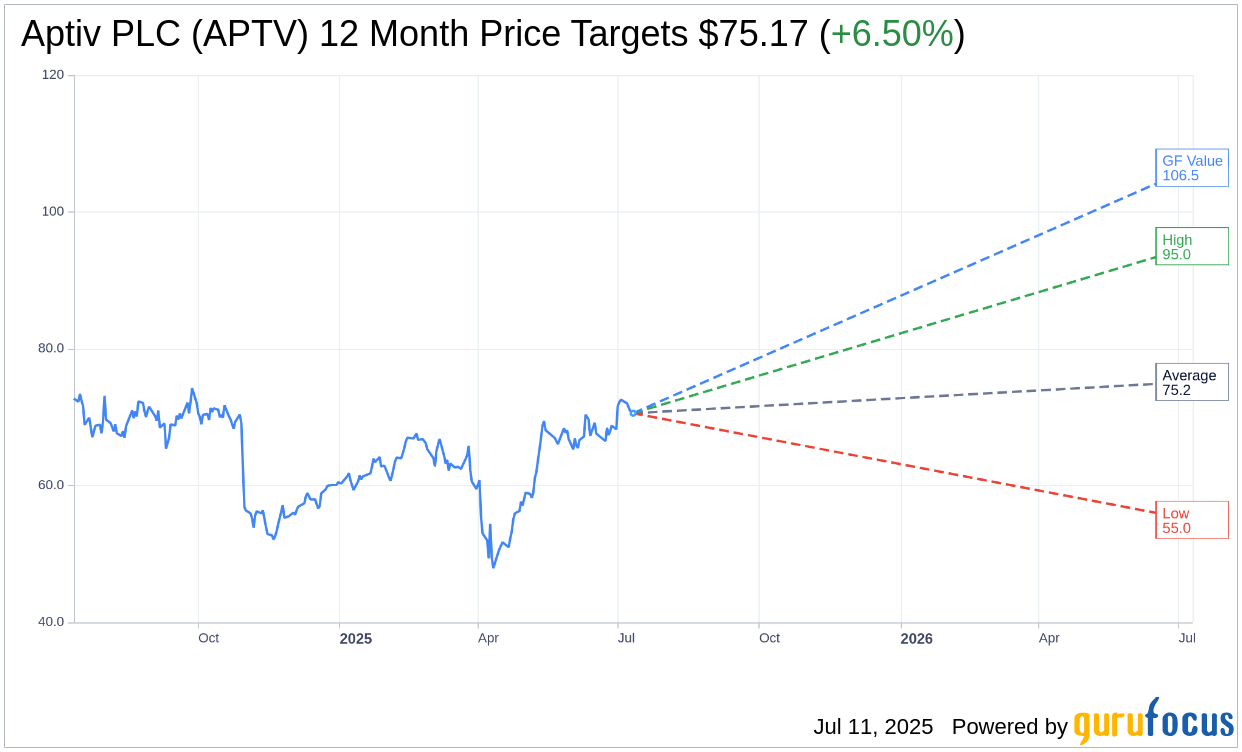

Based on the one-year price targets offered by 17 analysts, the average target price for Aptiv PLC (APTV, Financial) is $75.17 with a high estimate of $95.00 and a low estimate of $55.00. The average target implies an upside of 6.50% from the current price of $70.58. More detailed estimate data can be found on the Aptiv PLC (APTV) Forecast page.

Based on the consensus recommendation from 22 brokerage firms, Aptiv PLC's (APTV, Financial) average brokerage recommendation is currently 2.2, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Aptiv PLC (APTV, Financial) in one year is $106.48, suggesting a upside of 50.86% from the current price of $70.58. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Aptiv PLC (APTV) Summary page.

APTV Key Business Developments

Release Date: May 01, 2025

- Revenue: $4.8 billion, down 1% year-over-year.

- Operating Income: $572 million, an increase of over 5%.

- Earnings Per Share (EPS): $1.69, a first quarter record.

- Operating Cash Flow: $273 million.

- Share Repurchase Program: Completed $3 billion program, reducing share count by 18%.

- Bookings: Nearly $5 billion in the first quarter.

- Advanced Safety and User Experience Revenue: Flat, with active safety revenues up 9%.

- Engineered Components Group Revenue: Increased 1%, with China revenues up 24%.

- Electrical Distribution Systems Revenue: Declined 3%.

- Adjusted EBITDA: $758 million.

- Operating Income Margin: Expanded 80 basis points year-over-year.

- Capital Expenditures: $197 million in the quarter.

- Second Quarter Revenue Guidance: $4.92 billion to $5.12 billion.

- Second Quarter Operating Income Guidance: $575 million at the midpoint.

- Second Quarter EPS Guidance: $1.80 at the midpoint.

- Debt Reduction: Paid down approximately $700 million of debt since the start of the year.

- Liquidity: Over $3.4 billion with net leverage at 2.2 times.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Aptiv PLC (APTV, Financial) exceeded its first-quarter guidance due to higher vehicle production volumes, particularly in China, and strong growth in non-automotive markets.

- Operating income reached a record $572 million, reflecting a 5% increase due to strong operating execution and cost reduction initiatives.

- The company completed a $3 billion accelerated share repurchase program, reducing its share count by 18% and enhancing shareholder value.

- Aptiv PLC (APTV) secured nearly $5 billion in new business awards, with significant traction in China, including $1.4 billion in bookings with local OEMs.

- The company announced strategic partnerships with ServiceNow and Capgemini to expand its cloud solutions, enhancing its footprint in the enterprise sector.

Negative Points

- Revenue declined by 1% to $4.8 billion due to lower vehicle production in North America and Europe, and negative customer mix.

- The company faces uncertainty due to rapid changes in global trade policies, impacting demand in the automotive market.

- Aptiv PLC (APTV) is experiencing delays in customer program awards due to trade policy and regulatory changes.

- The Electrical Distribution Systems (EDS) segment saw a 3% revenue decline, primarily due to lower light vehicle production.

- The company is cautious about the second half of the year due to uncertain vehicle production volumes and consumer demand.