Recent analysis by Morgan Stanley indicates a notable shift for Hims & Hers Health, Inc. (HIMS, Financial), revealing a year-over-year decrease in app downloads for the first time. The company's app downloads have now settled at 185,000, marking a dip below pre-launch levels of their compounded GLP-1s. Additionally, web traffic saw a modest growth of just 5% in June, the slowest pace since March 2024.

Morgan Stanley maintains an Equal Weight rating on Hims & Hers shares, accompanied by a price target of $40. This development suggests investors may need to reassess their strategies regarding HIMS in light of the latest metrics.

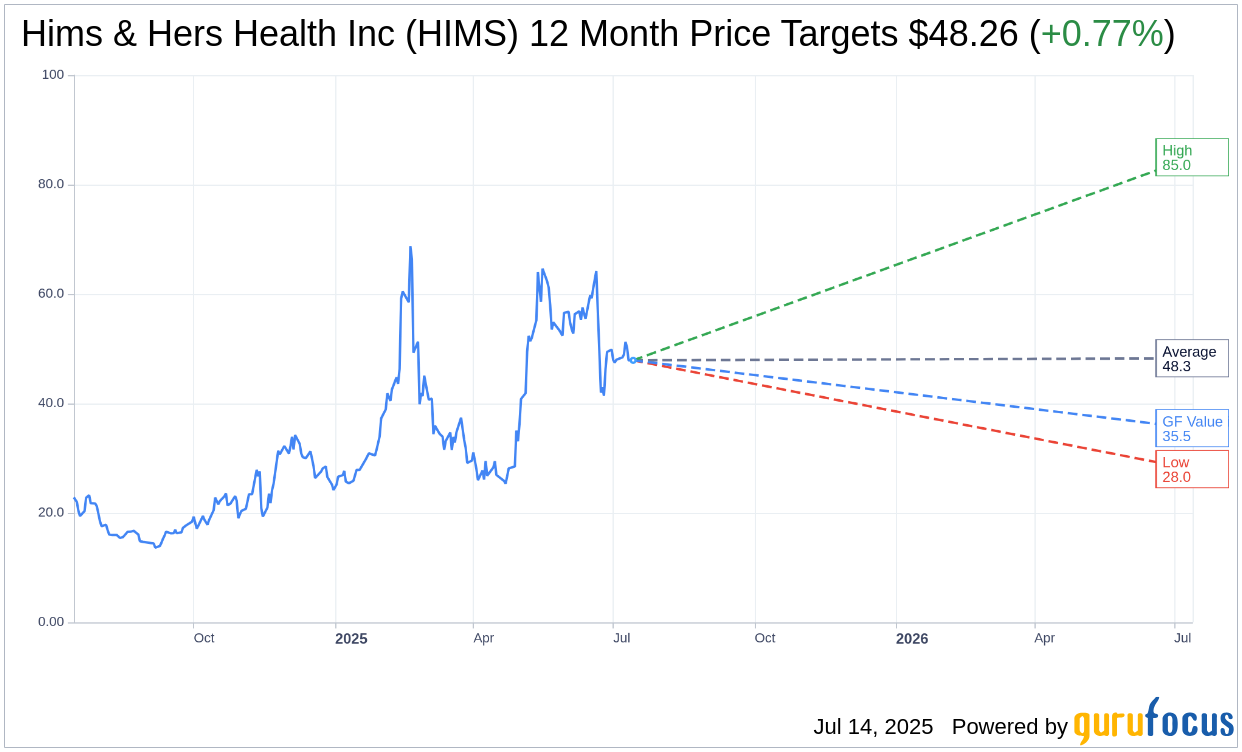

Wall Street Analysts Forecast

Based on the one-year price targets offered by 13 analysts, the average target price for Hims & Hers Health Inc (HIMS, Financial) is $48.26 with a high estimate of $85.00 and a low estimate of $28.00. The average target implies an upside of 0.77% from the current price of $47.89. More detailed estimate data can be found on the Hims & Hers Health Inc (HIMS) Forecast page.

Based on the consensus recommendation from 14 brokerage firms, Hims & Hers Health Inc's (HIMS, Financial) average brokerage recommendation is currently 2.8, indicating "Hold" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Hims & Hers Health Inc (HIMS, Financial) in one year is $35.48, suggesting a downside of 25.91% from the current price of $47.89. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Hims & Hers Health Inc (HIMS) Summary page.

HIMS Key Business Developments

Release Date: May 05, 2025

- Revenue: $586 million, up 111% year over year.

- Adjusted EBITDA: $91 million, nearly triple from the same quarter last year.

- Adjusted EBITDA Margin: Nearly 16%, expanded by over 4 points quarter over quarter.

- Subscriber Base: Nearly 2.4 million, a year-over-year increase of 38%.

- Monthly Online Revenue per Average Subscriber: $84, up more than 50% year over year.

- Gross Margin: Declined approximately 3 points quarter over quarter.

- Marketing Spend: 39% of revenue, improved by 8 points year over year.

- Cash Flow from Operations: $109 million.

- Free Cash Flow: $50 million.

- Cash and Short-term Investments: $323 million at quarter end.

- Capital Expenditures (CapEx): $59 million invested in the first quarter.

- Guidance for Q2 2025 Revenue: $530 million to $550 million, representing growth of 68% to 74% year over year.

- Guidance for Q2 2025 Adjusted EBITDA: $65 million to $75 million, reflecting a 13% margin at the midpoint.

- Full Year 2025 Revenue Guidance: $2.3 billion to $2.4 billion, up 56% to 63% year over year.

- Full Year 2025 Adjusted EBITDA Guidance: $295 million to $335 million, reflecting a 13% margin at the midpoint.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Revenue grew 111% year over year to $586 million, demonstrating strong momentum.

- Subscriber base increased by 38% year over year, reaching nearly 2.4 million.

- Partnership with Novo Nordisk expands access to branded Wegovy, enhancing weight loss offerings.

- Adjusted EBITDA nearly tripled, reaching $91 million, indicating improved profitability.

- Expansion into new specialties like low testosterone and menopause support is underway, broadening service offerings.

Negative Points

- Gross margins declined approximately 3 points quarter over quarter due to scaling of GLP-1 revenue.

- Volatility expected in sexual health growth as the company transitions to more premium daily products.

- Marketing efficiency may experience volatility as the company leans into specialty-specific marketing.

- Transition of subscribers off commercially available semaglutide expected to result in a one-time revenue drop in Q2.

- Potential headwinds from macroeconomic factors such as tariffs could impact gross margins.