Introduction

Cigna isn't a stock that commands meme buzz or makes headlines for flashy innovation. It's a $90 billion healthcare insurer that quietly generates over $180 billion in annual revenue, maintains strong free cash flow, and returns billions to shareholders through aggressive buybacks. Yet the market treats it like a sluggish legacy player. At just 9x forward earnings and under 1x tangible book, Cigna screens like a business in decline. But that's far from reality. Beneath the modest valuation is a structurally advantaged business model: a blend of sticky insurance premiums, a fast-growing pharmacy benefit segment, and a disciplined capital allocation strategy. Cigna generates 20%+ return on equity, has shrunk its share count by 35% over the past decade, and remains one of the few large-cap healthcare names actively returning cash on scale.

In a market that often favors story over substance, Cigna is doing the opposite, delivering cash-backed value while being priced like a risk. For long-term investors focused on durable earnings and disciplined capital returns, Cigna may be one of the most attractively mispriced compounders in healthcare.

History of Compounding and Business Model Strength

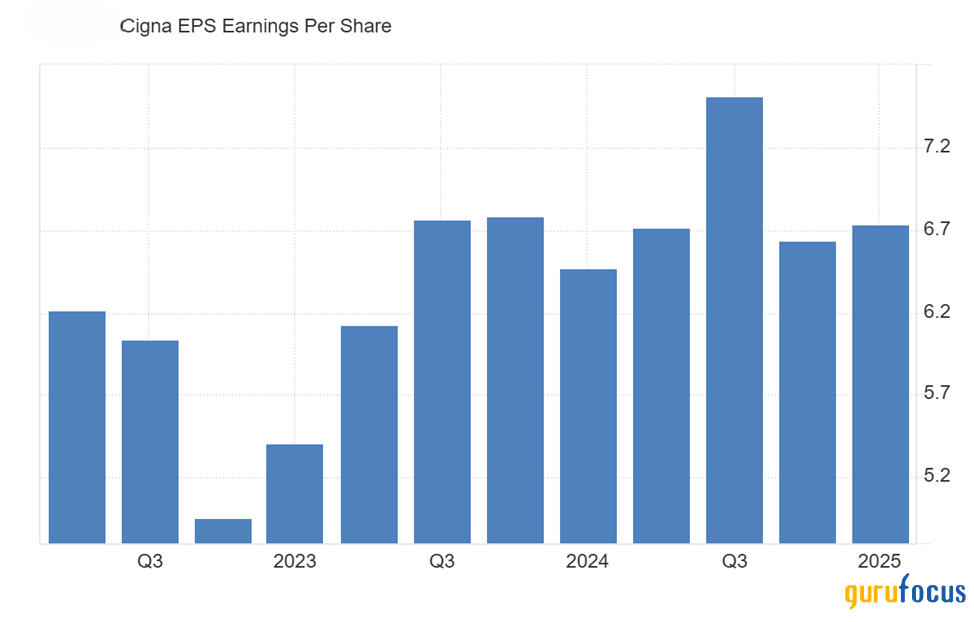

Cigna's core earnings engine blends two highly resilient segments: health insurance and pharmacy benefits management (PBM). Its commercial and government-backed health plans generate consistent premium revenue with low churn. At the same time, its PBM arm, Express Scripts, processes over 1 billion prescriptions annually and operates on a scale that few can match. This dual-engine structure is a key advantage. Insurance provides sticky revenue and predictable cash flow, while Express Scripts gives Cigna negotiating leverage with drug manufacturers and healthcare providers. That scale advantage has allowed Cigna to grow earnings per share at a compounded rate of 14% over the past decade, even as the broader healthcare sector faced margin compression and rising regulatory scrutiny.

