DA Davidson has revised its price target for WD-40 (WDFC, Financial), reducing it from $322 to $300, while maintaining a Buy rating on the stock. This adjustment follows the company's third-quarter results and updated guidance. WD-40 reported significant growth in its largest market, along with improved gross margins and increased profits compared to the prior quarter.

The performance in the Americas and Asia-Pacific regions was notably strong, which helped counterbalance a downturn in EIMEA. The decline in EIMEA was primarily attributed to timing issues related to customer orders in some areas.

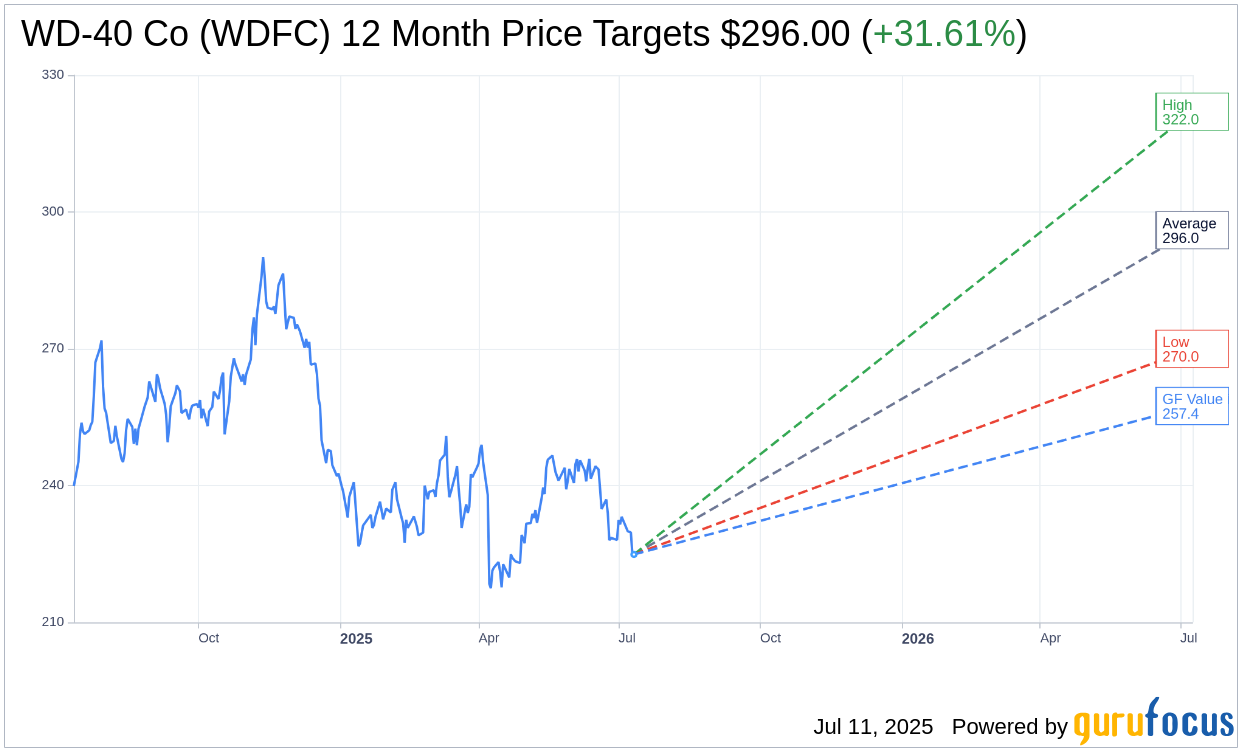

Wall Street Analysts Forecast

Based on the one-year price targets offered by 2 analysts, the average target price for WD-40 Co (WDFC, Financial) is $288.50 with a high estimate of $322.00 and a low estimate of $255.00. The average target implies an upside of 28.28% from the current price of $224.90. More detailed estimate data can be found on the WD-40 Co (WDFC) Forecast page.

Based on the consensus recommendation from 2 brokerage firms, WD-40 Co's (WDFC, Financial) average brokerage recommendation is currently 2.5, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for WD-40 Co (WDFC, Financial) in one year is $257.45, suggesting a upside of 14.47% from the current price of $224.9. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the WD-40 Co (WDFC) Summary page.

WDFC Key Business Developments

Release Date: July 10, 2025

- Net Sales: $156.9 million in Q3 2025, a 1% increase year-over-year.

- Maintenance Products Sales: $150.4 million in Q3 2025, a 2% year-over-year increase.

- Americas Sales: $78.2 million in Q3 2025, a 4% increase year-over-year.

- EIMEA Sales: $56.7 million in Q3 2025, a 5% decrease year-over-year.

- Asia Pacific Sales: $22 million in Q3 2025, a 7% increase year-over-year.

- Gross Margin: 56.2% in Q3 2025, up from 53.1% last year.

- Adjusted EBITDA Margin: 20% in Q3 2025, up from 19% last year.

- Operating Income: $27.4 million in Q3 2025, a 1% increase year-over-year.

- Diluted EPS: $1.54 in Q3 2025, up from $1.46 last year.

- Cash Flow from Operations: $35 million in Q3 2025.

- Dividend: $0.94 per share approved on June 17, 2025.

- Share Repurchase: Approximately 12,750 shares repurchased at a cost of $3 million in Q3 2025.

- FY25 Net Sales Guidance: Projected growth between 6% and 9%, with net sales between $600 million and $620 million.

- FY25 Gross Margin Guidance: Expected to be between 55% and 56%.

- FY25 Operating Income Guidance: Increased to between $96 million and $101 million.

- FY25 Diluted EPS Guidance: Expected to be between $5.30 and $5.60.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- WD-40 Co (WDFC, Financial) reported a record sales quarter with net sales of $156.9 million, marking a 1% increase compared to the same period last year.

- The company's gross margin improved significantly to 56.2%, up from 53.1% last year, driven by higher average selling prices and lower input costs.

- Sales of WD-40 Specialist products increased by 11% year-to-date, reflecting strong demand and effective promotional activities.

- E-commerce sales were up 11% year-to-date, highlighting the success of WD-40 Co (WDFC)'s digital commerce strategy.

- The company has a strong employee retention rate, with an average tenure of eight years, double the US median, contributing to sustained growth and stability.

Negative Points

- Sales in the EIMEA region declined by 5% in the third quarter, primarily due to lower sales volumes in Turkey and the Middle East.

- The company's cost of doing business increased to 38% of net sales, up from 34% in the same period last year, driven by higher employee-related expenses.

- Homecare and cleaning product sales declined in several regions, reflecting a strategic shift towards maintenance products but impacting overall sales figures.

- Foreign currency exchange rates posed a headwind, impacting net sales figures and contributing to variability in financial performance.

- The planned divestiture of the homecare and cleaning business remains uncertain, potentially affecting future financial outcomes and strategic focus.