Paychex (PAYX, Financial) has entered into a new collaboration with SoFi to enhance its financial well-being offerings via Paychex Flex Perks. This partnership aims to provide access to SoFi’s broad range of financial resources, such as personal loans and loan refinancing, through the Paychex digital marketplace. By leveraging SoFi's solutions, employees of Paychex client companies can work towards achieving financial independence. The integration is facilitated through the Paychex Flex HCM platform, offering a seamless experience for users seeking to improve their financial health.

Wall Street Analysts Forecast

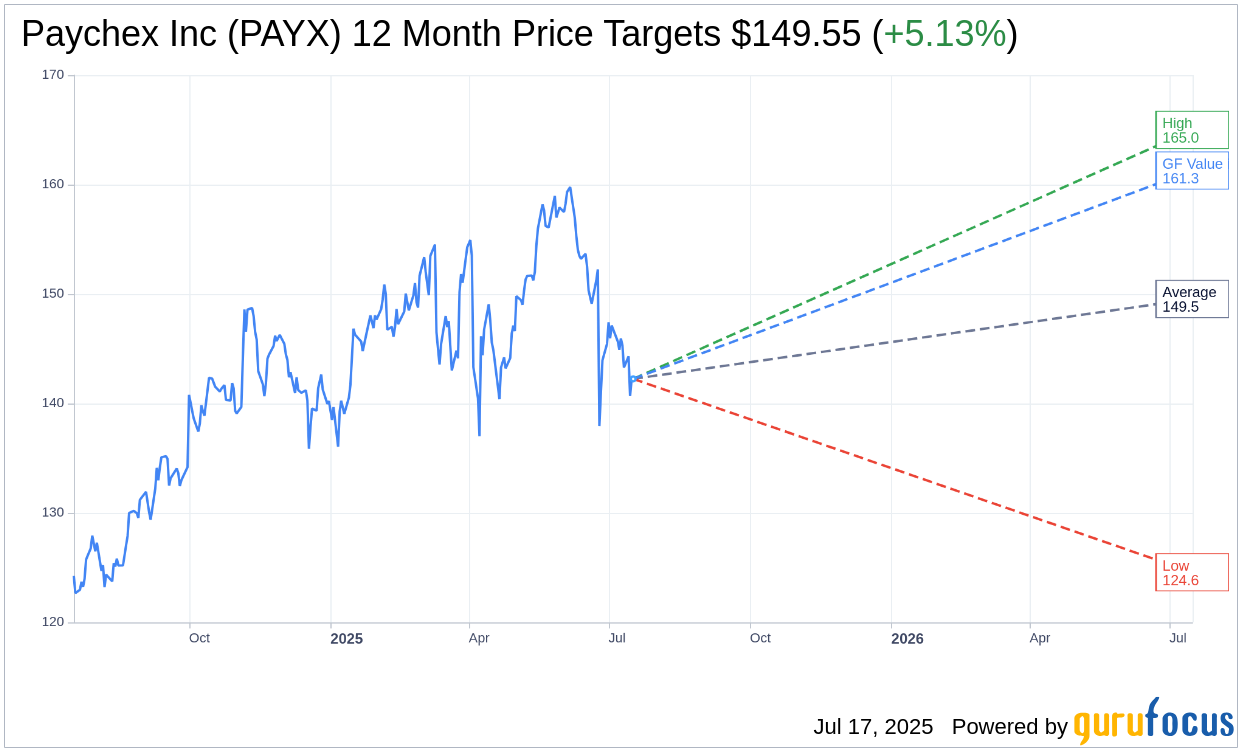

Based on the one-year price targets offered by 12 analysts, the average target price for Paychex Inc (PAYX, Financial) is $149.55 with a high estimate of $165.00 and a low estimate of $124.58. The average target implies an upside of 5.13% from the current price of $142.25. More detailed estimate data can be found on the Paychex Inc (PAYX) Forecast page.

Based on the consensus recommendation from 17 brokerage firms, Paychex Inc's (PAYX, Financial) average brokerage recommendation is currently 3.1, indicating "Hold" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Paychex Inc (PAYX, Financial) in one year is $161.29, suggesting a upside of 13.38% from the current price of $142.25. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Paychex Inc (PAYX) Summary page.

PAYX Key Business Developments

Release Date: June 25, 2025

- Q4 Revenue Growth: 10% increase to $1.4 billion.

- Full Year Revenue Growth: 6% increase to $5.6 billion.

- Management Solutions Revenue (Q4): 12% increase to $1 billion.

- PEO and Insurance Solutions Revenue (Q4): 4% increase to $340 million.

- Interest on Funds Held for Clients (Q4): 18% increase to $45 million.

- Operating Income Margin (Q4): 30.2% GAAP, 40.4% adjusted.

- Adjusted Diluted EPS (Q4): 6% increase to $1.19.

- Operating Margins (Full Year): 39.6% GAAP, 42.5% adjusted.

- Adjusted Diluted EPS (Full Year): 6% increase to $4.98.

- Cash Flow from Operations (Full Year): $2 billion.

- Return to Shareholders (Full Year): Over $1.5 billion in dividends and share repurchases.

- Fiscal 2026 Revenue Growth Outlook: 16.5% to 18.5% expected growth.

- Management Solutions Growth Outlook (Fiscal 2026): 20% to 22% expected growth.

- PEO and Insurance Solutions Growth Outlook (Fiscal 2026): 6% to 8% expected growth.

- Interest on Funds Held for Clients Outlook (Fiscal 2026): $190 million to $200 million expected.

- Adjusted Operating Income Margin Outlook (Fiscal 2026): Approximately 43%.

- Adjusted Diluted EPS Growth Outlook (Fiscal 2026): 8.5% to 10.5% expected growth.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Paychex Inc (PAYX, Financial) achieved 10% revenue growth in the fourth quarter, driven by the successful integration of Paycor.

- The company reported a 6% growth in adjusted diluted earnings per share for the full fiscal year 2025.

- Client retention rates increased year-over-year, highlighting the value Paychex Inc (PAYX) provides to its clients.

- The Paycor acquisition surpassed expectations, leading to increased cost synergy expectations of approximately $90 million in fiscal year 2026.

- Paychex Inc (PAYX) expanded its client base to approximately 800,000 and increased HR outsourcing worksite employees to 2.5 million.

Negative Points

- There was some internal disruption due to changes in sales territories and training, impacting sales resources in the fourth quarter.

- The macro environment showed signs of uncertainty, with increased bankruptcies and financial distress in the micro end of the market.

- Checks per client trended softer in the fourth quarter, impacting organic growth rates.

- The PEO and Insurance Solutions segment faced headwinds due to decreased enrollment in the Florida at-risk medical plan.

- Diluted earnings per share decreased by 22% to $0.82 per share in the fourth quarter.