Cigna's capital-light model helps maintain high returns on equity (averaging 20%+ in recent years), with limited need for reinvestment. The company has also steadily improved its underwriting discipline, maintaining a consistent medical loss ratio in the low 80s, despite the COVID-era volatility. Meanwhile, administrative cost leverage has expanded operating margins across both segments. What is overlooked is how aggressively Cigna has utilized this cash flow to repurchase shares. Since 2013, Cigna has repurchased nearly $30 billion worth of stock, reducing its share count by over one-third while growing per-share book value and earnings. That's compounding the right way: through real profitability, not dilution or debt-fueled expansion.

Understanding Express Scripts

Cigna's 2018 acquisition of Express Scripts wasn't just about scale; it was a strategic move to embed a capital-light, cash-generating asset into its ecosystem. Express Scripts is one of the largest pharmacy benefit managers (PBMs) in the United States. At its core, it negotiates with drug manufacturers to secure discounts, manages drug formularies (the list of covered medications), processes prescription claims, and contracts with pharmacies. This layer of coordination simplifies an otherwise fragmented and opaque system. For doctors, it provides a clear path for prescribing; for patients, it ensures cost control and broad pharmacy access; for drugmakers, it offers volume and distribution certainty; and for pharmacies, it streamlines billing and reimbursement. The result is a platform that reduces complexity and friction across every stakeholder in the drug supply chain.

This operational role also creates high switching costs. Employers and insurers typically sign multi-year contracts due to the integration burden of switching PBMs. Once Express Scripts is embedded into a company's healthcare infrastructure, it's rarely replaced. These sticky relationships, combined with scale economics and consistent cash flow, make Express Scripts a quietly dominant force within Cigna, amplifying the parent company's returns without requiring massive reinvestment.

A Market Built for Long-Term Compounding

Cigna's capital efficiency is well-known; its return on equity consistently exceeds 12%, and return on assets remains strong even with a complex mix of services. But what makes this particularly powerful is the size of the opportunity in front of it. Cigna currently holds just about 17% market share in the U.S. commercial health insurance market, despite being one of the most integrated and efficient players in the system. The total addressable market in U.S. healthcare spending exceeds $4.5 trillion annually, with employer-sponsored and government programs accounting for the bulk of that figure. Within this ecosystem, Cigna plays multiple roles: insurer, pharmacy benefit manager, behavioral health provider, and care coordinator. Each business line feeds into the next, creating a flywheel of services that drives retention and increases share of wallet per member.

The under-penetration across segments like behavioral health, care coordination, and even international markets leaves plenty of white space for growth. And because each dollar of retained earnings compounds at high internal rates of return, even modest organic growth can drive meaningful long-term gains. If Cigna continues to capture incremental market share, even a few basis points per the compounding engine can run for decades. This isn't a story about hypergrowth. It's about depth, integration, and expanding economic gravity in a massive, complex industry that rewards operational precision. Cigna's combination of scale and discipline gives it a long runway few peers can match.

Valuation VS Peers

Despite consistently solid returns on capital and disciplined capital allocation, Cigna trades at a steep discount to its managed care peers. At ~9.5x forward earnings and ~1.3x tangible book value, the stock is priced as if its fundamentals have stalled. But Cigna's financial profile tells a different story, one of stable margins, rising free cash flow, and focused execution.

| Metric | Cigna (CI, Financial) | UnitedHealth (UNH) | Elevance (ELV) | CVS Health (CVS) |

| Forward P/E | ~9.5x | ~20x | ~14x | ~8.9x |

| Price/Tangible Book | ~1.3x | ~5.2x | ~2.9x | ~1.2x |

| Return on Equity (ROE) | ~15.5% | ~25% | ~17% | ~8% |

| Shareholder Yield (TTM) | ~6.8% | ~3.2% | ~4.6% | ~5.3% |

While CVS trades at a similarly low multiple, it carries far more operational complexity and integration risk. Cigna, by contrast, has exited non-core segments, focused on capital-light, recurring-revenue businesses, and is now returning nearly 7% of its market cap annually to shareholders, If the stock were to re-rate even to the peer group's average forward multiple of ~14x, it would imply more than 40% upside without assuming any earnings growth. That rerating potential, combined with consistent buybacks and a structurally lean model, makes the valuation disconnect increasingly hard to ignore.

