Hancock Whitney Corporation (HWC, Financial) reported an increase in its loan loss provision for the second quarter, rising to $14.9 million from $8.7 million in the same period last year. This indicates a notable year-over-year increase in potential risk coverage.

The company's Return on Assets (ROA) was recorded at 1.32% for the second quarter. However, when adjusting for supplemental disclosure items, the ROA slightly increased to 1.37%, compared to a ROA of 1.41% in the previous quarter. This adjustment reflects a minor decline in profitability compared with the last quarter.

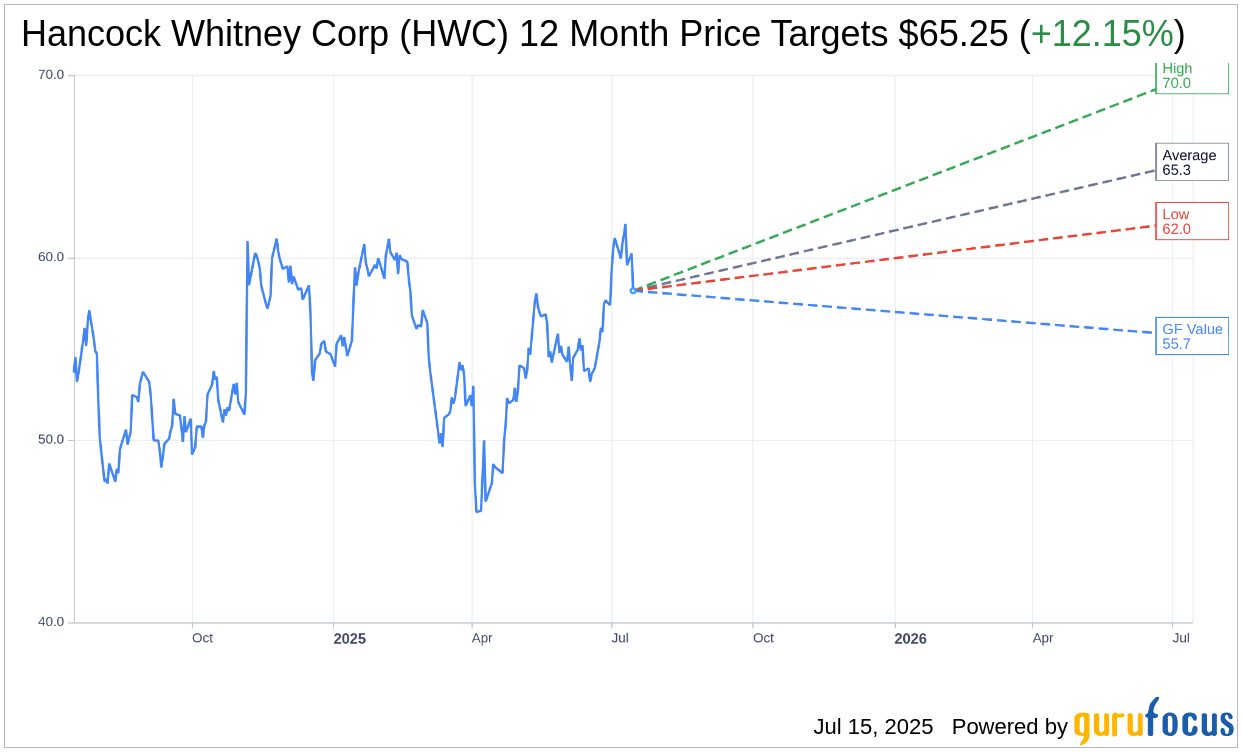

Wall Street Analysts Forecast

Based on the one-year price targets offered by 8 analysts, the average target price for Hancock Whitney Corp (HWC, Financial) is $65.25 with a high estimate of $70.00 and a low estimate of $62.00. The average target implies an upside of 12.15% from the current price of $58.18. More detailed estimate data can be found on the Hancock Whitney Corp (HWC) Forecast page.

Based on the consensus recommendation from 8 brokerage firms, Hancock Whitney Corp's (HWC, Financial) average brokerage recommendation is currently 1.9, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Hancock Whitney Corp (HWC, Financial) in one year is $55.70, suggesting a downside of 4.26% from the current price of $58.18. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Hancock Whitney Corp (HWC) Summary page.

HWC Key Business Developments

Release Date: April 15, 2025

- Return on Assets (ROA): 1.41%

- Total Risk-Based Capital: 16.39%

- Net Income: $120 million or $1.38 per share

- Net Interest Margin (NIM): Expanded 2 basis points to 3.43%

- Fee Income Growth: Expected to be up between 9% and 10% year over year

- Expense Growth: Expected between 4% and 5% year over year

- Loan Growth: Expected low single digits in 2025

- Deposits: Down $298 million

- Common Equity Tier 1 Ratio: 14.51%

- Tangible Common Equity Ratio: 10.01%

- Share Repurchases: 350,000 shares

- Dividend Increase: $0.45 per share, a 50% increase from last year

- Cost of Funds: Down 14 basis points to 1.59%

- Loan Yield: Down 18 basis points to 5.84%

- Net Charge-Offs: 18 basis points

- Allowance for Credit Losses: 1.49% of loans

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Hancock Whitney Corp (HWC, Financial) reported a strong start to 2025 with a 1.41% return on assets (ROA) and continued capital growth.

- The company achieved net income of $120 million or $1.38 per share, with earnings up 10% compared to the same quarter a year ago.

- Net interest margin (NIM) expanded by 2 basis points to 3.43%, driven by lower deposit costs and higher yields on the bond portfolio.

- Fee income grew across most categories, with expectations for a 9% to 10% increase year over year, partly due to the Sabal Trust transaction.

- Hancock Whitney Corp (HWC) continues to return capital to investors, repurchasing 350,000 shares and increasing the common stock dividend by 50% from last year.

Negative Points

- Loans were down $201 million due to higher payoffs on large healthcare and commercial non-real estate loans.

- Deposits decreased by $298 million, primarily driven by seasonal public funds outflows.

- The company lowered its loan growth guidance to low single digits for 2025, with most growth expected in the second half of the year.

- Net interest income (NII) was down due to two fewer accrual days and a lower level of average earning assets.

- The company faces uncertainty in the economic environment, which could impact future growth and performance.