Morgan Stanley has revised its price target for Primerica (PRI, Financial), reducing it slightly from $296 to $292. Despite this adjustment, the firm maintains its Equal Weight rating on the stock. This suggests that while there is a slight downward revision in expectations, the overall view on the company's performance remains stable.

Wall Street Analysts Forecast

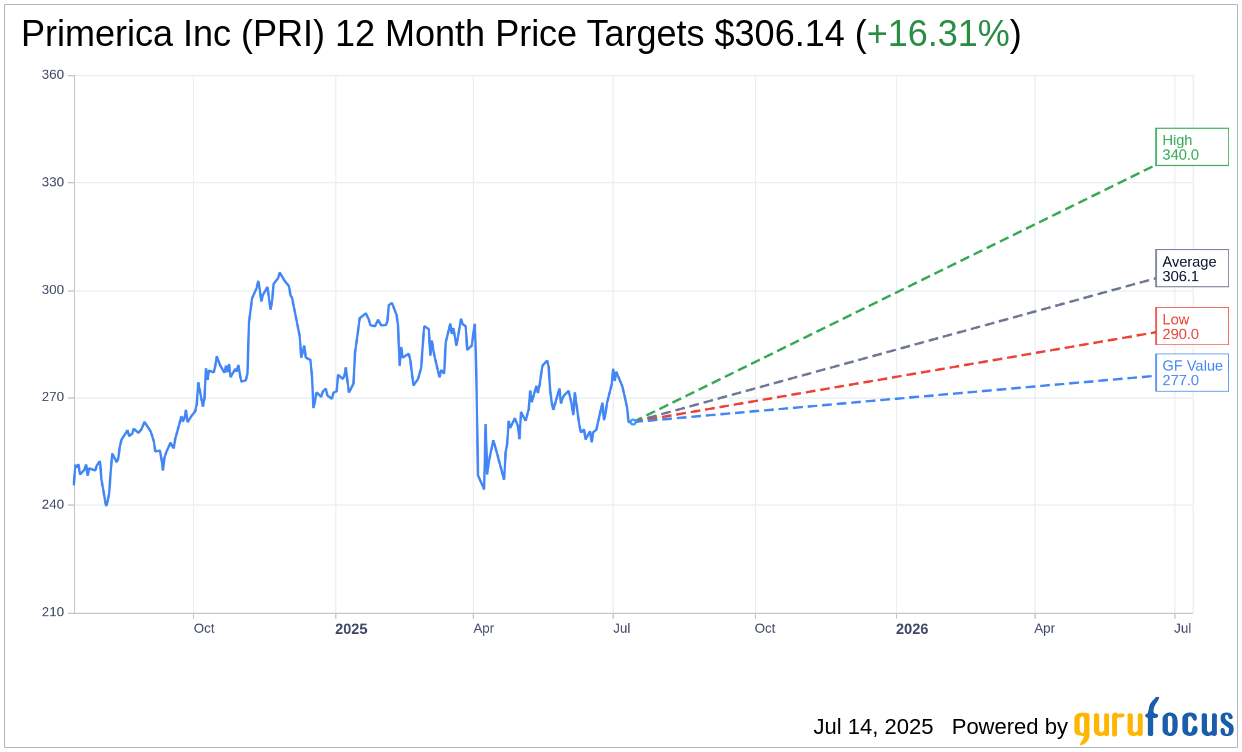

Based on the one-year price targets offered by 7 analysts, the average target price for Primerica Inc (PRI, Financial) is $306.14 with a high estimate of $340.00 and a low estimate of $290.00. The average target implies an upside of 16.31% from the current price of $263.21. More detailed estimate data can be found on the Primerica Inc (PRI) Forecast page.

Based on the consensus recommendation from 9 brokerage firms, Primerica Inc's (PRI, Financial) average brokerage recommendation is currently 2.8, indicating "Hold" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Primerica Inc (PRI, Financial) in one year is $277.01, suggesting a upside of 5.24% from the current price of $263.21. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Primerica Inc (PRI) Summary page.

PRI Key Business Developments

Release Date: May 08, 2025

- Adjusted Net Operating Income: $168 million, up 14% year over year.

- Diluted Adjusted Operating EPS: Increased 20% to $5.02.

- Shareholder Returns: $153 million returned, including $118 million in share repurchases and $35 million in dividends.

- Recruitment: 100,867 individuals recruited, a 9% decline year over year.

- New Life Licenses: Declined 5% year over year.

- New Term Life Policies: 86,415 issued, representing $28 billion in new protection.

- Term Life Operating Revenue: $458 million, up 4% year over year.

- Term Life Pre-tax Operating Income: $147 million, up 6% year over year.

- ISP Segment Sales: $3.6 billion, up 28% year over year.

- Net Inflows: $839 million, compared to $274 million in the prior year period.

- Client Asset Values: $110 billion, up 6% year over year.

- Investment and Savings Product Operating Revenue: $291 million, up 19% year over year.

- Investment and Savings Product Pre-tax Income: $81 million, up 24% year over year.

- Closed Loans in the US: $93.5 million, up 31%.

- Closed Loans in Canada: $43.3 million, up 78%.

- Consolidated Insurance and Other Operating Expenses: $163 million, up 4% year over year.

- Holding Company Cash and Invested Assets: $407 million.

- Primerica Life Estimated RPC Ratio: 470%.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Adjusted net operating income increased by 14% year over year to $168 million, with diluted adjusted operating EPS up 20% to $5.02.

- The investment and savings product segment saw a 28% year-over-year increase in total sales, driven by strong demand across mutual funds, variable annuities, and managed accounts.

- Primerica Inc (PRI, Financial) returned $153 million to stockholders through share repurchases and dividends during the quarter.

- The company experienced strong sales growth in its mortgage business in both the US and Canada, with closed loans up 31% in the US and 78% in Canada.

- Persistency in term life policies remained stable, with $957 billion of protection in place for middle-income families at quarter-end.

Negative Points

- Recruiting declined by 9% year over year, with new life licenses down 5%, attributed to economic uncertainty and cost-of-living pressures.

- Term life insurance sales faced pressure, with productivity slightly below historical ranges at 0.19 policies per representative.

- The company experienced a 2% decline in client asset values during the first three months of 2025 due to negative market performance.

- Overall lapse rates remain above long-term expectations, reflecting ongoing financial impacts from higher cost-of-living pressures on middle-income families.

- Economic uncertainty is contributing to a slowdown in recruiting and investment sales momentum, with potential impacts on future growth.