Despite its significant reshaping of the business, Cigna's current market capitalization of approximately $79 billion remains only modestly above the $67 billion it paid for Express Scripts back in 2018. That delta, just $12 billion over six years, is striking given the scale of the acquisition and the company's robust earnings growth since. The subdued valuation partly reflects aggressive share repurchases; Cigna has retired billions in stock since the deal closed, driving EPS growth and improving capital efficiency. But it also reveals how little credit the market has given the company for integrating Express Scripts successfully, especially at a time when pharmacy benefit managers are more essential than ever in managing healthcare costs. For long-term investors, this gap between strategic execution and market recognition may represent the clearest case of mispricing.

Who's buying

Cigna hasn't made headlines or fueled retail chatter, but it's quietly built a loyal following among seasoned value investors, many of whom have been adding to their stakes as the stock trades near multi-year valuation lows.

Lakewood Capital, led by Anthony Bozza, holds Cigna as its largest position by portfolio weight, an 11.5% bet worth nearly $130 million. With an average cost of $232.95 and a recent 10.8% increase in position size, this isn't a passive holding; it's a concentrated conviction. Lakewood's strategy favors overlooked compounders with solid balance sheets and recurring cash flows. Cigna, having divested Medicare Advantage and doubled down on high-ROE assets like Express Scripts, fits that mold precisely.

Owl Creek Asset Management, run by Jeffrey Altman, raised its stake by 75% last quarter, while Camber Capital, managed by Stephen DuBois, added 33%. Both funds have a track record of targeting high-margin businesses undergoing structural shifts, exactly the environment Cigna is navigating post-divestiture. Their actions suggest they're not reacting to short-term volatility but positioning for durable value creation.

Notably, Davis Selected Advisers, a long-time holder with deep familiarity with Cigna and its PBM business, maintains a stake exceeding 1.4 million shares with a cost basis of $212.27, still up over 40% despite recent pullbacks. Davis was likely a shareholder of Express Scripts before its acquisition, underscoring the firm's long-term understanding of the business. BloombergSen, a Canada-based value shop, added shares at an average price of $190.14 and is currently sitting on a nearly 60% gain.

While some holders like Glenview and Sanders trimmed modestly, most of the company's top shareholders either held or added, reinforcing the view that recent price weakness has created opportunity, not a broken thesis.

Considerations: Not Without Risks, But Mispriced Nonetheless

No insurance is risk-free, and Cigna is no exception. As a major player in the managed care space, Cigna's earnings are tethered to regulatory changes, employer-sponsored enrollment trends, and pharmacy benefit dynamics of which can be politically sensitive and margin-volatile. The recent sale of its Medicare Advantage business reflects a desire to avoid headwinds in one of the most tightly scrutinized parts of the insurance market, but it also reduces future optionality. There's also the risk of execution in the pharmacy benefits segment, where Express Scripts still faces pricing pressure and increasing calls for transparency. Cigna's scale helps, but continued scrutiny around rebate practices could pressure margins over time. On top of that, large-cap health insurers now face growing political attention, especially in election years, making sentiment as much a risk factor as operations.

Still, most of these risks are known and, more importantly, priced in. Cigna trades at just ~10x forward earnings and under 0.9x tangible book value, levels rarely seen for a business with 15%+ ROE, strong free cash flow conversion, and a long runway for buybacks. Its debt is well-laddered, with no near-term maturities creating liquidity strain, and management has explicitly committed to returning $10 billion to shareholders over the next 12 months. That's over 10% of the company's market cap in capital return, without relying on any earnings growth.

In short, Cigna doesn't need optimism to outperform. It just needs time. With defensive cash flows, structural capital efficiency, and quiet but growing guru ownership, Cigna offers an increasingly rare setup: a durable business priced as if uncertainty is permanent.